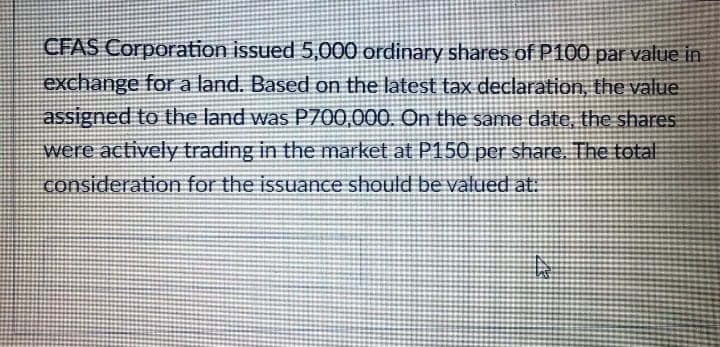

CFAS Corporation issued 5,000 ordinary shares of P100 par value in Exchange for a land. Based on the latest tax declaration, the value assigned to the land was P700,000. On the same date, the shares were actively trading in the market at P150 per share. The total consideration for the issuance should be valued at:

CFAS Corporation issued 5,000 ordinary shares of P100 par value in Exchange for a land. Based on the latest tax declaration, the value assigned to the land was P700,000. On the same date, the shares were actively trading in the market at P150 per share. The total consideration for the issuance should be valued at:

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter15: Contributed Capital

Section: Chapter Questions

Problem 1MC

Related questions

Question

Transcribed Image Text:CFAS Corporation issued 5,000 ordinary shares of P100 par value in

exchange for a land. Based on the latest tax declaration, the value.

assigned to the land was P700,000. On the same date, the shares

were actively trading in the market at P150 per share. The total

consideration for the issuance should be valued at:

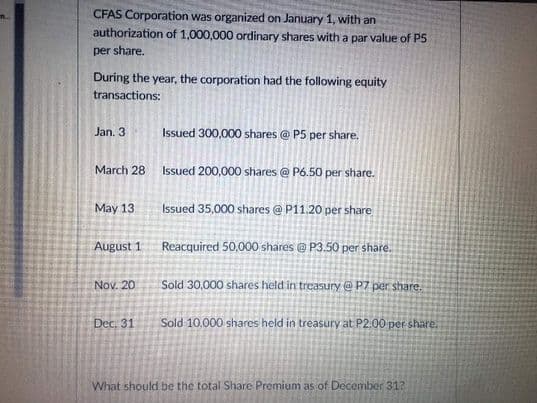

Transcribed Image Text:CFAS Corporation was organized on January 1, with an

authorization of 1,000,000 ordinary shares with a par value of P5

per share.

During the year, the corporation had the following equity

transactions:

Jan. 3

Issued 300,000 shares @ P5 per share.

March 28

Issued 200,000 shares @ P6.50 per share.

May 13

Issued 35,000 shares @ P11.20 per share

August 1

Reacquired 50,000 shares @ P3.50 per share.

Nov. 20

Sold 30,000 shares held in treasury @ P7 per share.

Dec. 31

Sold 10.000 shares held in treasury at P2.00 per share.

What should be the total Share Premium as of December 31?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning