d. If a taxable temporary difference originates in 2022, it will cause taxable income for 2022 to be. pretax financial income for 2022. (less than, greater than) e. If total tax expense is $50,000 and deferred tax expense is $65,000, then the current portion of the expense computation is referred to as a current tax. (expense, benefit) of $_ f. If a company's tax return shows taxable income of $105,000 for Year 2 and a tax rate of 40%, how much will appear on the December 31, Year 2, statement of financial position for “Income taxes payable" if the company has made estimated tax payments of $36,500 for Year 2?

d. If a taxable temporary difference originates in 2022, it will cause taxable income for 2022 to be. pretax financial income for 2022. (less than, greater than) e. If total tax expense is $50,000 and deferred tax expense is $65,000, then the current portion of the expense computation is referred to as a current tax. (expense, benefit) of $_ f. If a company's tax return shows taxable income of $105,000 for Year 2 and a tax rate of 40%, how much will appear on the December 31, Year 2, statement of financial position for “Income taxes payable" if the company has made estimated tax payments of $36,500 for Year 2?

Chapter18: Accounting Periods And Methods

Section: Chapter Questions

Problem 9DQ: LO.2 Osprey Corporation, an accrual basis taxpayer, had taxable income for 2019 and paid 40,000 on...

Related questions

Question

Complete the following statements by filling in the blanks. Please make sure to indicate the subparts when you are answering.

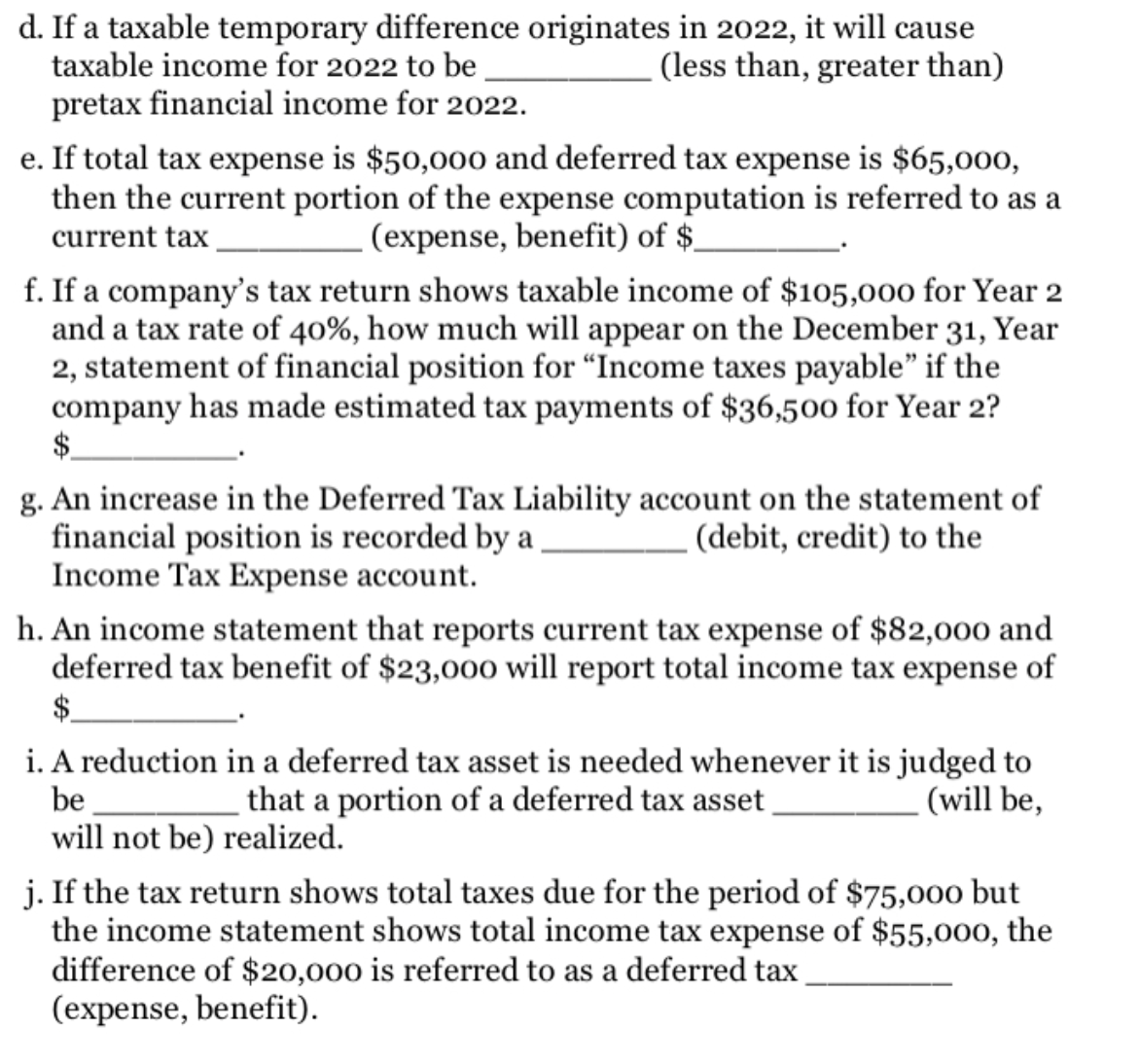

Transcribed Image Text:d. If a taxable temporary difference originates in 2022, it will cause

taxable income for 2022 to be

(less than, greater than)

pretax financial income for 2022.

e. If total tax expense is $50,000 and deferred tax expense is $65,000,

then the current portion of the expense computation is referred to as a

.(expense, benefit) of $-

current tax

f. If a company's tax return shows taxable income of $105,000 for Year 2

and a tax rate of 40%, how much will appear on the December 31, Year

2, statement of financial position for “Income taxes payable" if the

company has made estimated tax payments of $36,500 for Year 2?

$.

g. An increase in the Deferred Tax Liability account on the statement of

financial position is recorded by a

Income Tax Expense account.

. (debit, credit) to the

h. An income statement that reports current tax expense of $82,000 and

deferred tax benefit of $23,000 will report total income tax expense of

$.

i. A reduction in a deferred tax asset is needed whenever it is judged to

that a portion of a deferred tax asset

be

will not be) realized.

- (will be,

j. If the tax return shows total taxes due for the period of $75,000 but

the income statement shows total income tax expense of $55,000, the

difference of $20,000 is referred to as a deferred tax

(expense, benefit).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning