Consider the Orstein-Uhlenbeck process Y = e-a"E + o :le-a(t-s) dW, t>0, where a and o are positive constants, W = (Wt)t>o is a Wiener mar- tingale with respect to a filtration (F;)t>0, and § is an Fo-measurable random variable with variance E(§ – E£)² = v². Determine the co- variance function C(s,t) = E((Y – EY;)(Y, – EY,)) for 0 < s < t in terms of s, t, a, o and v. Hence for h > 0 calculate %3D - lim C(s, s+ h). (Vou mou ugo 1ut proof that Ćond +he stoc intogro1 rt o-ar d

Consider the Orstein-Uhlenbeck process Y = e-a"E + o :le-a(t-s) dW, t>0, where a and o are positive constants, W = (Wt)t>o is a Wiener mar- tingale with respect to a filtration (F;)t>0, and § is an Fo-measurable random variable with variance E(§ – E£)² = v². Determine the co- variance function C(s,t) = E((Y – EY;)(Y, – EY,)) for 0 < s < t in terms of s, t, a, o and v. Hence for h > 0 calculate %3D - lim C(s, s+ h). (Vou mou ugo 1ut proof that Ćond +he stoc intogro1 rt o-ar d

Linear Algebra: A Modern Introduction

4th Edition

ISBN:9781285463247

Author:David Poole

Publisher:David Poole

Chapter7: Distance And Approximation

Section7.3: Least Squares Approximation

Problem 32EQ

Related questions

Question

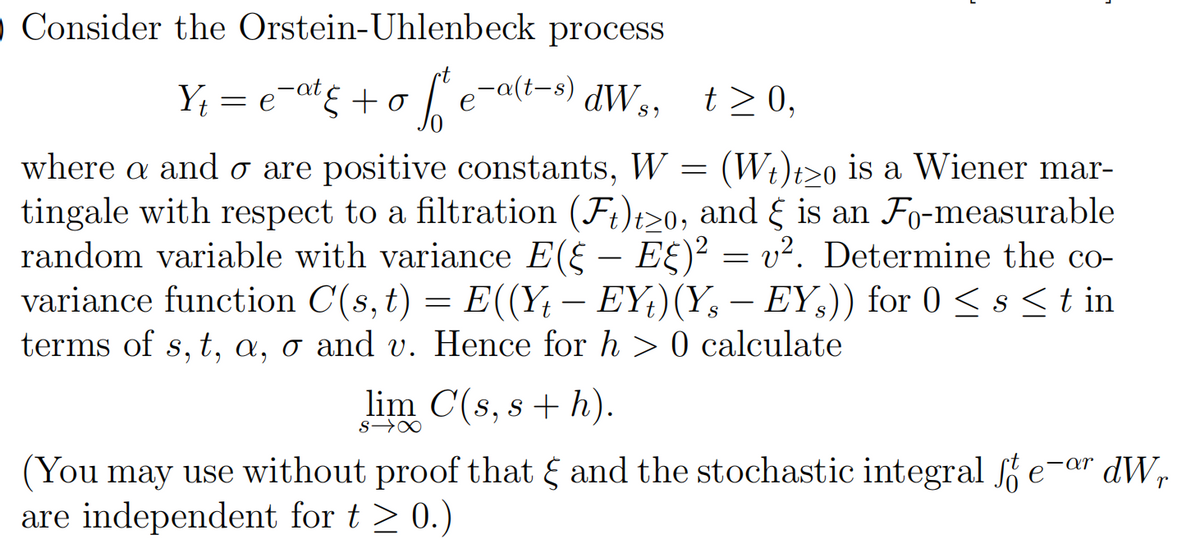

Transcribed Image Text:o Consider the Orstein-Uhlenbeck process

Y; = e-at¢ +o [ e-a(i-s) dW,,

dW s,

t>0,

where a and o are positive constants, W = (Wt)t>o is a Wiener mar-

tingale with respect to a filtration (F;)t>0, and { is an Fo-measurable

random variable with variance E(§ -

variance function C(s,t)

terms of s, t, a, o and v. Hence for h > 0 calculate

E£)² = v². Determine the co-

) = E((Y; – EY;)(Y, – EY,)) for 0 < s <t in

-

lim C(s, s + h).

s→∞

(You may use without proof that and the stochastic integral e-ar dW,

are independent for t > 0.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Recommended textbooks for you

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning