Let W(t) be Brownian motion. Using Ito's lemma evaluate | (4w (t) – 124W (t))dW(t)

Linear Algebra: A Modern Introduction

4th Edition

ISBN:9781285463247

Author:David Poole

Publisher:David Poole

Chapter4: Eigenvalues And Eigenvectors

Section4.6: Applications And The Perron-frobenius Theorem

Problem 70EQ

Related questions

Question

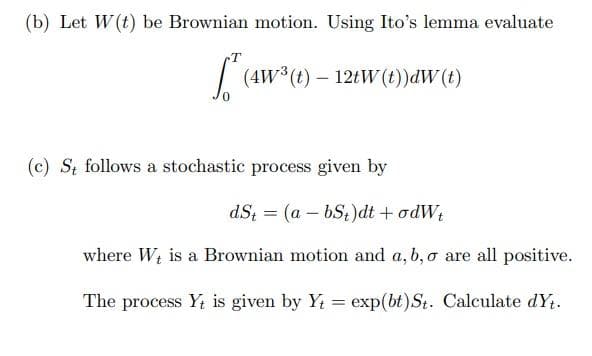

Transcribed Image Text:(b) Let W(t) be Brownian motion. Using Ito's lemma evaluate

| (4w*(t) – 121W (t))dW(t)

(c) St follows a stochastic process given by

dS; = (a – bS;)dt + odW;

where Wt is a Brownian motion and a, b, o are all positive.

The process Y; is given by Y = exp(bt)St. Calculate dYt.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Recommended textbooks for you

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning