b) Suppose that you observe the following information in Table 2 for stocks A and B: Table 2 Expected Return (%) 11% Stock Beta A 0.8 В 14% 1.5 The risk-free rate of return is 6% and the expected rate of return on the market index is 12%. Using the Single-Index Model, calculate the alpha of both stocks. Show your calculations. Explain what the alpha of the single-factor model represents and interpret your results.

b) Suppose that you observe the following information in Table 2 for stocks A and B: Table 2 Expected Return (%) 11% Stock Beta A 0.8 В 14% 1.5 The risk-free rate of return is 6% and the expected rate of return on the market index is 12%. Using the Single-Index Model, calculate the alpha of both stocks. Show your calculations. Explain what the alpha of the single-factor model represents and interpret your results.

Chapter6: Risk And Return

Section: Chapter Questions

Problem 14P

Related questions

Question

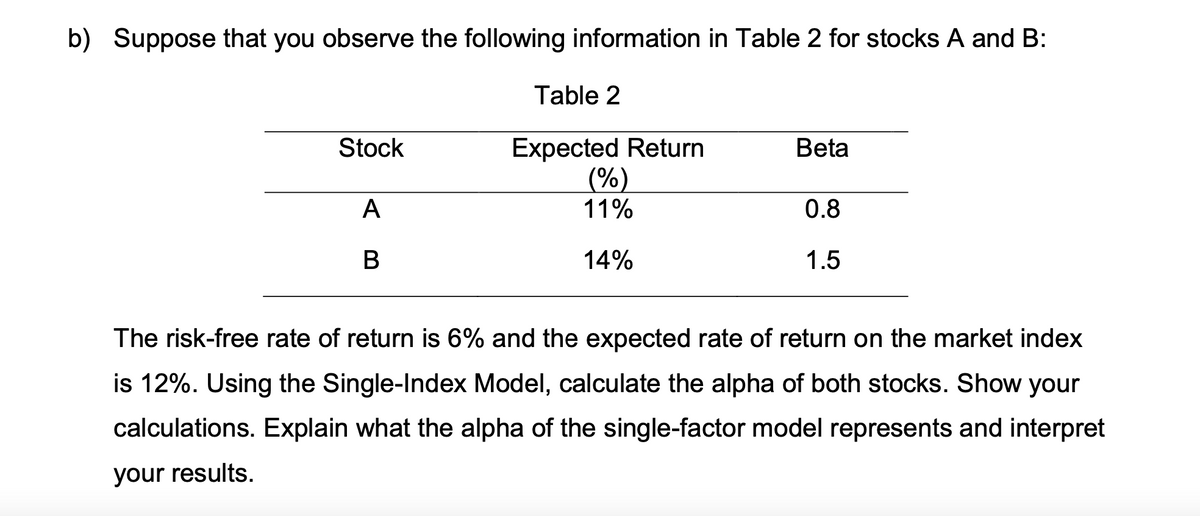

Transcribed Image Text:b) Suppose that you observe the following information in Table 2 for stocks A and B:

Table 2

Expected Return

(%)

11%

Stock

Beta

A

0.8

В

14%

1.5

The risk-free rate of return is 6% and the expected rate of return on the market index

is 12%. Using the Single-Index Model, calculate the alpha of both stocks. Show your

calculations. Explain what the alpha of the single-factor model represents and interpret

your results.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT