From the information generated in the previous two questions; a) Identify two investment alternatives that can be combined in a portfolio. Assume a 50-50 investment allocation in each investment alternative b) Compute the expected return of the portfolio thus formed c) Compute the portfolio’s beta. Is the portfolio aggressive or defensive?

From the information generated in the previous two questions; a) Identify two investment alternatives that can be combined in a portfolio. Assume a 50-50 investment allocation in each investment alternative b) Compute the expected return of the portfolio thus formed c) Compute the portfolio’s beta. Is the portfolio aggressive or defensive?

Essentials of Business Analytics (MindTap Course List)

2nd Edition

ISBN:9781305627734

Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Chapter15: Decision Analysis

Section: Chapter Questions

Problem 4P: Investment advisors estimated the stock market returns for four market segments: computers,...

Related questions

Question

All computations must be done and shown manually. No spreadsheet computations are allowed.

Question 3

From the information generated in the previous two questions;

a) Identify two investment alternatives that can be combined in a portfolio. Assume a 50-50 investment allocation in each investment alternative

b) Compute the expected return of the portfolio thus formed

c) Compute the portfolio’s beta. Is the portfolio aggressive or defensive?

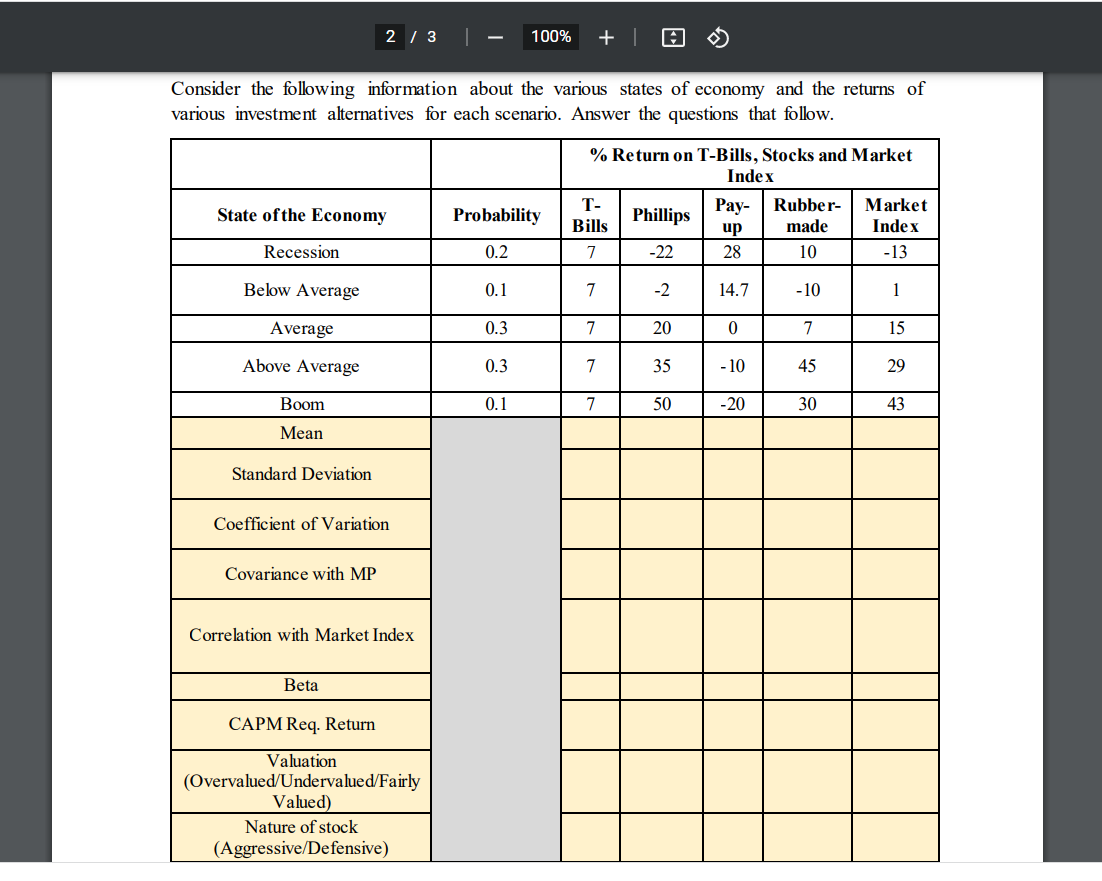

Transcribed Image Text:State of the Economy

Recession

Below Average

Average

Consider the following information about the various states of economy and the returns of

various investment alternatives for each scenario. Answer the questions that follow.

Above Average

Boom

Mean

Standard Deviation

2 / 3

Coefficient of Variation

Covariance with MP

Correlation with Market Index

Beta

CAPM Req. Return

Valuation

(Overvalued/Undervalued/Fairly

Valued)

-

Nature of stock

(Aggressive/Defensive)

Probability

0.2

0.1

0.3

100% +

0.3

0.1

% Return on T-Bills, Stocks and Market

Index

T-

Bills

7

7

7

7

7

Phillips

-22

-2

20

35

50

Pay-

up

28

14.7

0

-10

-20

Rubber-

made

10

-10

7

45

30

Market

Index

-13

1

15

29

43

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 9 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning