In each of the following scenarios (i) to (iv), advise on the appropriate accounting treatment for the intangible assets for year ended 31 March 2018. On 1 April 2017, HHH acquired, from a bankrupt competitor, a license to provide radio broadcast services to a region within Ireland. This license would have been originally issued by the government for a ten-year period at zero cost, but has a market value due to its exclusivity. The cost of the license to Handsetter was RM3.3 million, and the remaining useful economic life was 6 years. i. ii. On 1 April 2017, HHH commenced work on developing a new technology to enhance the quality of the radio broadcasts. It purchased a number of patents at a cost of RM2 million and spent a further RM6 million developing the technology, as well as RM2 million researching the international market for the technology in advance of its launch. The directors of HHH were confident throughout the development process that the technology had massive potential to generate future economic benefit. On 31 March 2018, this opinion was validated when a rival broadcaster offered HHH RM15 million for its partially developed technology project. i. As a result of HHH's growing reputation in the broadcasting industry, the directors commissioned a consulting firm to value its brand name. The brand name has not been recognised as an asset in the financial statements to date. On 31 March 2018, the consultants issued a report stating that the fair value of HHH's brand was RM20 million. iv. HHH has a portfolio of patents it developed over the past few years. These represent technologies and processes used in the company's business to generate economic benefits. The total carrying value of these patents was RM2.8 million at 1 April 2017. They originally had a 15-year useful economic life, but on average seven years remain to their expiry date. The directors propose, at 31 March 2018, to revalue this portfolio to its estimated fair value of RM5 million.

In each of the following scenarios (i) to (iv), advise on the appropriate accounting treatment for the intangible assets for year ended 31 March 2018. On 1 April 2017, HHH acquired, from a bankrupt competitor, a license to provide radio broadcast services to a region within Ireland. This license would have been originally issued by the government for a ten-year period at zero cost, but has a market value due to its exclusivity. The cost of the license to Handsetter was RM3.3 million, and the remaining useful economic life was 6 years. i. ii. On 1 April 2017, HHH commenced work on developing a new technology to enhance the quality of the radio broadcasts. It purchased a number of patents at a cost of RM2 million and spent a further RM6 million developing the technology, as well as RM2 million researching the international market for the technology in advance of its launch. The directors of HHH were confident throughout the development process that the technology had massive potential to generate future economic benefit. On 31 March 2018, this opinion was validated when a rival broadcaster offered HHH RM15 million for its partially developed technology project. i. As a result of HHH's growing reputation in the broadcasting industry, the directors commissioned a consulting firm to value its brand name. The brand name has not been recognised as an asset in the financial statements to date. On 31 March 2018, the consultants issued a report stating that the fair value of HHH's brand was RM20 million. iv. HHH has a portfolio of patents it developed over the past few years. These represent technologies and processes used in the company's business to generate economic benefits. The total carrying value of these patents was RM2.8 million at 1 April 2017. They originally had a 15-year useful economic life, but on average seven years remain to their expiry date. The directors propose, at 31 March 2018, to revalue this portfolio to its estimated fair value of RM5 million.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter12: Intangibles

Section: Chapter Questions

Problem 8P

Related questions

Question

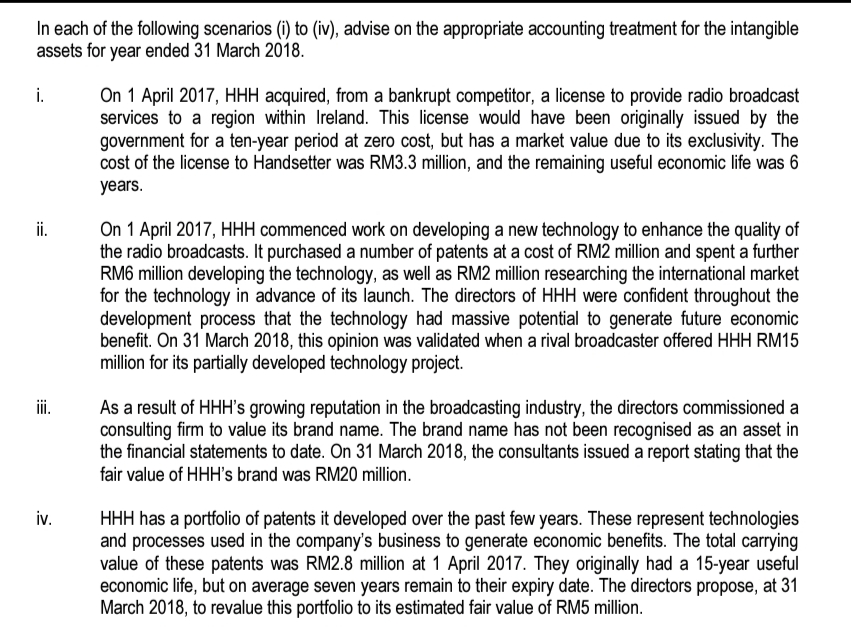

Transcribed Image Text:In each of the following scenarios (i) to (iv), advise on the appropriate accounting treatment for the intangible

assets for year ended 31 March 2018.

On 1 April 2017, HHH acquired, from a bankrupt competitor, a license to provide radio broadcast

services to a region within Ireland. This license would have been originally issued by the

government for a ten-year period at zero cost, but has a market value due to its exclusivity. The

cost of the license to Handsetter was RM3.3 million, and the remaining useful economic life was 6

years.

i.

ii.

On 1 April 2017, HHH commenced work on developing a new technology to enhance the quality of

the radio broadcasts. It purchased a number of patents at a cost of RM2 million and spent a further

RM6 million developing the technology, as well as RM2 million researching the international market

for the technology in advance of its launch. The directors of HHH were confident throughout the

development process that the technology had massive potential to generate future economic

benefit. On 31 March 2018, this opinion was validated when a rival broadcaster offered HHH RM15

million for its partially developed technology project.

i.

As a result of HHH's growing reputation in the broadcasting industry, the directors commissioned a

consulting firm to value its brand name. The brand name has not been recognised as an asset in

the financial statements to date. On 31 March 2018, the consultants issued a report stating that the

fair value of HHH's brand was RM20 million.

iv.

HHH has a portfolio of patents it developed over the past few years. These represent technologies

and processes used in the company's business to generate economic benefits. The total carrying

value of these patents was RM2.8 million at 1 April 2017. They originally had a 15-year useful

economic life, but on average seven years remain to their expiry date. The directors propose, at 31

March 2018, to revalue this portfolio to its estimated fair value of RM5 million.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning