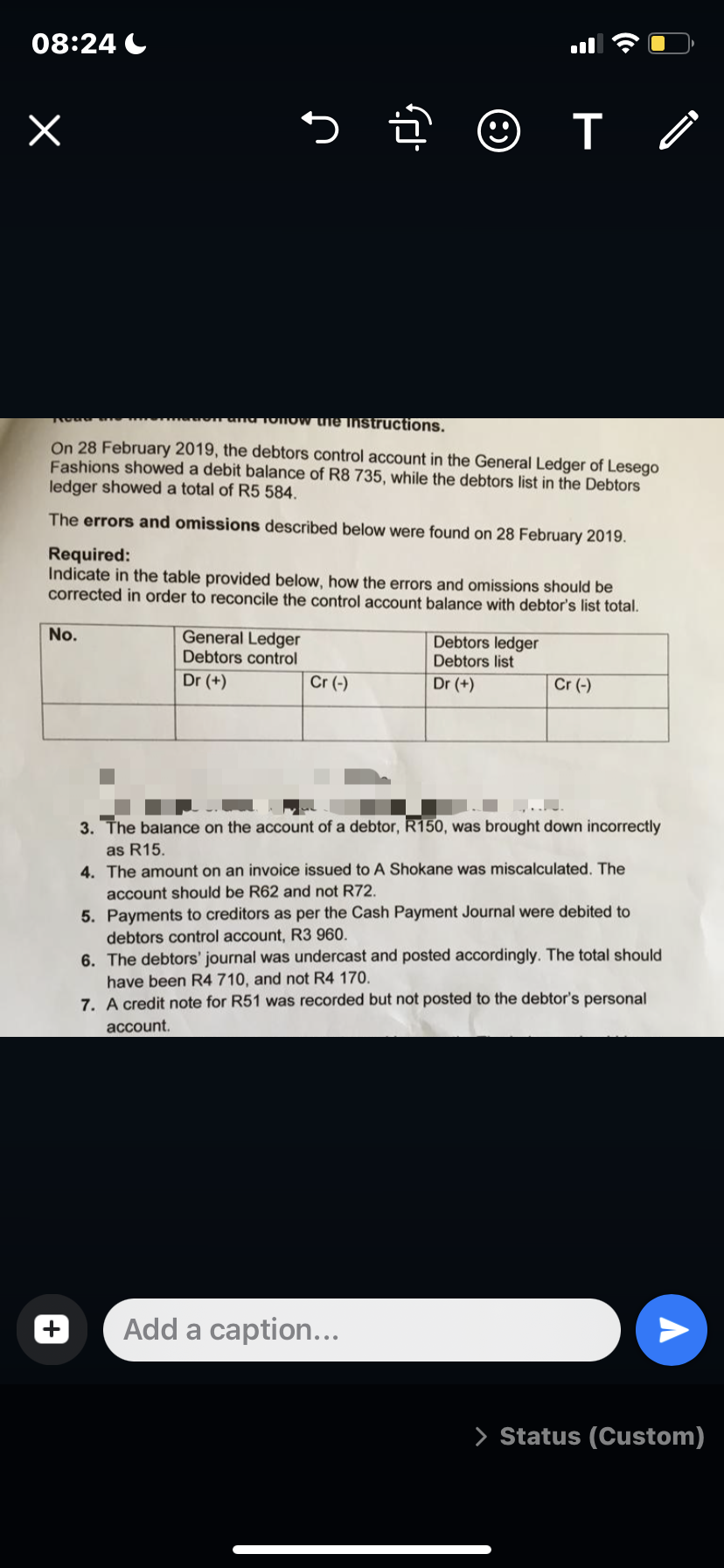

On 28 February 2019, the debtors control account in the General Ledger of Lesego Fashions showed a debit balance of R8 735, while the debtors list in the Debtors ledger showed a total of R5 584. The errors and omissions described below were found on 28 February 2019. Required: Indicate in the table provided below, how the errors and omissions should be corrected in order to reconcile the control account balance with debtor's list total. No. General Ledger Debtors control Debtors ledger Debtors list Dr (+) Cr (-) Dr (+) Cr (-) 3. The balance on the account of a debtor, R150, was brought down incorrectly as R15. 4. The amount on an invoice issued to A Shokane was miscalculated. The account should be R62 and not R72. 5. Payments to creditors as per the Cash Payment Journal were debited to debtors control account, R3 960. 6. The debtors' journal was undercast and posted accordingly. The total should have been R4 710, and not R4 170. 7. A credit note for R51 was recorded but not posted to the debtor's personal account.

Bad Debts

At the end of the accounting period, a financial statement is prepared by every company, then at that time while preparing the financial statement, the company determines among its total receivable amount how much portion of receivables is collected by the company during that accounting period.

Accounts Receivable

The word “account receivable” means the payment is yet to be made for the work that is already done. Generally, each and every business sells its goods and services either in cash or in credit. So, when the goods are sold on credit account receivable arise which means the company is going to get the payment from its customer to whom the goods are sold on credit. Usually, the credit period may be for a very short period of time and in some rare cases it takes a year.

Step by step

Solved in 3 steps