For each of the following situations, indicate the type of report that would be required as well as how various paragraphs/sections of he auditors'report would be modified in the audit of an issuer. Assume any amount in question is material on an overall basis (but not pervasive) unless otherwise noted. 1. The entity is subject to a going-concern uncertainty and has properly disclosed this uncertainty in its financial statements. 2. The entity has changed from an accounting principle in accordance with GAAP to an accounting principle not in accordance with GAAP. 3. The audit team encounters a material, but not pervasive, scope limitation; this limitation has not been imposed by the client. 4. The entity's financial statements are presented in accordance with GAAP. 5. The entity has changed from one accounting principle in accordance with GAAP to another principle in accordance with GAAP; this change has been properly reported by restating prior years' financial statements. 5. After accepting the engagement, the audit team determines that the firm is not independent. 7. The entity's financial statements contain a material and pervasive departure from GAAP. 3. The group auditors' opinion on group financial statements is based partially on the report of component auditors. 9. The entity presents condensed financial statements along with its full set of financial statements. ). The audit team was unable to observe ending inventories because of late appointment, this represented a material and pervasive

For each of the following situations, indicate the type of report that would be required as well as how various paragraphs/sections of he auditors'report would be modified in the audit of an issuer. Assume any amount in question is material on an overall basis (but not pervasive) unless otherwise noted. 1. The entity is subject to a going-concern uncertainty and has properly disclosed this uncertainty in its financial statements. 2. The entity has changed from an accounting principle in accordance with GAAP to an accounting principle not in accordance with GAAP. 3. The audit team encounters a material, but not pervasive, scope limitation; this limitation has not been imposed by the client. 4. The entity's financial statements are presented in accordance with GAAP. 5. The entity has changed from one accounting principle in accordance with GAAP to another principle in accordance with GAAP; this change has been properly reported by restating prior years' financial statements. 5. After accepting the engagement, the audit team determines that the firm is not independent. 7. The entity's financial statements contain a material and pervasive departure from GAAP. 3. The group auditors' opinion on group financial statements is based partially on the report of component auditors. 9. The entity presents condensed financial statements along with its full set of financial statements. ). The audit team was unable to observe ending inventories because of late appointment, this represented a material and pervasive

Auditing: A Risk Based-Approach (MindTap Course List)

11th Edition

ISBN:9781337619455

Author:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Chapter15: Audit Reports For Financial Statement Audits

Section: Chapter Questions

Problem 3CYBK

Related questions

Question

Please do not give image format

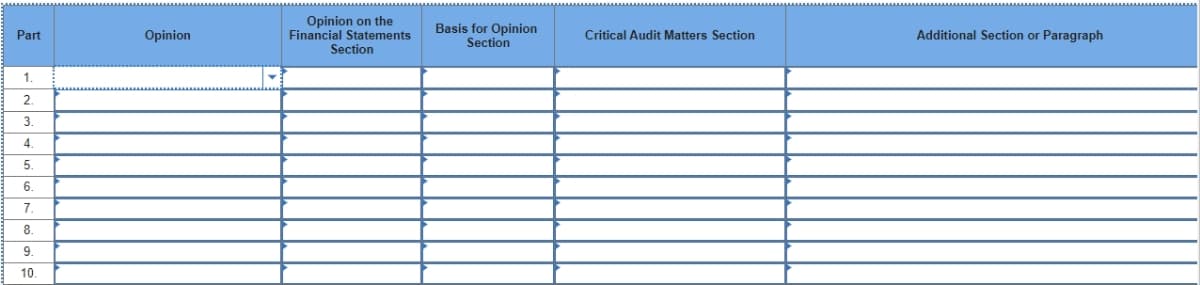

Transcribed Image Text:Part

1.

2

3.

4

5.

6.

7.

8.

9.

10.

Opinion

Opinion on the

Financial Statements

Section

Basis for Opinion

Section

Critical Audit Matters Section

Additional Section or Paragraph

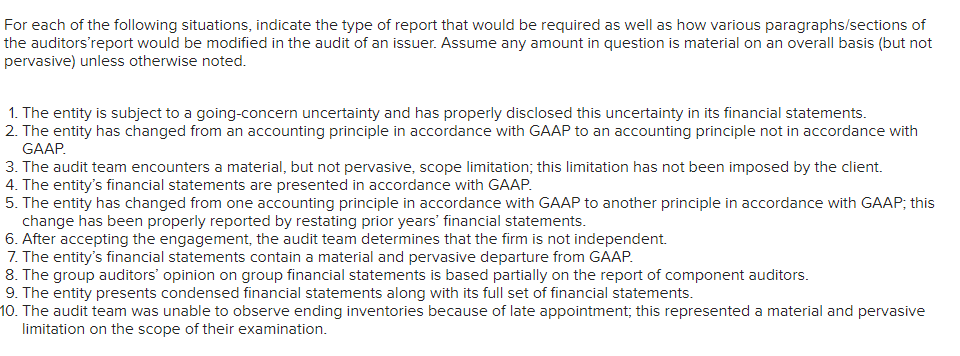

Transcribed Image Text:For each of the following situations, indicate the type of report that would be required as well as how various paragraphs/sections of

the auditors'report would be modified in the audit of an issuer. Assume any amount in question is material on an overall basis (but not

pervasive) unless otherwise noted.

1. The entity is subject to a going-concern uncertainty and has properly disclosed this uncertainty in its financial statements.

2. The entity has changed from an accounting principle in accordance with GAAP to an accounting principle not in accordance with

GAAP.

3. The audit team encounters a material, but not pervasive, scope limitation; this limitation has not been imposed by the client.

4. The entity's financial statements are presented in accordance with GAAP.

5. The entity has changed from one accounting principle in accordance with GAAP to another principle in accordance with GAAP; this

change has been properly reported by restating prior years' financial statements.

6. After accepting the engagement, the audit team determines that the firm is not independent.

7. The entity's financial statements contain a material and pervasive departure from GAAP.

8. The group auditors' opinion on group financial statements is based partially on the report of component auditors.

9. The entity presents condensed financial statements along with its full set of financial statements.

10. The audit team was unable to observe ending inventories because of late appointment; this represented a material and pervasive

limitation on the scope of their examination.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub