Heath Production manufactures chairs. Several weeks ago, the company received an enquiry from Rose Limited. Rose wants to market a foldable chair similar to one of Heath's, and has offered to purchase 11 000 units if the offer can be completed in three months. The cost data for Heath's foldable chair is as follow: Direct material $16.40 Direct labour (0.125 @ $36 per hour) 4.50 Total manufacturing overhead 20.00 Total $40.90 The normal selling price of Heath's foldable chair is $53.00. However, Rose has offered Heath only $31.50 because of the large quantity it is willing to purchase. Rose requires a modification of the design that will allow a $4.20 reduction in direct material cost. The production manager of Heath notes that the company will incur $7400 in additional setup costs and will have to purchase a $4800 special equipment to manufacturing the units for Rose. The equipment will be discarded once the special order is completed. Total manufacturing overhead costs are applied to production at the rate of $40 per machine hour. The figure is based, in part, on budgeted annual fixed overhead of $1 500 000 and planned production activity of 60 000 machine hours (5000 hours per month). Rose will allocate $3600 of existing fixed administrative costs to the order as "part of the cost of doing business". Required: a) Which of the data above should be ignored in making the special order decision? For what reason? b) Assume that Heath's present sales will not be affected by the special order, should the order be accepted from the financial point of view? Show calculation. c) Assume that Heath's current production activity 80 per cent of planned machine hours, can the company accept the order and meet Rose's deadline? Explain.

Heath Production manufactures chairs. Several weeks ago, the company received an enquiry from Rose Limited. Rose wants to market a foldable chair similar to one of Heath's, and has offered to purchase 11 000 units if the offer can be completed in three months. The cost data for Heath's foldable chair is as follow: Direct material $16.40 Direct labour (0.125 @ $36 per hour) 4.50 Total manufacturing overhead 20.00 Total $40.90 The normal selling price of Heath's foldable chair is $53.00. However, Rose has offered Heath only $31.50 because of the large quantity it is willing to purchase. Rose requires a modification of the design that will allow a $4.20 reduction in direct material cost. The production manager of Heath notes that the company will incur $7400 in additional setup costs and will have to purchase a $4800 special equipment to manufacturing the units for Rose. The equipment will be discarded once the special order is completed. Total manufacturing overhead costs are applied to production at the rate of $40 per machine hour. The figure is based, in part, on budgeted annual fixed overhead of $1 500 000 and planned production activity of 60 000 machine hours (5000 hours per month). Rose will allocate $3600 of existing fixed administrative costs to the order as "part of the cost of doing business". Required: a) Which of the data above should be ignored in making the special order decision? For what reason? b) Assume that Heath's present sales will not be affected by the special order, should the order be accepted from the financial point of view? Show calculation. c) Assume that Heath's current production activity 80 per cent of planned machine hours, can the company accept the order and meet Rose's deadline? Explain.

Chapter10: Short-term Decision Making

Section: Chapter Questions

Problem 6PA: Gent Designs requires three units of part A for every unit of Al that it produces. Currently, part A...

Related questions

Question

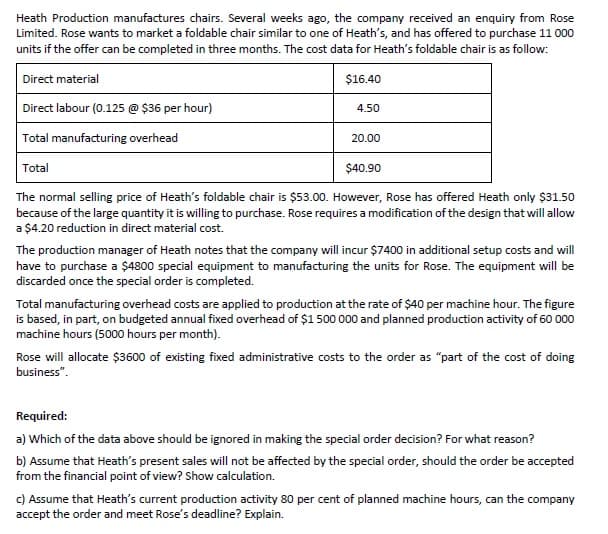

Transcribed Image Text:Heath Production manufactures chairs. Several weeks ago, the company received an enquiry from Rose

Limited. Rose wants to market a foldable chair similar to one of Heath's, and has offered to purchase 11 000

units if the offer can be completed in three months. The cost data for Heath's foldable chair is as follow:

Direct material

$16.40

Direct labour (0.125 @ $36 per hour)

4.50

Total manufacturing overhead

20.00

Total

$40.90

The normal selling price of Heath's foldable chair is $53.00. However, Rose has offered Heath only $31.50

because of the large quantity it is willing to purchase. Rose requires a modification of the design that will allow

a $4.20 reduction in direct material cost.

The production manager of Heath notes that the company will incur $7400 in additional setup costs and will

have to purchase a $4800 special equipment to manufacturing the units for Rose. The equipment will be

discarded once the special order is completed.

Total manufacturing overhead costs are applied to production at the rate of $40 per machine hour. The figure

is based, in part, on budgeted annual fixed overhead of $1 500 000 and planned production activity of 60 000

machine hours (500o hours per month).

Rose will allocate $3600 of existing fixed administrative costs to the order as "part of the cost of doing

business".

Required:

a) Which of the data above should be ignored in making the special order decision? For what reason?

b) Assume that Heath's present sales will not be affected by the special order, should the order be accepted

from the financial point of view? Show calculation.

c) Assume that Heath's current production activity 80 per cent of planned machine hours, can the company

accept the order and meet Rose's deadline? Explain.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,