Jay Rexford, president of Photo Artistry Company, was just concluding a budget meeting with his senior staff. It was November of 20x1, and the group was discussing preparation of the firm’s master budget for 20x2. “I've decided to go ahead and purchase the industrial robot we’ve been talking about. We’ll make the acquisition on January 2 of next year, and I expect it will take most of the year to train the personnel and reorganize the production process to take full advantage of the new equipment.” In response to a question about financing the acquisition, Rexford replied as follows: “The robot will cost $950,000. There will also be an additional $50,000 in ancillary equipment to be purchased. We’ll finance these purchases with a one‑year $1,000,000 loan from Shark Bank and Trust Company. I’ve negotiated a repayment schedule of four equal installments on the last day of each quarter. The interest rate will be 10 percent, and interest payments will be quarterly as well.” With that the meeting broke up, and the budget process was on. Photo Artistry Company is a manufacturer of metal picture frames. The firm’s two product lines are designated as S (small frames; 5 × 7 inches) and L (large frames; 8 × 10 inches). The primary raw materials are flexible metal strips and 9‑inch by 24‑inch glass sheets. Each S frame requires a 2‑foot metal strip; an L frame requires a 3‑foot metal strip. Allowing for normal breakage and scrap glass, the company can get either four S frames or two L frames out of a glass sheet. Other raw materials, such as cardboard backing, are insignificant in cost and are treated as indirect materials. Emily Jackson, Photo Artistry's controller, is in charge of preparing the master budget for 20x2. She has gathered the following information: Sales in the 4th quarter of 20x1 are expected to be 50,000 S frames and 40,000 L frames. The sales manager predicts that over the next 2 years, sales in each product line will grow by 5,000 units each quarter over the previous quarter. For example, S frame sales in the 1st quarter of 20x2 are expected to be 55,000 units. Photo Artistry's sales history indicates that 60% of all sales are on credit, with the remainder of the sales in cash. The company’s collection experience shows that 80% of the credit sales are collected during the quarter in which the sale is made, while the remaining 20% is collected in the, following quarter. For simplicity, assume the company is able to collect 100% of its accounts receivable. The S frame sells for $10, and the L frame sells for $15. These prices are expected to hold constant throughout 20x2. The production manager attempts to end each quarter with enough finished‑goods inventory in each product line to cover 20% of the following quarter’s sales. Photo Artistry makes an attempt to end each quarter with 20% of the glass sheets needed for the following quarter's production. The company wants to have an inventory of 10,400 sheets at the end of 20x2. Metal strips are purchased locally and the company buys them on a just‑in‑time basis. Inventory of metal strips is negligible. All direct‑material purchases are made on account, and 80% of each quarter’s purchases are paid in cash during the same quarter as the purchase. The other 20% is paid in the next quarter. Indirect materials are purchased with cash as needed. Work‑in‑process is negligible. Projected manufacturing costs in 20x2 are as follow: S Frame L Frame Direct material: Metal strips: S: 2 ft. @ $1 per foot $2.00 L: 3 ft. @ $1 per foot $3.00 Glass sheets: S: ¼ sheet @ $8 per sheet 2.00 L: ½ sheet @ $8 per sheet 4.00 Direct labor: .1 hour @ $20 2.00 2.00 Manufacturing overhead: .1 hour @ $10 1.00 1.00 Total manufacturing cost per unit $7.00 $10.00 Manufacturing equipment depreciation is $20,000 per quarter. Photo Artistry’s quarterly selling and administrative expenses are $100,000, paid in The company rents all its administrative office space and equipment. Thus, there is no depreciation related to the administrative functions of the company. The $1,000,000 loan from Shark Bank and Trust Company will be received on January 1, 20x2. Photo Artistry will use all the money immediately to purchase new equipment. Interest payments will be made at the end of each quarter. Loan principal will be paid in four equal installments of $250,000 at the end of each quarter. Jackson anticipates that dividends of $50,000 will be declared and paid in cash each quarter. Photo Artistry’s projected balance sheet as of December 31, 20x1, follows: Cash $ 95,000 Accounts receivable 132,000 Inventory: Raw material 59,200 Finished goods 167,000 Plant and equipment, net 8,000,000 Total assets $ 8,453,200 Accounts payable $ 99,400 Common stock 5,000,000

Master Budget

A master budget can be defined as an estimation of the revenue earned or expenses incurred over a specified period of time in the future and it is generally prepared on a periodic basis which can be either monthly, quarterly, half-yearly, or annually. It helps a business, an organization, or even an individual to manage the money effectively. A budget also helps in monitoring the performance of the people in the organization and helps in better decision-making.

Sales Budget and Selling

A budget is a financial plan designed by an undertaking for a definite period in future which acts as a major contributor towards enhancing the financial success of the business undertaking. The budget generally takes into account both current and future income and expenses.

Jay Rexford, president of Photo Artistry Company, was just concluding a budget meeting with his senior staff. It was November of 20x1, and the group was discussing preparation of the firm’s

In response to a question about financing the acquisition, Rexford replied as follows: “The robot will cost $950,000. There will also be an additional $50,000 in ancillary equipment to be purchased. We’ll finance these purchases with a one‑year $1,000,000 loan from Shark Bank and Trust Company. I’ve negotiated a repayment schedule of four equal installments on the last day of each quarter. The interest rate will be 10 percent, and interest payments will be quarterly as well.” With that the meeting broke up, and the budget process was on.

Photo Artistry Company is a manufacturer of metal picture frames. The firm’s two product lines are designated as S (small frames; 5 × 7 inches) and L (large frames; 8 × 10 inches). The primary raw materials are flexible metal strips and 9‑inch by 24‑inch glass sheets. Each S frame requires a 2‑foot metal strip; an L frame requires a 3‑foot metal strip. Allowing for normal breakage and scrap glass, the company can get either four S frames or two L frames out of a glass sheet. Other raw materials, such as cardboard backing, are insignificant in cost and are treated as indirect materials. Emily Jackson, Photo Artistry's controller, is in charge of preparing the master budget for 20x2. She has gathered the following information:

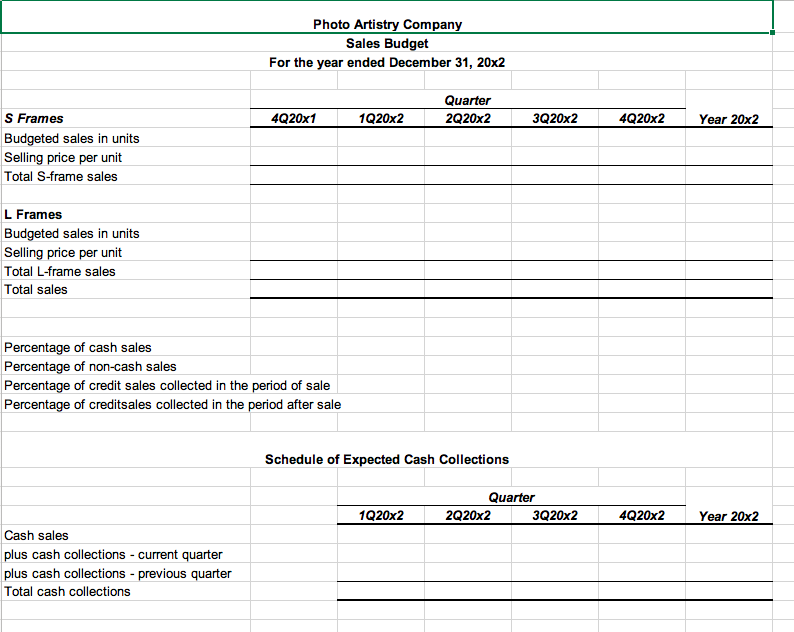

- Sales in the 4th quarter of 20x1 are expected to be 50,000 S frames and 40,000 L frames. The sales manager predicts that over the next 2 years, sales in each product line will grow by 5,000 units each quarter over the previous quarter. For example, S frame sales in the 1st quarter of 20x2 are expected to be 55,000 units.

- Photo Artistry's sales history indicates that 60% of all sales are on credit, with the remainder of the sales in cash. The company’s collection experience shows that 80% of the credit sales are collected during the quarter in which the sale is made, while the remaining 20% is collected in the, following quarter. For simplicity, assume the company is able to collect 100% of its

accounts receivable .

- The S frame sells for $10, and the L frame sells for $15. These prices are expected to hold constant throughout 20x2.

- The production manager attempts to end each quarter with enough finished‑goods inventory in each product line to cover 20% of the following quarter’s sales.

- Photo Artistry makes an attempt to end each quarter with 20% of the glass sheets needed for the following quarter's production. The company wants to have an inventory of 10,400 sheets at the end of 20x2.

- Metal strips are purchased locally and the company buys them on a just‑in‑time basis. Inventory of metal strips is negligible.

- All direct‑material purchases are made on account, and 80% of each quarter’s purchases are paid in cash during the same quarter as the purchase. The other 20% is paid in the next quarter.

- Indirect materials are purchased with cash as needed. Work‑in‑process is negligible.

- Projected

manufacturing costs in 20x2 are as follow:

|

|

S Frame |

|

L Frame |

|

Direct material: |

|

|

|

|

Metal strips: |

|

|

|

|

S: 2 ft. @ $1 per foot |

$2.00 |

|

|

|

L: 3 ft. @ $1 per foot |

|

|

$3.00 |

|

Glass sheets: |

|

|

|

|

S: ¼ sheet @ $8 per sheet |

2.00 |

|

|

|

L: ½ sheet @ $8 per sheet |

|

|

4.00 |

|

Direct labor: |

|

|

|

|

.1 hour @ $20 |

2.00 |

|

2.00 |

|

Manufacturing overhead: |

|

|

|

|

.1 hour @ $10 |

1.00 |

|

1.00 |

|

Total manufacturing cost per unit |

$7.00 |

|

$10.00 |

- Manufacturing equipment

depreciation is $20,000 per quarter.

- Photo Artistry’s quarterly selling and administrative expenses are $100,000, paid in The company rents all its administrative office space and equipment. Thus, there is no depreciation related to the administrative functions of the company.

- The $1,000,000 loan from Shark Bank and Trust Company will be received on January 1, 20x2. Photo Artistry will use all the money immediately to purchase new equipment. Interest payments will be made at the end of each quarter. Loan principal will be paid in four equal installments of $250,000 at the end of each quarter.

- Jackson anticipates that dividends of $50,000 will be declared and paid in cash each quarter.

- Photo Artistry’s projected balance sheet as of December 31, 20x1, follows:

|

Cash |

$ 95,000 |

|

Accounts receivable |

132,000 |

|

Inventory: |

|

|

Raw material |

59,200 |

|

Finished goods |

167,000 |

|

Plant and equipment, net |

8,000,000 |

|

Total assets |

$ 8,453,200 |

|

Accounts payable |

$ 99,400 |

|

Common stock |

5,000,000 |

|

|

3,353,800 |

|

Total liabilities and |

$ 8,453,200 |

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images