I just want to clarify the solution provided for our review material: In adjusting the capital accounts, why is under depreciated in the equipment of Francis subtracted and over depreciation added in Rinna? Does this apply to all problems that deals with over depreciation and under depreciation? Isn't it, add when under depreciated and subtract when over depreciated?

I just want to clarify the solution provided for our review material: In adjusting the capital accounts, why is under depreciated in the equipment of Francis subtracted and over depreciation added in Rinna? Does this apply to all problems that deals with over depreciation and under depreciation? Isn't it, add when under depreciated and subtract when over depreciated?

Chapter10: Partnerships: Formation, Operation, And Basis

Section: Chapter Questions

Problem 2BCRQ

Related questions

Question

Hi I just want to clarify the solution provided for our review material:

In adjusting the capital accounts, why is under

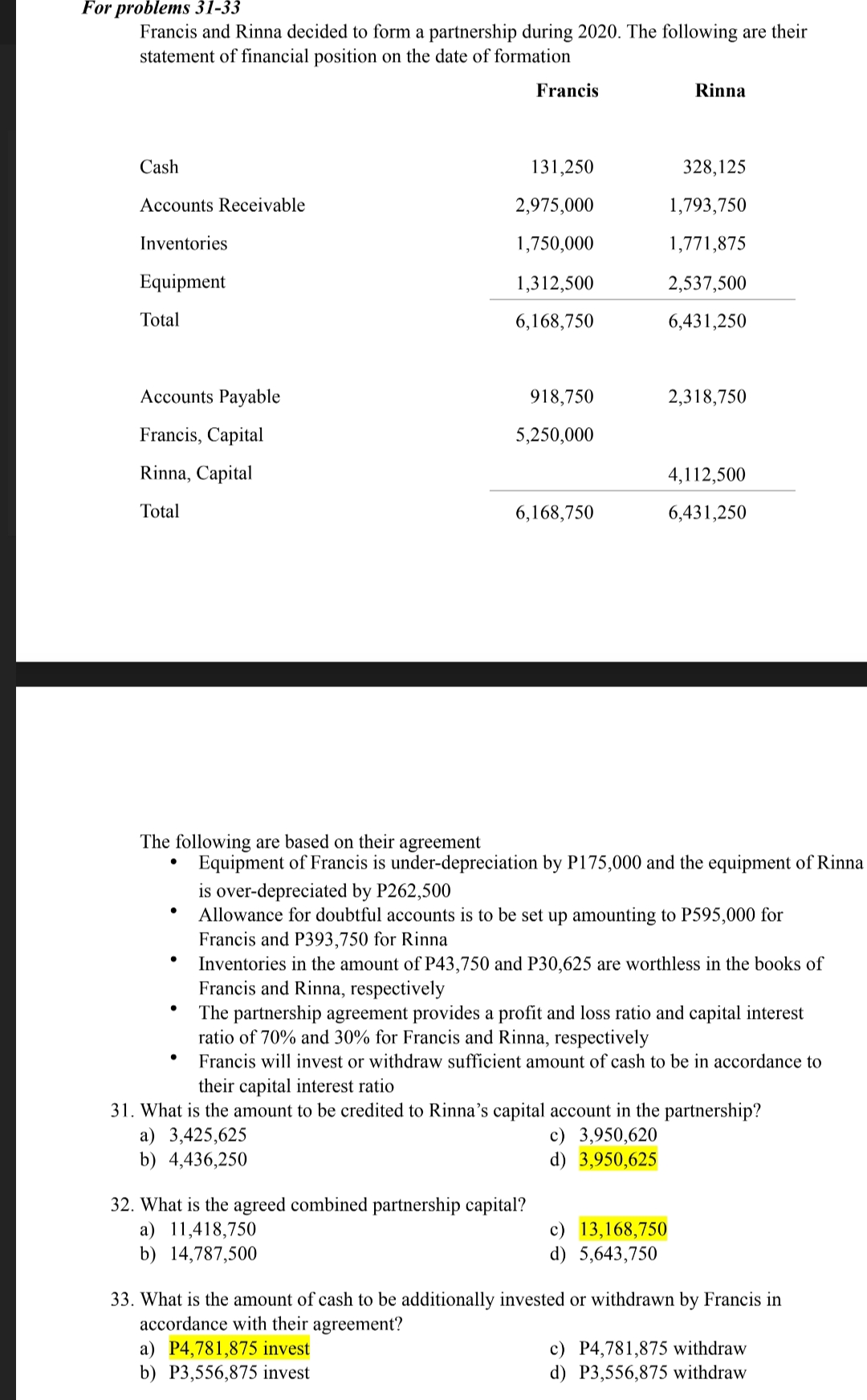

Transcribed Image Text:For problems 31-33

Francis and Rinna decided to form a partnership during 2020. The following are their

statement of financial position on the date of formation

Francis

Rinna

Cash

131,250

328,125

Accounts Receivable

2,975,000

1,793,750

Inventories

1,750,000

1,771,875

Equipment

1,312,500

2,537,500

Total

6,168,750

6,431,250

Accounts Payable

918,750

2,318,750

Francis, Capital

5,250,000

Rinna, Capital

4,112,500

Total

6,168,750

6,431,250

The following are based on their agreement

• Equipment of Francis is under-depreciation by P175,000 and the equipment of Rinna

is over-depreciated by P262,500

Allowance for doubtful accounts is to be set up amounting to P595,000 for

Francis and P393,750 for Rinna

Inventories in the amount of P43,750 and P30,625 are worthless in the books of

Francis and Rinna, respectively

The partnership agreement provides a profit and loss ratio and capital interest

ratio of 70% and 30% for Francis and Rinna, respectively

Francis will invest or withdraw sufficient amount of cash to be in accordance to

their capital interest ratio

31. What is the amount to be credited to Rinna's capital account in the partnership?

a) 3,425,625

b) 4,436,250

c) 3,950,620

d) 3,950,625

32. What is the agreed combined partnership capital?

a) 11,418,750

b) 14,787,500

c) 13,168,750

d) 5,643,750

33. What is the amount of cash to be additionally invested or withdrawn by Francis in

accordance with their agreement?

a) P4,781,875 invest

b) P3,556,875 invest

c) P4,781,875 withdraw

d) P3,556,875 withdraw

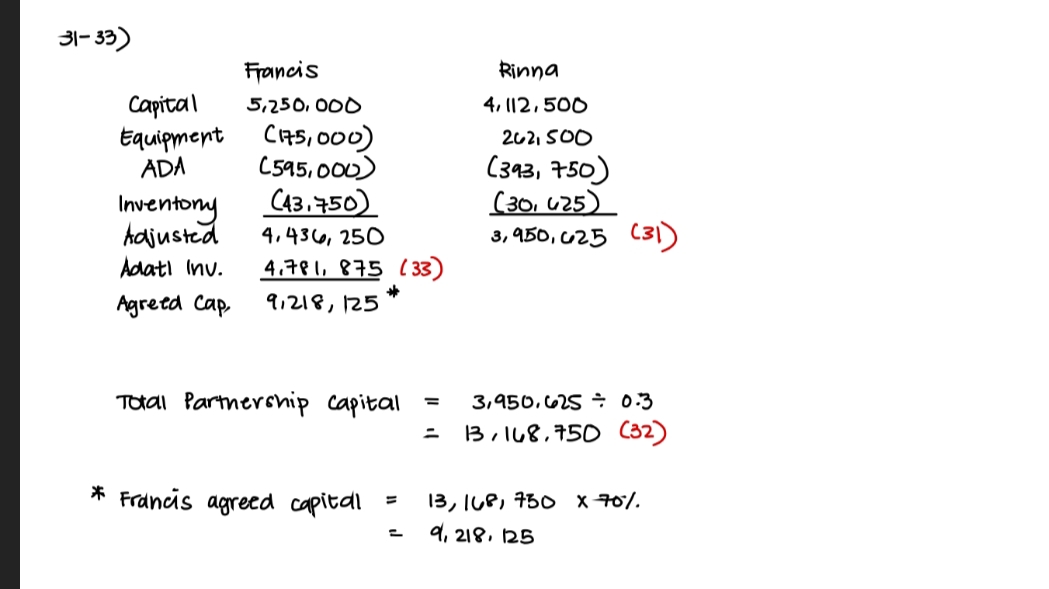

Transcribed Image Text:31- 33)

Francis

Rinna

Capital

5,250, 000

4, I12,500

Equipment CAS, 000)

ADA

(545,000)

CA3.750)

202, SOO

(313, 750)

(30, U25)

3, 950, U25 (31)

Inventory

Adjusted

Adati Inv.

4,436, 250

4.781, 875 ( 33)

Agreta Cap.

9,218, 125

Ttai Partnercnip capital

3,950,625 ÷ 0.3

13,l48,750 (32)

* Francis agrecd capital

13, IUP, 730 x70%

9, 218, 25

%3D

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning