On January 1, Year 4, Grant Corporation bought 8,000 (80%) of the outstanding common shares of Lee Company for $70,000 cash. On that date, Lee had $25,000 of common shares outstanding and $30,000 retained earnings. Also on that date, the carrying amount of each of Lee's identifiable assets and liabilities was equal to its fair value except for the following: The patent had an estimated useful life of 5 years at January 1, Year 4, and the entire inventory was sold during Year 4. Grant uses the cost method to account for its investment. Additional Information The recoverable (unimpaired) amount for goodwill was determined to be $10,000 on December 31, Year 6. The goodwill impairment loss occurred in Year 6. Grant's accounts receivable contains $30,000 owing from Lee. Amortization expense is grouped with distribution expenses and impairment losses are grouped with other expenses. The following are the separate-entity financial statements of Grant and Lee as of December 31, Year 6. Required: Assume Grant prepares consolidated statements under the FVE theory (also known as entity theory). Calculate the acquisition differential, goodwill and NCI at the date the two entities became related. Prepare the acquisition eliminating worksheet entry to facilitate the consolidation process on the consolidation worksheet at acquisition date. Prepare a schedule to show the amortization of acquisition differential and impairment losses since acquisition date to December 31, year 6.

On January 1, Year 4, Grant Corporation bought 8,000 (80%) of the outstanding common shares of Lee Company for $70,000 cash. On that date, Lee had $25,000 of common shares outstanding and $30,000

The patent had an estimated useful life of 5 years at January 1, Year 4, and the entire inventory was sold during Year 4. Grant uses the cost method to account for its investment.

Additional Information

- The recoverable (unimpaired) amount for

goodwill was determined to be $10,000 on December 31, Year 6. The goodwill impairment loss occurred in Year 6. - Grant's

accounts receivable contains $30,000 owing from Lee. - Amortization expense is grouped with distribution expenses and impairment losses are grouped with other expenses.

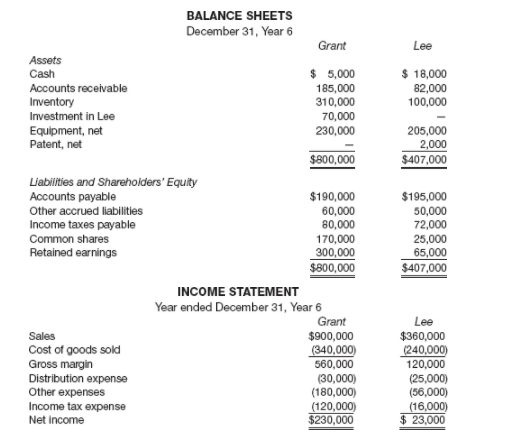

The following are the separate-entity financial statements of Grant and Lee as of December 31, Year 6.

Required: Assume Grant prepares consolidated statements under the FVE theory (also known as entity theory).

- Calculate the acquisition differential, goodwill and NCI at the date the two entities became related.

- Prepare the acquisition eliminating worksheet entry to facilitate the consolidation process on the consolidation worksheet at acquisition date.

- Prepare a schedule to show the amortization of acquisition differential and impairment losses since acquisition date to December 31, year 6.

- Calculate consolidated net income for year 6 and show attribution.

- Prepare a consolidated income statement using the direct method for year 6.

- Calculate consolidated retained earnings at December 31, year 6.

- Calculate NCI on the consolidated balance sheet at December 31, year 6 (use either method).

- Prepare the consolidated balance sheet using the direct method at December 31, year 6.

- Assume Grant used the equity method to report its investment in Lee. In this case what would be the value of the Investment in Lee account at December 31, year 6 on Grant’s separate entity balance sheet?

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images