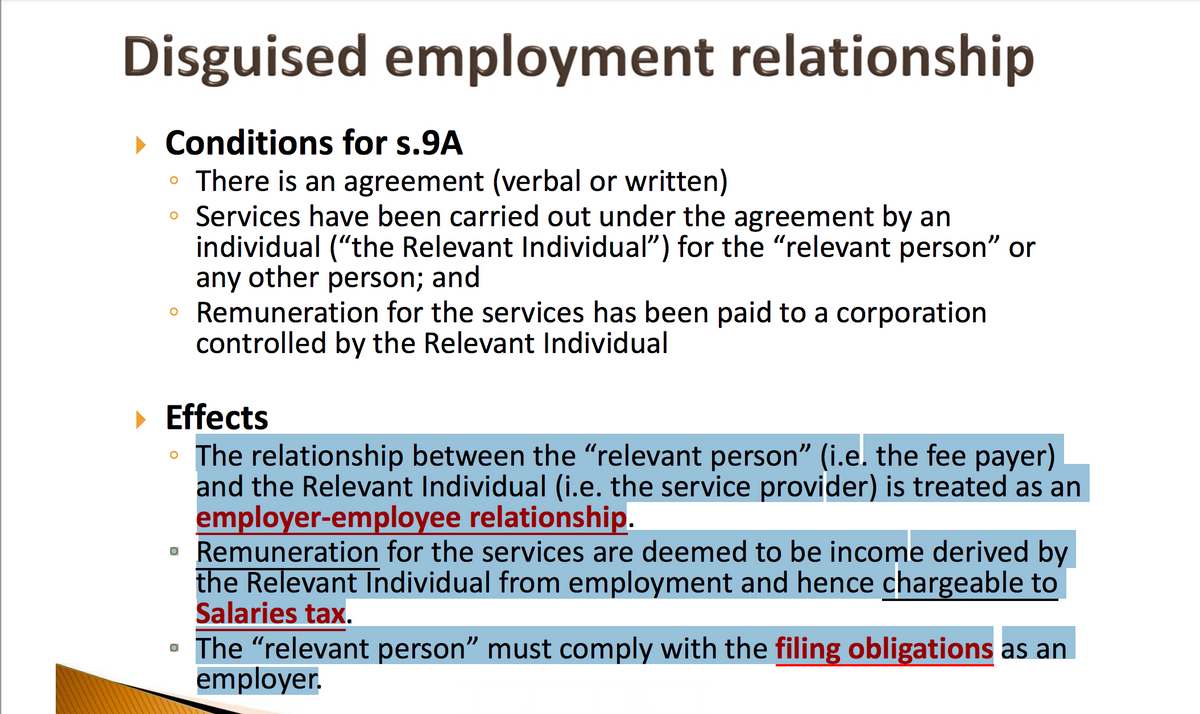

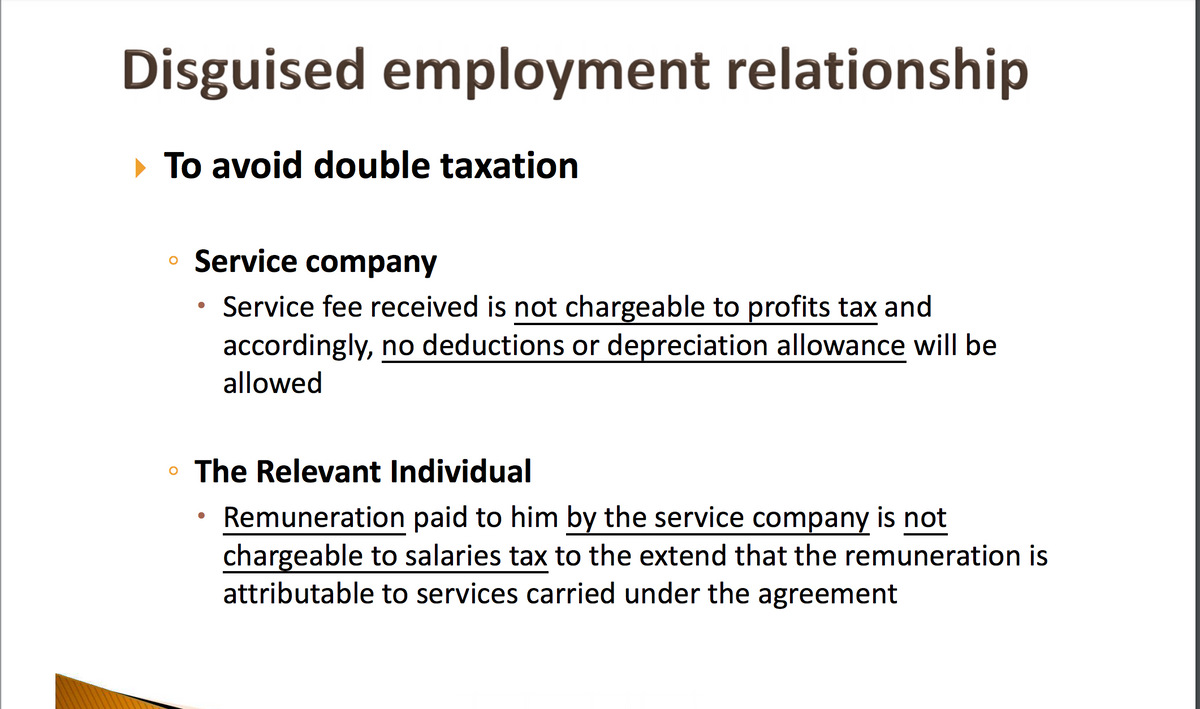

Disguised employment relationship ▸ Conditions for s.9A о 。 There is an agreement (verbal or written) 。 Services have been carried out under the agreement by an individual ("the Relevant Individual") for the "relevant person" or any other person; and 。 Remuneration for the services has been paid to a corporation controlled by the Relevant Individual Effects 0 The relationship between the "relevant person” (i.e. the fee payer) and the Relevant Individual (i.e. the service provider) is treated as an employer-employee relationship. • Remuneration for the services are deemed to be income derived by the Relevant Individual from employment and hence chargeable to Salaries tax. 0 ⚫ The "relevant person” must comply with the filing obligations as an employer. Disguised employment relationship To avoid double taxation • Service company Service fee received is not chargeable to profits tax and accordingly, no deductions or depreciation allowance will be allowed The Relevant Individual Remuneration paid to him by the service company is not chargeable to salaries tax to the extend that the remuneration is attributable to services carried under the agreement

Disguised employment relationship ▸ Conditions for s.9A о 。 There is an agreement (verbal or written) 。 Services have been carried out under the agreement by an individual ("the Relevant Individual") for the "relevant person" or any other person; and 。 Remuneration for the services has been paid to a corporation controlled by the Relevant Individual Effects 0 The relationship between the "relevant person” (i.e. the fee payer) and the Relevant Individual (i.e. the service provider) is treated as an employer-employee relationship. • Remuneration for the services are deemed to be income derived by the Relevant Individual from employment and hence chargeable to Salaries tax. 0 ⚫ The "relevant person” must comply with the filing obligations as an employer. Disguised employment relationship To avoid double taxation • Service company Service fee received is not chargeable to profits tax and accordingly, no deductions or depreciation allowance will be allowed The Relevant Individual Remuneration paid to him by the service company is not chargeable to salaries tax to the extend that the remuneration is attributable to services carried under the agreement

Chapter23: Exempt Entities

Section: Chapter Questions

Problem 1BCRQ

Related questions

Question

It is talking about "Hong Kong Tax system, tax planning, type I service company, disguised employment relationship", can you explain these two slides? What is condition and what is effect? And if the service fee is chrageable to salaries tax and profit tax? As these two slides have some contradiction between if it is chargeable to salaries and profit tax. Or I interpreted it wrongly.

Transcribed Image Text:Disguised employment relationship

▸ Conditions for s.9A

о

。 There is an agreement (verbal or written)

。 Services have been carried out under the agreement by an

individual ("the Relevant Individual") for the "relevant person" or

any other person; and

。 Remuneration for the services has been paid to a corporation

controlled by the Relevant Individual

Effects

0

The relationship between the "relevant person” (i.e. the fee payer)

and the Relevant Individual (i.e. the service provider) is treated as an

employer-employee relationship.

• Remuneration for the services are deemed to be income derived by

the Relevant Individual from employment and hence chargeable to

Salaries tax.

0

⚫ The "relevant person” must comply with the filing obligations as an

employer.

Transcribed Image Text:Disguised employment relationship

To avoid double taxation

• Service company

Service fee received is not chargeable to profits tax and

accordingly, no deductions or depreciation allowance will be

allowed

The Relevant Individual

Remuneration paid to him by the service company is not

chargeable to salaries tax to the extend that the remuneration is

attributable to services carried under the agreement

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning