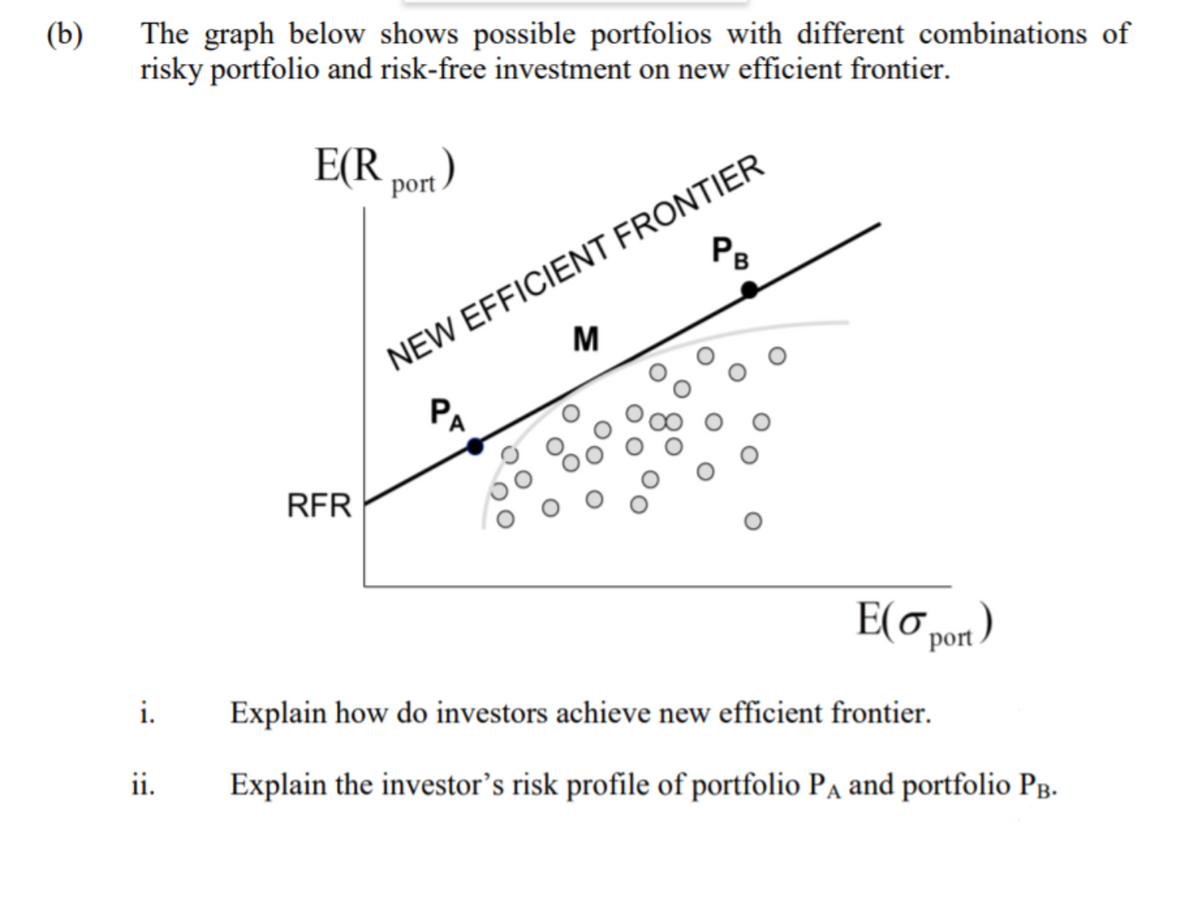

(b) The graph below shows possible portfolios with different combinations of risky portfolio and risk-free investment on new efficient frontier. E(R Port ) NEW EFFICIENT FRONTIER M RFR E(O port) i. Explain how do investors achieve new efficient frontier. ii. Explain the investor's risk profile of portfolio Pa and portfolio PB.

(b) The graph below shows possible portfolios with different combinations of risky portfolio and risk-free investment on new efficient frontier. E(R Port ) NEW EFFICIENT FRONTIER M RFR E(O port) i. Explain how do investors achieve new efficient frontier. ii. Explain the investor's risk profile of portfolio Pa and portfolio PB.

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 13QTD

Related questions

Question

Transcribed Image Text:(b)

The graph below shows possible portfolios with different combinations of

risky portfolio and risk-free investment on new efficient frontier.

E(R port )

NEW EFFICIENT FRONTIER

PA

RFR

E(o pon)

port

i.

Explain how do investors achieve new efficient frontier.

ii.

Explain the investor's risk profile of portfolio Pa and portfolio Pg.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning