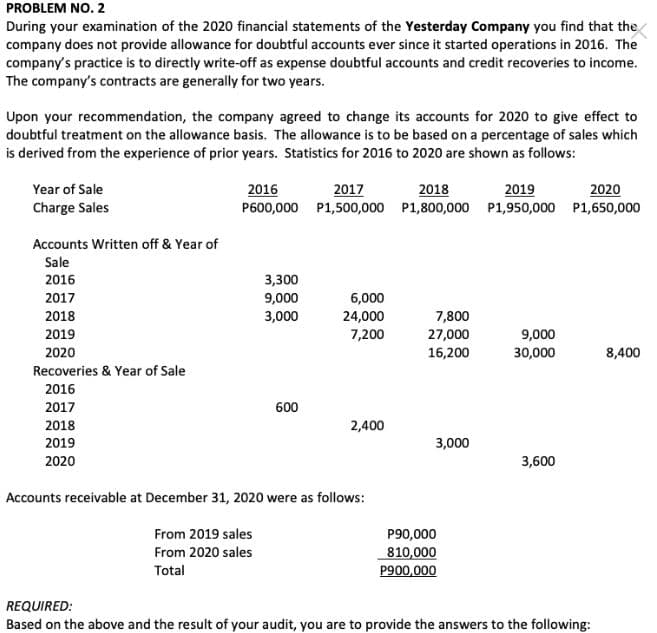

During your examination of the 2020 financial statements of the Yesterday Company you find that the company does not provide allowance for doubtful accounts ever since it started operations in 2016. The company's practice is to directly write-off as expense doubtful accounts and credit recoveries to income. The company's contracts are generally for two years. Upon your recommendation, the company agreed to change its accounts for 2020 to give effect to doubtful treatment on the allowance basis. The allowance is to be based on a percentage of sales which is derived from the experience of prior years. Statistics for 2016 to 2020 are shown as follows: 2017 2018 2019 Year of Sale Charge Sales 2016 P600,000 2020 P1,650,000 P1,500,000 P1,800,000 P1,950,000 Accounts Written off & Year of Sale 2016 3,300 2017 9,000 6,000 2018 3,000 24,000 7,800 2019 7,200 27,000 9,000 2020 16,200 30,000 8,400 Recoveries & Year of Sale 2016 2017 600 2018 2,400 2019 3,000 2020 3,600 Accounts receivable at December 31, 2020 were as follows: From 2019 sales From 2020 sales Total P90,000 810,000 P900,000

Bad Debts

At the end of the accounting period, a financial statement is prepared by every company, then at that time while preparing the financial statement, the company determines among its total receivable amount how much portion of receivables is collected by the company during that accounting period.

Accounts Receivable

The word “account receivable” means the payment is yet to be made for the work that is already done. Generally, each and every business sells its goods and services either in cash or in credit. So, when the goods are sold on credit account receivable arise which means the company is going to get the payment from its customer to whom the goods are sold on credit. Usually, the credit period may be for a very short period of time and in some rare cases it takes a year.

1. The average percentage of net doubtful accounts to charge sales that should be used in setting up the 2020 allowance is?

2. How much is the doubtful account expense for 2020

Step by step

Solved in 4 steps with 2 images