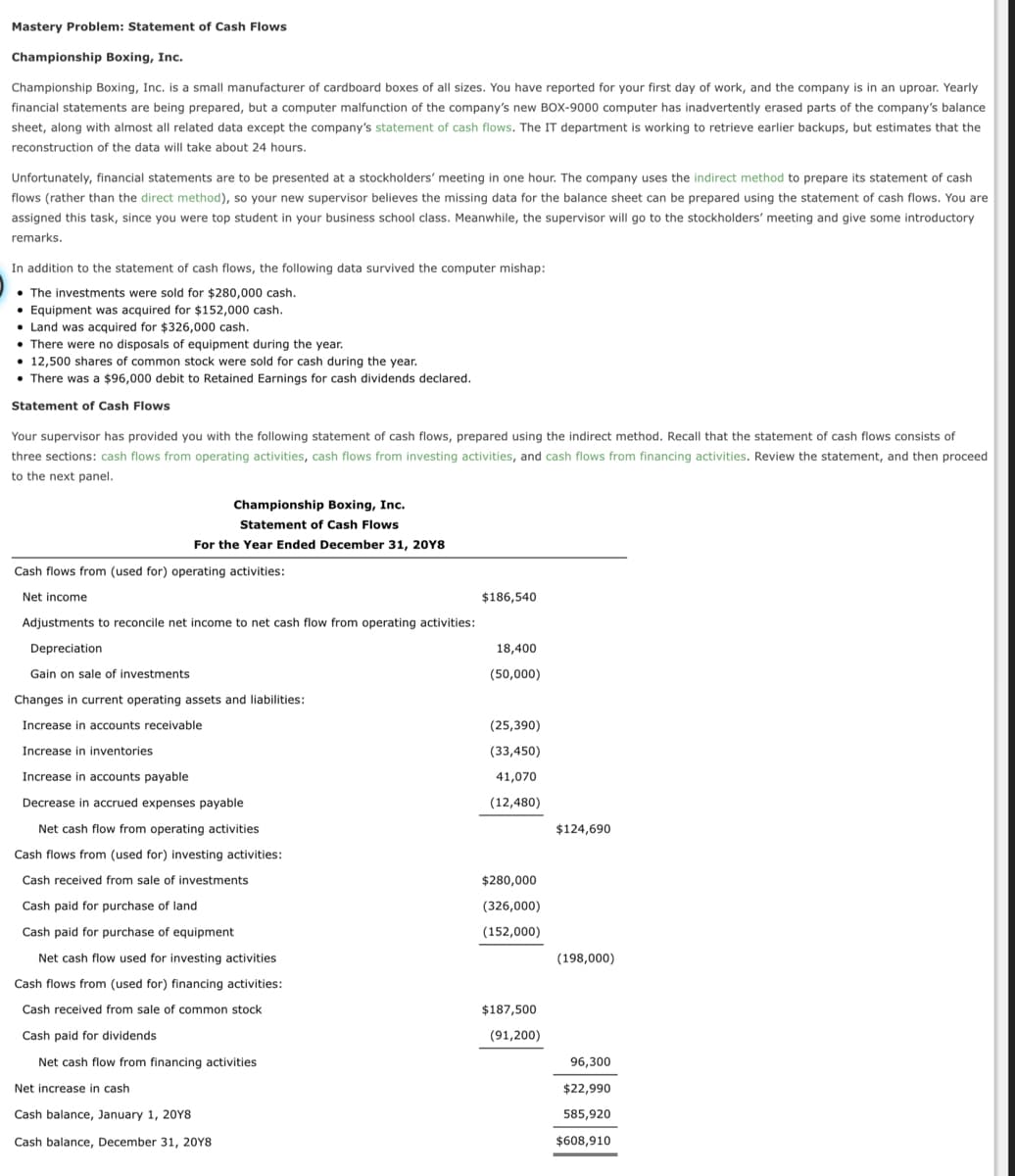

Mastery Problem: Statement of Cash Flows Championship Boxing, Inc. Championship Boxing, Inc. is a small manufacturer of cardboard boxes of all sizes. You have reported for your first day of work, and the company is in an uproar. Yearly financial statements are being prepared, but a computer malfunction of the company's new BOX-9000 computer has inadvertently erased parts of the company's balance sheet, along with almost all related data except the company's statement of cash flows. The IT department is working to retrieve earlier backups, but estimates that the reconstruction of the data will take about 24 hours. Unfortunately, financial statements are to be presented at a stockholders' meeting in one hour. The company uses the indirect method to prepare its statement of cash flows (rather than the direct method), so your new supervisor believes the missing data for the balance sheet can be prepared using the statement of cash flows. You are assigned this task, since you were top student in your business school class. Meanwhile, the supervisor will go to the stockholders' meeting and give some introductory remarks. In addition to the statement of cash flows, the following data survived the computer mishap: • The investments were sold for $280,000 cash. • Equipment was acquired for $152,000 cash. • Land was acquired for $326,000 cash. • There were no disposals of equipment during the year. • 12,500 shares of common stock were sold for cash during the year. • There was a $96,000 debit to Retained Earnings for cash dividends declared. Statement of Cash Flows Your supervisor has provided you with the following statement of cash flows, prepared using the indirect method. Recall that the statement of cash flows consists of three sections: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. Review the statement, and then proceed to the next panel. Championship Boxing, Inc. Statement of Cash Flows For the Year Ended December 31, 20Y8 Cash flows from (used for) operating activities: Net income $186,540 Adjustments to reconcile net income to net cash flow from operating activities: Depreciation 18,400 Gain on sale of investments (50,000) Changes in current operating assets and liabilities: Increase in accounts receivable (25,390) Increase in inventories (33,450) Increase in accounts payable 41,070 Decrease in accrued expenses payable (12,480) Net cash flow from operating activities $124,690 Cash flows from (used for) investing activities: Cash received from sale of investments $280,000 Cash paid for purchase of land (326,000) Cash paid for purchase of equipment (152,000) Net cash flow used for investing activities (198,000) Cash flows from (used for) financing activities: Cash received from sale of common stock $187,500 Cash paid for dividends (91,200) Net cash flow from financing activities 96,300 Net increase in cash $22,990 Cash balance, January 1, 20Y8 585,920 Cash balance, December 31, 20Y8 $608,910

Mastery Problem: Statement of Cash Flows Championship Boxing, Inc. Championship Boxing, Inc. is a small manufacturer of cardboard boxes of all sizes. You have reported for your first day of work, and the company is in an uproar. Yearly financial statements are being prepared, but a computer malfunction of the company's new BOX-9000 computer has inadvertently erased parts of the company's balance sheet, along with almost all related data except the company's statement of cash flows. The IT department is working to retrieve earlier backups, but estimates that the reconstruction of the data will take about 24 hours. Unfortunately, financial statements are to be presented at a stockholders' meeting in one hour. The company uses the indirect method to prepare its statement of cash flows (rather than the direct method), so your new supervisor believes the missing data for the balance sheet can be prepared using the statement of cash flows. You are assigned this task, since you were top student in your business school class. Meanwhile, the supervisor will go to the stockholders' meeting and give some introductory remarks. In addition to the statement of cash flows, the following data survived the computer mishap: • The investments were sold for $280,000 cash. • Equipment was acquired for $152,000 cash. • Land was acquired for $326,000 cash. • There were no disposals of equipment during the year. • 12,500 shares of common stock were sold for cash during the year. • There was a $96,000 debit to Retained Earnings for cash dividends declared. Statement of Cash Flows Your supervisor has provided you with the following statement of cash flows, prepared using the indirect method. Recall that the statement of cash flows consists of three sections: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. Review the statement, and then proceed to the next panel. Championship Boxing, Inc. Statement of Cash Flows For the Year Ended December 31, 20Y8 Cash flows from (used for) operating activities: Net income $186,540 Adjustments to reconcile net income to net cash flow from operating activities: Depreciation 18,400 Gain on sale of investments (50,000) Changes in current operating assets and liabilities: Increase in accounts receivable (25,390) Increase in inventories (33,450) Increase in accounts payable 41,070 Decrease in accrued expenses payable (12,480) Net cash flow from operating activities $124,690 Cash flows from (used for) investing activities: Cash received from sale of investments $280,000 Cash paid for purchase of land (326,000) Cash paid for purchase of equipment (152,000) Net cash flow used for investing activities (198,000) Cash flows from (used for) financing activities: Cash received from sale of common stock $187,500 Cash paid for dividends (91,200) Net cash flow from financing activities 96,300 Net increase in cash $22,990 Cash balance, January 1, 20Y8 585,920 Cash balance, December 31, 20Y8 $608,910

Financial Reporting, Financial Statement Analysis and Valuation

8th Edition

ISBN:9781285190907

Author:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Chapter3: Income Flows Versus Cash Flows: Understanding The Statement Of Cash Flow

Section: Chapter Questions

Problem 27PC: Preparing a Statement of Cash Flows from Balance Sheets and Income Statements. BTB Electronics Inc....

Related questions

Question

Transcribed Image Text:Mastery Problem: Statement of Cash Flows

Championship Boxing, Inc.

Championship Boxing, Inc. is a small manufacturer of cardboard boxes of all sizes. You have reported for your first day of work, and the company is in an uproar. Yearly

financial statements are being prepared, but a computer malfunction of the company's new BOX-9000 computer has inadvertently erased parts of the company's balance

sheet, along with almost all related data except the company's statement of cash flows. The IT department is working to retrieve earlier backups, but estimates that the

reconstruction of the data will take about 24 hours.

Unfortunately, financial statements are to be presented at a stockholders' meeting in one hour. The company uses the indirect method to prepare its statement of cash

flows (rather than the direct method), so your new supervisor believes the missing data for the balance sheet can be prepared using the statement of cash flows. You are

assigned this task, since you were top student in your business school class. Meanwhile, the supervisor will go to the stockholders' meeting and give some introductory

remarks.

In addition to the statement of cash flows, the following data survived the computer mishap:

• The investments were sold for $280,000 cash.

• Equipment was acquired for $152,000 cash.

• Land was acquired for $326,000 cash.

• There were no disposals of equipment during the year.

• 12,500 shares of common stock were sold for cash during the year.

• There was a $96,000 debit to Retained Earnings for cash dividends declared.

Statement of Cash Flows

Your supervisor has provided you with the following statement of cash flows, prepared using the indirect method. Recall that the statement of cash flows consists of

three sections: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. Review the statement, and then proceed

to the next panel.

Championship Boxing, Inc.

Statement of Cash Flows

For the Year Ended December 31, 20Y8

Cash flows from (used for) operating activities:

Net income

$186,540

Adjustments to reconcile net income to net cash flow from operating activities:

Depreciation

18,400

Gain on sale of investments

(50,000)

Changes in current operating assets and liabilities:

Increase in accounts receivable

(25,390)

Increase in inventories

(33,450)

Increase in accounts payable

41,070

Decrease in accrued expenses payable

(12,480)

Net cash flow from operating activities

$124,690

Cash flows from (used for) investing activities:

Cash received from sale of investments

$280,000

Cash paid for purchase of land

(326,000)

Cash paid for purchase of equipment

(152,000)

Net cash flow used for investing activities

(198,000)

Cash flows from (used for) financing activities:

Cash received from sale of common stock

$187,500

Cash paid for dividends

(91,200)

Net cash flow from financing activities

96,300

Net increase in cash

$22,990

Cash balance, January 1, 20Y8

585,920

Cash balance, December 31, 20Y8

$608,910

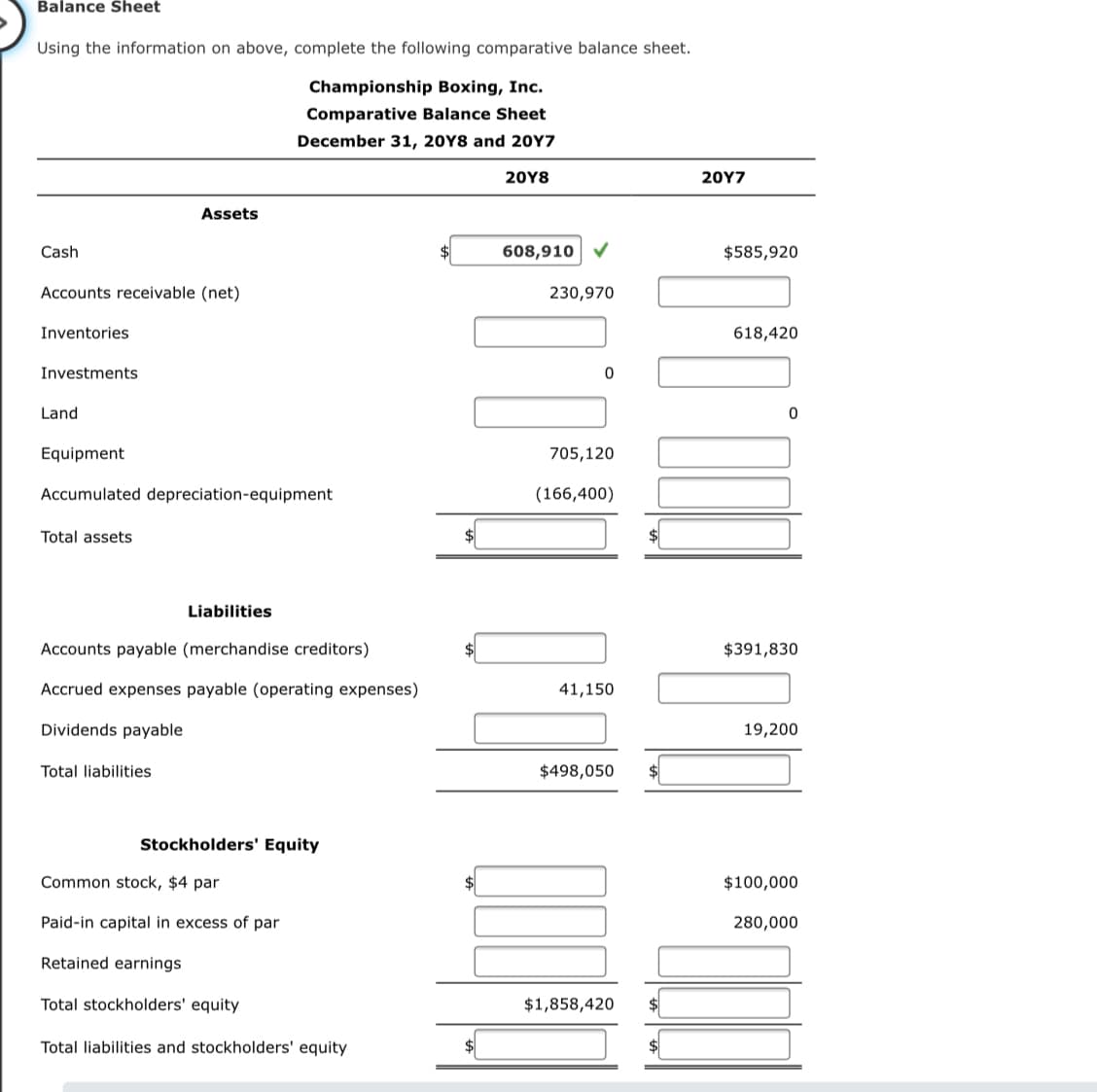

Transcribed Image Text:Balance Sheet

Using the information on above, complete the following comparative balance sheet.

Championship Boxing, Inc.

Comparative Balance Sheet

December 31, 20Y8 and 20Y7

20Υ8

20Y7

Assets

Cash

$

608,910

$585,920

Accounts receivable (net)

230,970

Inventories

618,420

Investments

Land

Equipment

705,120

Accumulated depreciation-equipment

(166,400)

Total assets

Liabilities

Accounts payable (merchandise creditors)

$391,830

Accrued expenses payable (operating expenses)

41,150

Dividends payable

19,200

Total liabilities

$498,050

Stockholders' Equity

Common stock, $4 par

$100,000

Paid-in capital in excess of par

280,000

Retained earnings

Total stockholders' equity

$1,858,420

$

Total liabilities and stockholders' equity

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning