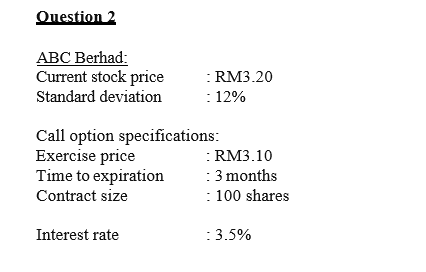

АВС Вerhad: Current stock price Standard deviation :RM3.20 : 12% Call option specifications: Exercise price Time to expiration Contract size : RM3.10 : 3 months : 100 shares Interest rate : 3.5%

Q: Q1 - What is the price of European call option on same stock, same expiry and same strike price. Q2…

A: The question is based on the concept of PUT-CALL parity. The theory of "put-call" parity explains…

Q: down 10 percent. Compute the fair market value of an American put option on Strategy Inc. stock with…

A: Put Option: A put option provides the buyer the right to exercise the option when the spot price of…

Q: Calculate the fair value of a put option using BSOPM based on the following information. Cumulative…

A: Here, Stock Price is RM40 Exercise Price is RM35 Annual Interest Rate is 12% Maturity is 180 days…

Q: ssume that you buy a single stock futures (SSF) of ABC Company with total initial margin of $2,000…

A: In this we need to calculate initial margin and calculate the profit on that.

Q: Current Price $100 Expected Price in 1 year Expected Dividend T-year T Bond yield $107.98 Beta 2.0…

A: Holding period return is referred to the total return received from holding an asset or portfolio of…

Q: jear long forward contract on a non-dividend-paying stock is entered into when the stock pric erest…

A: Difference between spot rate and forward rate is risk free interest rate.If difference between two…

Q: Consider a call option on Stock X. The call expires in 7 months and has a strike price X=$22. The…

A: A call option is an option in which the buyer has the choice but not the obligation to buy the…

Q: & non dividen poyng Consider a long forware Contrect to purchese Stock in Emoritht that the Current…

A: Forward Price = Spot Price*e^(rt) Where, r= risk freee Interest = 9% Months = 8 Years = 8/12 = 0.67…

Q: A stock currently trades at R84 and the interest rate is 1.25%. The 6-month forward price of this…

A: To construct an arbitrage strategy, we will first se what is arbitrage. Arbitrage is the act of…

Q: Ise the Black-Scholes formula for the following stock: Time to expiration 6 months Standard…

A: The given problem relates to Black and scholes model.

Q: . A one-month European put option on a non-dividend stock is currently selling for 2.50$. The stock…

A: An European put option can only be exercised on its maturity. It is a kind of derivative option that…

Q: The following data relate to a listed company. • Current share price = $160 • Exercise price =…

A: Given: Given: Particulars Amount Spot price $160.00 Standard deviation 40% Risk free rate…

Q: Calculate the theoretical forward price and initial value of the forward contract and explain the…

A: Forward Contract: A forward contract by it's name only suggests a contract pursued for future course…

Q: A 90-day put option for 10,000 ABC ordinary shares has an exercise price of 32 per share. The…

A: Exercise price is 32 per share Risk-free rate is 5% Market Value per share is 30 Total number of…

Q: You have been granted stock is 10 years. What is the opbons on 300 shares of your employer's stock.…

A: Intrinsic Value: It is the difference between the strike price and the underlying spot price.…

Q: A stock futures contract is priced at $27.18. The stock has a dividend yield of 1.25 percent and the…

A: Price of future contract is $27.18 and dividend yield and the risk-free rate are 1.25% and 2.5%…

Q: Intro You anticipate the receipt of money in 190 days, which you will use to purchase stocks in a…

A: The current selling price of a stock = $76 Dividend on stock : $0.5 in 50 days $0.6 in another 140…

Q: Based on the table, compute the 1. value of the call option 2. value of the put option. Contract…

A: Given: Particulars Current stock price 78.25 Standard deviation 36% Risk free rate 6.00%…

Q: A non-dividend-paying stock has a current price of 800 ngwee. In any unit of time (t, t + 1) the…

A: Given, (a) (u )= 25% Increase in % = 1 + 25% = 1.25 d = 20% Decrease % = 1 - 20% = 0.80 R = 1.04 Up…

Q: The common stock of Company XLT and its derivative securities currently trade in the market at the…

A: Part (a)Let's denote current stock price as S0, call premium as C, put premium as P, strike price as…

Q: Suppose a stock is currently (time t = 0) worth 100. Further, suppose the one year annually…

A: Note: Hi! Thank you for the question, As per the Honor code, we are allowed to answer the first…

Q: The market price of a stock is $35.00. An investor has purchased a call option for 100 shares of…

A: Price of underlying asset = $35 Exercise price = $20 Number of shares = 100 Intrinsic value of the…

Q: A stock is trading at $40. The market consensus expectation is that it will pay a dividend of $1 in…

A: The question is to calculate forward price of dividend paying stock.

Q: ppose that you enter into a six-month forward contract on a non-dividend paying stock when the stock…

A: Forward price can be calculated assuming interest to be compounding continuously.

Q: Contract size (in number of shares) 1,000 Strike price for an ABC Inc. share 124 Current value of an…

A: Options are the financial derivatives which gives the buyer the right to buy or sell an asset but…

Q: Assume that you buy a single stock futures (SSF) of ABC Company with total initial margin of $2,000…

A: Investing is a critical component of wealth growth. It enables the investor to fight inflation,…

Q: mmon stocK has (-free rate is 4 percent an market risk prem 7 регcent. EQUIRED Calculate the…

A: Price of common equity can be present value of dividends and present value of terminal value of…

Q: A.K. Scott’s stock is selling for $37 a share. A 3-month call on this stock with a strike price of…

A: The put-call parity is a term used to describe the relationship between call and put options in…

Q: The current price of a stock paying no income is 30. Assume the annually compounded zero rate will…

A: A legal agreement between two parties through which they agreed to sell or buy an asset at a…

Q: 1. Today's value of the S&P500 stock index is at 3,915. The 500 stocks underlying the index provide…

A: Prices of the assets change with the time which may arise the loss or gain. To avoid the losses,…

Q: The stock price of Top Gloves Bhd today is RM3.00. The call option on this stock with a strike price…

A:

Q: Current share price is $1.50 Call option exercise price is $1.80 in 3 months Risk free interest rate…

A: Delta hedging is a popular risk-neutral investment strategy used in options trading strategy by…

Q: stock market Future market January KLSE composite index stands at 1162. Investor expects to purchase…

A: The question is related to Spot transactions profit or loss.

Q: A stock is about to pay a dividend. You are given tock's current price is 110. tock pays dividends…

A: In this we have use the given formula and calculate the price of call option.

Q: A 6-month put option on Smith Corp.'s stock has a strike price of $43.50 and sells in the market for…

A: An option premium is the sum of intrinsic and extrinsic value of an option. In other words, we can…

Q: Contract size (in number of shares) 100,000 Market value of an ABC Inc. share 32 Exercise price for…

A: Black Scholes Merton formula With volatility, the value of call option is calculated using Black…

Q: J-Rata Corp shares are currently trading at $30 each. It is expected to increase by 10% or decrease…

A: Solution- So=$30 Strike price (k)=$32 Risk free rate=8% (per anum) q=(e^0.08*3/12) -0.94/ (1.1-0.94)…

Q: he Moon company currently sells for 100 $. The annual stock price volatility is %10 and risk- free…

A: The question is based on valuation of option by use of Black and Scholes model. Formula as:

Calculate the price of a call and a put option based on the Black-Scholes option pricing.

Step by step

Solved in 3 steps with 1 images

- Put–Call Parity The current price of a stock is $33, and the annual risk-free rate is 6%. A call option with a strike price of $32 and with 1 year until expiration has a current value of $6.56. What is the value of a put option written on the stock with the same exercise price and expiration date as the call option?Binomial Model The current price of a stock is 20. In 1 year, the price will be either 26 or 16. The annual risk-free rate is 5%. Find the price of a call option on the stock that has a strike price of 21 and that expires in 1 year. (Hint: Use daily compounding.)A non paying dividend stock's price is 51. Call option delta is 0.5. Stock volatility is 0.2.By using BS model, the premium of 9 months 56-strike priced European Call option is (Please keep four decimal places).

- 13. Assume Company AAA options have an exercise price of $45 and expire in 156 days. The current price of Company AAA stock is $44.375. The (annually compounded) risk-free rate is 7 percent per year and the standard deviation of Company AAA's stock returns is 0.31. Calculate d1 [Use the Black-Scholes formula].12. A non paying dividend stock is priced at 50. Call option delta is 0.5. Stock volatility is 0.29. By using BS model, the premium of 55-strike priced European call option in 6 months isUmberto Consulting Limited Convertible Bond Common Equity Par Value $1,000.00 Coupon (Annual Payment) 0.03 Current Market Price $975.00 $30.50 Straight Bond Value $935.00 Conversion Ratio 30 Conversion Option Any Time Dividend $1.00 Expected Market Price in One Year $38.25 Required: Using the information in the tables above, please calculate the current market conversion price and the following expected rates of return. Assume coupons are received before any conversion takes place. (Use cells A3 to C10 from the given information to complete this question.) Umberto Consulting Limited Market Conversion Price Expected Rate of Return, Convertible Bond Expected Return of Return, Common Equity

- Question content area top Part 1 (Preferred stock valuation) Pioneer's preferred stock is selling for $40 in the market and pays a $4.40 annual dividend. a. If the market's required yield is 9 percent, what is the value of the stock for that investor? b. Should the investor acquire the stock? Question content area bottom Part 1 a. The value of the stock for that investor is $enter your response here per share. (Round to the nearest cent.)(Valuing common Stock) Assume the following: • The investor’s required rate of return is 15 percent. • The expected level of earnings at the end of this year (E1) is $5.00. • The retention ratio is 50 percent. • The return on equity (ROE) is 20 percent (that is, it can earn 20 percent on reinvested earnings). • Similar shares of stock sell at multiples of 10 times earnings per share. a. Determine the price/earnings ratio (P/E1) b. What is the stock price using the P/E ratio valuation method? c. What is the stock price using the dividend discount model? d. What would happen to the P/E ratio (P/E1) and stock price if the firm could earn 25 percent on reinvested earnings (ROE)? e. What does this tell you about the relationship between the rate the firm can earn on reinvested earnings and the P/E ratio? 2. Jelaskan mengapa investor menganggap bahwa saha(Valuing common Stock) Assume the following: • The investor’s required rate of return is 15 percent. • The expected level of earnings at the end of this year (E1) is $5.00. • The retention ratio is 50 percent. • The return on equity (ROE) is 20 percent (that is, it can earn 20 percent on reinvested earnings). • Similar shares of stock sell at multiples of 10 times earnings per share. A. Determine the price/earnings ratio (P/E1) B. What is the stock price using the P/E ratio valuation method? C. What is the stock price using the dividend discount model? D. What would happen to the P/E ratio (P/E1) and stock price if the firm could earn 25 percent on reinvested earnings (ROE)? E. What does this tell you about the relationship between the rate the firm can earn on reinvested earnings and the P/E ratio?

- A.K. Scott’s stock is selling for $37 a share. A 3-month call on this stock with a strike price of $38 is priced at $2. Risk-free assets are currently returning 0.28 percent per month. a) What should be the price of a 3-month put option on this stock with a strike price of $38? b) Which of the two options is currently in the money and does that accord with your conclusions about their relative prices?Question content area top Part 1 (Preferred stock valuation) Pioneer's preferred stock is selling for $21 in the market and pays a $2.70 annual dividend. a. If the market's required yield is 11 percent, what is the value of the stock for that investor? b. Should the investor acquire the stock? Question content area bottom Part 1 a. The value of the stock for that investor is $enter your response here per share. (Round to the nearest cent.) Part 2 b. Should the investor acquire the stock? (Select from the drop-down menus.) The investor ▼ should should not acquire the stock because it is currently ▼ underpriced overpriced in the market.Question content area top Part 1 (Preferred stock valuation) Kendra Corporation's preferred shares are trading for $29 in the market and pay a $4.70 annual dividend. Assume that the market's required yield is 17 percent. a. What is the stock's value to you, the investor? b. Should you purchase the stock? Question content area bottom Part 1 a. The value of the stock to you, the investor, is $enter your response here per share. (Round to the nearest cent.)