Consider the following information on a portfolio of three stocks: State of Probability of State Stock A Rate of Economy Boom Normal of Economy Return Stock B Rate of Return .15 Stock C Rate of Return 04 .34 .48 .53 .12 .24 Bust .22 .32 .18 -.23 -.37 a. If your portfolio is invested 36 percent each in A and B and 28 percent in C, what is the portfolio's expected return, the variance, and the standard deviation? Note: Do not round intermediate calculations. Round your variance answer to 5 decimal places, e.g., .16161. Enter your other answers as a percent rounded to 2 decimal places, e.g., 32.16. b. If the expected T-bill rate is 4.35 percent, what is the expected risk premium on the portfolio? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. a. Expected return 6.94 % Variance 0.19200 Standard deviation 0.44 % b. Expected risk premium 2.59 %

Consider the following information on a portfolio of three stocks: State of Probability of State Stock A Rate of Economy Boom Normal of Economy Return Stock B Rate of Return .15 Stock C Rate of Return 04 .34 .48 .53 .12 .24 Bust .22 .32 .18 -.23 -.37 a. If your portfolio is invested 36 percent each in A and B and 28 percent in C, what is the portfolio's expected return, the variance, and the standard deviation? Note: Do not round intermediate calculations. Round your variance answer to 5 decimal places, e.g., .16161. Enter your other answers as a percent rounded to 2 decimal places, e.g., 32.16. b. If the expected T-bill rate is 4.35 percent, what is the expected risk premium on the portfolio? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. a. Expected return 6.94 % Variance 0.19200 Standard deviation 0.44 % b. Expected risk premium 2.59 %

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 12P

Related questions

Question

Pakodi

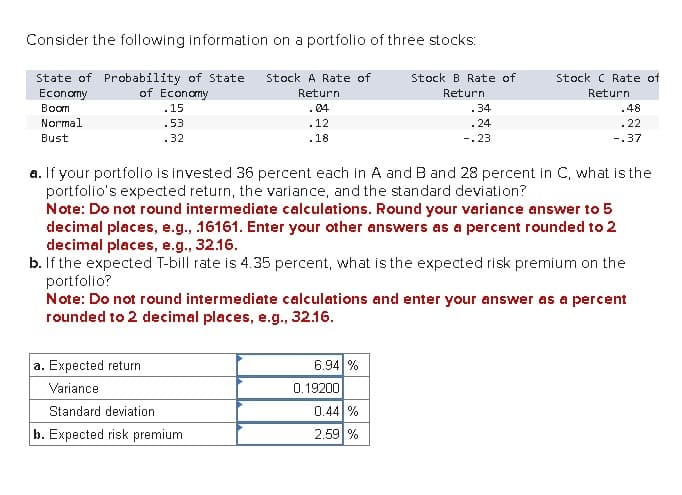

Transcribed Image Text:Consider the following information on a portfolio of three stocks:

State of Probability of State

Stock A Rate of

Economy

Boom

Normal

of Economy

Return

Stock B Rate of

Return

.15

Stock C Rate of

Return

04

.34

.48

.53

.12

.24

Bust

.22

.32

.18

-.23

-.37

a. If your portfolio is invested 36 percent each in A and B and 28 percent in C, what is the

portfolio's expected return, the variance, and the standard deviation?

Note: Do not round intermediate calculations. Round your variance answer to 5

decimal places, e.g., .16161. Enter your other answers as a percent rounded to 2

decimal places, e.g., 32.16.

b. If the expected T-bill rate is 4.35 percent, what is the expected risk premium on the

portfolio?

Note: Do not round intermediate calculations and enter your answer as a percent

rounded to 2 decimal places, e.g., 32.16.

a. Expected return

6.94 %

Variance

0.19200

Standard deviation

0.44 %

b. Expected risk premium

2.59 %

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 1 images

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning