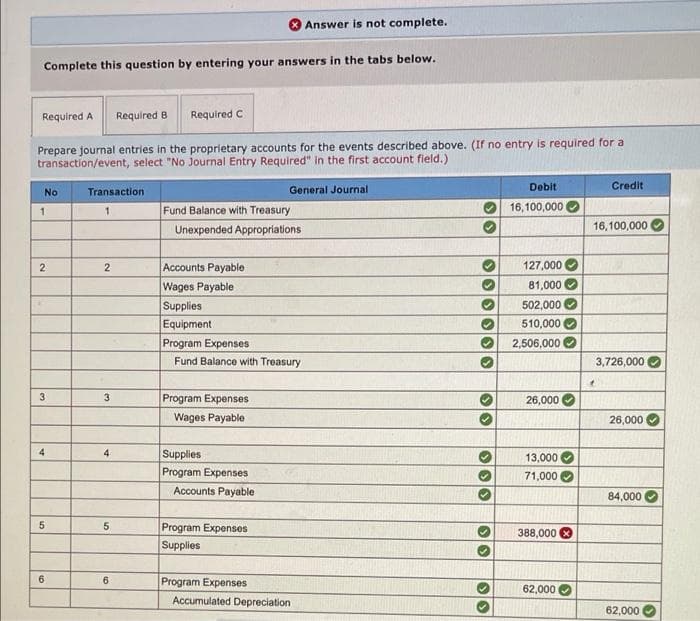

Complete this question by entering your answers in the tabs below. Required A Required B Required C "repare journal entries in the proprietary accounts for the events described above. (If no entry is required for a ransaction/event, select "No Journal Entry Required" in the first account field.) Transaction General Journal Debit Credit No Fund Balance with Treasury 16, 100,000 16,100,000 Unexpended Appropriations 2 Accounts Payable 127,000 Wages Payable Supplies Equipment Program Expenses 81,000 O 502,000 510,000 2,506,000 Fund Balance with Treasury 3,726,000 Program Expenses Wages Payable 3 26,000 O 26,000 Supplies Program Expenses 4 13,000 71,000 Accounts Payable 84,000 Program Expenses Supplies 5. 388,000 O 6. Program Expenses 62,000 Accumulated Depreciation 62,000

Complete this question by entering your answers in the tabs below. Required A Required B Required C "repare journal entries in the proprietary accounts for the events described above. (If no entry is required for a ransaction/event, select "No Journal Entry Required" in the first account field.) Transaction General Journal Debit Credit No Fund Balance with Treasury 16, 100,000 16,100,000 Unexpended Appropriations 2 Accounts Payable 127,000 Wages Payable Supplies Equipment Program Expenses 81,000 O 502,000 510,000 2,506,000 Fund Balance with Treasury 3,726,000 Program Expenses Wages Payable 3 26,000 O 26,000 Supplies Program Expenses 4 13,000 71,000 Accounts Payable 84,000 Program Expenses Supplies 5. 388,000 O 6. Program Expenses 62,000 Accumulated Depreciation 62,000

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter12: Intangibles

Section: Chapter Questions

Problem 10MC

Related questions

Question

Requirement A

Transcribed Image Text:Answer is not complete.

Complete this question by entering your answers in the tabs below.

Required A

Required B

Required C

Prepare journal entries in the proprietary accounts for the events described above. (If no entry is required for a

transaction/event, select "No Journal Entry Required" in the first account field.)

Debit

Credit

No

Transaction

General Journal

Fund Balance with Treasury

Unexpended Appropriations

16, 100,000

1.

16,100,000

2

Accounts Payable

127,000 O

2.

Wages Payable

Supplies

Equipment

Program Expenses

81,000 O

502,000 O

510,000 O

2,506,000

Fund Balance with Treasury

3,726,000

3

Program Expenses

26,000

Wages Payable

26,000

4

4

Supplies

13,000

Program Expenses

71,000

Accounts Payable

84,000

Program Expenses

Supplies

5.

388,000 O

Program Expenses

62,000

Accumulated Depreciation

62,000

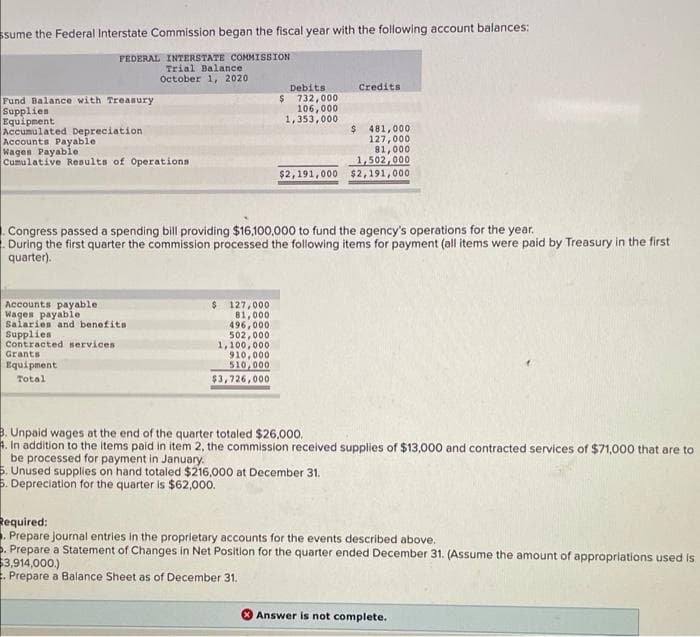

Transcribed Image Text:ssume the Federal Interstate Commission began the fiscal year with the following account balances:

FEDERAL INTERSTATE COMMISSION

Trial Balance

October 1, 2020

Debits

Credits

Pund Balance with Treasury

Supplies

Equipment

Accumulated Depreciation

Accounts Payable

Wages Payable

Cumulative Results of Operations

$ 732,000

106,000

1,353,000

$ 481,000

127,000

81,000

1,502,000

$2,191,000 $2,191,000

Congress passed a spending bill providing $16,100,000 to fund the agency's operations for the year.

During the first quarter the commission processed the following items for payment (all items were paid by Treasury in the first

quarter).

Accounts payable

Wages payable

Salarien and benefits

Supplies

Contracted services

$ 127,000

81,000

496,000

502,000

1,100,000

910,000

510,000

$3,726,000

Grants

Equipment

Total

B. Unpaid wages at the end of the quarter totaled $26,000.

4. In addition to the items paid in item 2, the commission received supplies of $13,000 and contracted services of $71,000 that are to

be processed for payment in January.

5. Unused supplies on hand totaled $216,000 at December 31.

5. Depreciation for the quarter is $62,000.

Required:

. Prepare Journal entries in the proprietary accounts for the events described above.

. Prepare a Statement of Changes in Net Position for the quarter ended December 31. (Assume the amount of appropriations used is

3,914,000.)

E. Prepare a Balance Sheet as of December 31.

Answer is not complete.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning