Company Z enters into a 5-year interest rate swap contract on 1 January 2015 as the fixed-rate payer party. The settlement period is one year. The settlement dates are 31 December of each year from 2015 to 2019. The spot rates of interest at the beginning of various years for investment horizons of t = 1,2,3, 4 and 5 years are given in the following table. t 1 Jan 2015 1 Jan 2016 1 Jan 2017 1 Jan 2018 1 Jan 2019 0.35% 0.71% 1.43% 2.05% 0.79% 0.42% 0.34% 0.47% 0.95% 0.31% 0.38% 0.57% 1.08% 1.58% 1 1.24% 1.72% 2.59% 3.24% 0.64% 1.05% 3 1.78% 2.31% 4 2.94% 3.55% 1.47% (a) Assuming a level notional amount of $1 million for the contract, determine the swap rate. (b) Suppose the contract is an accreting swap with notional amounts of $1 million, $3 million, $5 million, $7 million and $9 million. Determine the swap rate.

Company Z enters into a 5-year interest rate swap contract on 1 January 2015 as the fixed-rate payer party. The settlement period is one year. The settlement dates are 31 December of each year from 2015 to 2019. The spot rates of interest at the beginning of various years for investment horizons of t = 1,2,3, 4 and 5 years are given in the following table. t 1 Jan 2015 1 Jan 2016 1 Jan 2017 1 Jan 2018 1 Jan 2019 0.35% 0.71% 1.43% 2.05% 0.79% 0.42% 0.34% 0.47% 0.95% 0.31% 0.38% 0.57% 1.08% 1.58% 1 1.24% 1.72% 2.59% 3.24% 0.64% 1.05% 3 1.78% 2.31% 4 2.94% 3.55% 1.47% (a) Assuming a level notional amount of $1 million for the contract, determine the swap rate. (b) Suppose the contract is an accreting swap with notional amounts of $1 million, $3 million, $5 million, $7 million and $9 million. Determine the swap rate.

Financial Accounting Intro Concepts Meth/Uses

14th Edition

ISBN:9781285595047

Author:Weil

Publisher:Weil

Chapter13: Marketable Securities And Derivatives

Section: Chapter Questions

Problem 30P

Related questions

Question

I need the ans in 30 min I give u 3 likes immediately

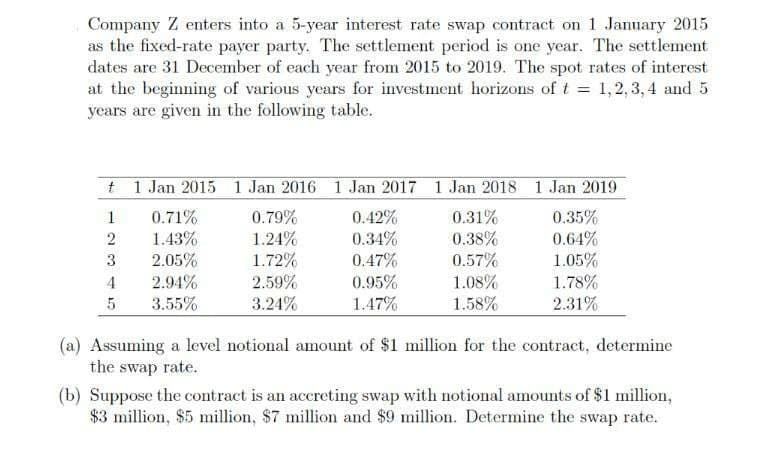

Transcribed Image Text:Company Z enters into a 5-year interest rate swap contract on 1 January 2015

as the fixed-rate payer party. The settlement period is one year. The settlement

dates are 31 December of each year from 2015 to 2019. The spot rates of interest

at the beginning of various years for investment horizons of t = 1,2, 3, 4 and 5

years are given in the following table.

t 1 Jan 2015 1 Jan 2016 1 Jan 2017 1 Jan 2018 1 Jan 2019

0.71%

1.43%

2.05%

0.42%

0.34%

0.79%

0.35%

0.31%

0.38%

0.57%

1.08%

1.58%

1

0.64%

1.05%

1.24%

1.72%

0.47%

0.95%

1.47%

3

2.94%

2.59%

1.78%

5

3.55%

3.24%

2.31%

(a) Assuming a level notional amount of $1 million for the contract, determine

the swap rate.

(b) Suppose the contract is an acereting swap with notional amounts of $1 million,

$3 million, $5 million, $7 million and $9 million. Determine the swap rate.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 6 steps with 10 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you