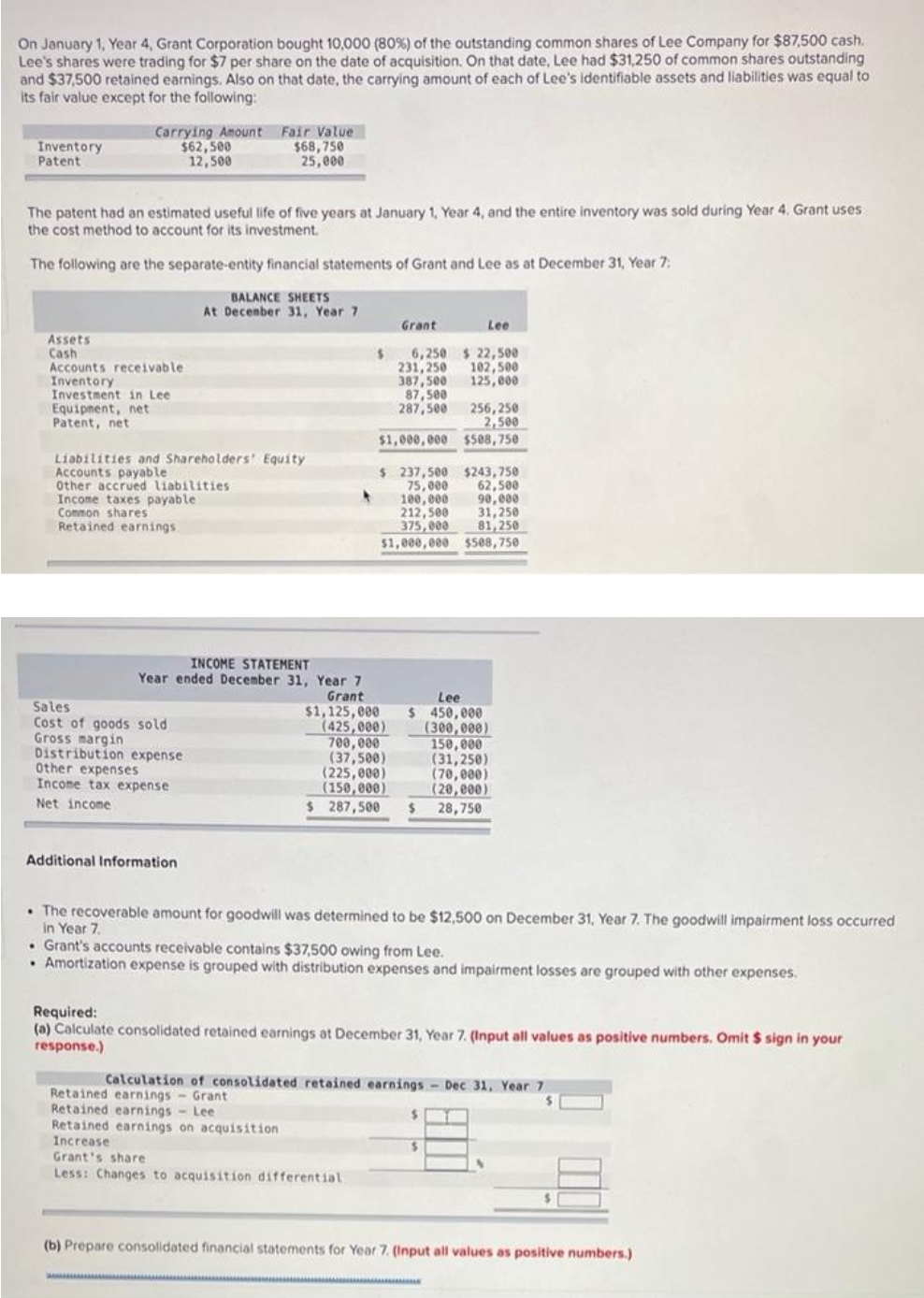

On January 1, Year 4, Grant Corporation bought 10,000 (80%) of the outstanding common shares of Lee Company for $87,500 cash. Lee's shares were trading for $7 per share on the date of acquisition. On that date, Lee had $31,250 of common shares outstanding and $37,500 retained earnings. Also on that date, the carrying amount of each of Lee's identifiable assets and liabilities was equal to its fair value except for the following: Inventory Patent Carrying Amount $62,500 12,500 Assets Cash The patent had an estimated useful life of five years at January 1, Year 4, and the entire inventory was sold during Year 4. Grant uses the cost method to account for its investment. The following are the separate-entity financial statements of Grant and Lee as at December 31, Year 7: Accounts receivable Inventory Investment in Lee Equipment, net Patent, net Liabilities and Shareholders' Equity Accounts payable Other accrued liabilities Income taxes payable: Common shares Retained earnings Sales Cost of goods sold Gross margin Distribution expense BALANCE SHEETS At December 31, Year 7 Other expenses Income tax expense Net income Fair Value $68,750 25,000 Additional Information $ INCOME STATEMENT Year ended December 31, Year 7 Grant $1,125,000 (425,000) 700,000 (37,500) (225,000) (150,000) $ 287,500 $ Grant Retained earnings - Grant Retained earnings - Lee 6,250 $22,500 102,500 125,000 231,250 387,500 Retained earnings on acquisition Increase 87,500 287,500 $1,000,000 $ 237,500 75,000 100,000 212,500 375,000 $1,000,000 Lee 256,250 2,500 $588,750 $243,750 62,500 90,000 31,250 81,250 $508,750 . The recoverable amount for goodwill was determined to be $12,500 on December 31, Year 7. The goodwill impairment loss occurred in Year 7. Lee $ 450,000 (300,000) 150,000 (31,250) (70,000) (20,000) 28,750 • Grant's accounts receivable contains $37,500 owing from Lee. . Amortization expense is grouped with distribution expenses and impairment losses are grouped with other expenses. Required: (a) Calculate consolidated retained earnings at December 31, Year 7. (Input all values as positive numbers. Omit $ sign in your response.) Calculation of consolidated retained earnings- Dec 31, Year 7

On January 1, Year 4, Grant Corporation bought 10,000 (80%) of the outstanding common shares of Lee Company for $87,500 cash. Lee's shares were trading for $7 per share on the date of acquisition. On that date, Lee had $31,250 of common shares outstanding and $37,500 retained earnings. Also on that date, the carrying amount of each of Lee's identifiable assets and liabilities was equal to its fair value except for the following: Inventory Patent Carrying Amount $62,500 12,500 Assets Cash The patent had an estimated useful life of five years at January 1, Year 4, and the entire inventory was sold during Year 4. Grant uses the cost method to account for its investment. The following are the separate-entity financial statements of Grant and Lee as at December 31, Year 7: Accounts receivable Inventory Investment in Lee Equipment, net Patent, net Liabilities and Shareholders' Equity Accounts payable Other accrued liabilities Income taxes payable: Common shares Retained earnings Sales Cost of goods sold Gross margin Distribution expense BALANCE SHEETS At December 31, Year 7 Other expenses Income tax expense Net income Fair Value $68,750 25,000 Additional Information $ INCOME STATEMENT Year ended December 31, Year 7 Grant $1,125,000 (425,000) 700,000 (37,500) (225,000) (150,000) $ 287,500 $ Grant Retained earnings - Grant Retained earnings - Lee 6,250 $22,500 102,500 125,000 231,250 387,500 Retained earnings on acquisition Increase 87,500 287,500 $1,000,000 $ 237,500 75,000 100,000 212,500 375,000 $1,000,000 Lee 256,250 2,500 $588,750 $243,750 62,500 90,000 31,250 81,250 $508,750 . The recoverable amount for goodwill was determined to be $12,500 on December 31, Year 7. The goodwill impairment loss occurred in Year 7. Lee $ 450,000 (300,000) 150,000 (31,250) (70,000) (20,000) 28,750 • Grant's accounts receivable contains $37,500 owing from Lee. . Amortization expense is grouped with distribution expenses and impairment losses are grouped with other expenses. Required: (a) Calculate consolidated retained earnings at December 31, Year 7. (Input all values as positive numbers. Omit $ sign in your response.) Calculation of consolidated retained earnings- Dec 31, Year 7

Chapter13: Comparative Forms Of Doing Business

Section: Chapter Questions

Problem 44P

Related questions

Question

Transcribed Image Text:On January 1, Year 4, Grant Corporation bought 10,000 (80%) of the outstanding common shares of Lee Company for $87,500 cash.

Lee's shares were trading for $7 per share on the date of acquisition. On that date, Lee had $31,250 of common shares outstanding

and $37,500 retained earnings. Also on that date, the carrying amount of each of Lee's identifiable assets and liabilities was equal to

its fair value except for the following:

Inventory

Patent

Carrying Amount

$62,500

12,500

Assets

Cash

The patent had an estimated useful life of five years at January 1, Year 4, and the entire inventory was sold during Year 4. Grant uses

the cost method to account for its investment.

The following are the separate-entity financial statements of Grant and Lee as at December 31, Year 7:

Accounts receivable

Inventory

Investment in Lee

Equipment, net

Patent, net

Liabilities and Shareholders' Equity

Accounts payable

Other accrued liabilities

Income taxes payable:

Common shares

Retained earnings

Fair Value

$68,750

25,000

Sales

Cost of goods sold

Gross margin

Distribution expense

BALANCE SHEETS

At December 31, Year 7

Other expenses

Income tax expense

Net income

Additional Information

INCOME STATEMENT

Year ended December 31, Year 7

Grant

$1,125,000

$

(425,000)

700,000

(37,500)

(225,000)

(150,000)

$ 287,500

Grant

87,500

287,500

$1,000,000

$ 237,500 $243,750

75,000

62,500

90,000

31,250

81,250

$1,000,000 $508,750

6,250

231,250

$22,500

102,500

387,500 125,000

Retained earnings on acquisition

Increase

Grant's share

Less: Changes to acquisition differential.

100,000

212,500

375,000

Lee

Lee

$450,000

256,250

2,500

$508,750

The recoverable amount for goodwill was determined to be $12,500 on December 31, Year 7. The goodwill impairment loss occurred

in Year 7.

Grant's accounts receivable contains $37,500 owing from Lee.

. Amortization expense is grouped with distribution expenses and impairment losses are grouped with other expenses.

(300,000)

150,000

(31,250)

(70,000)

(20,000)

28,750

Required:

(a) Calculate consolidated retained earnings at December 31, Year 7. (Input all values as positive numbers. Omit $ sign in your

response.)

$

Calculation of consolidated retained earnings- Dec 31, Year 7

Retained earnings - Grant

$

Retained earnings

Lee

$

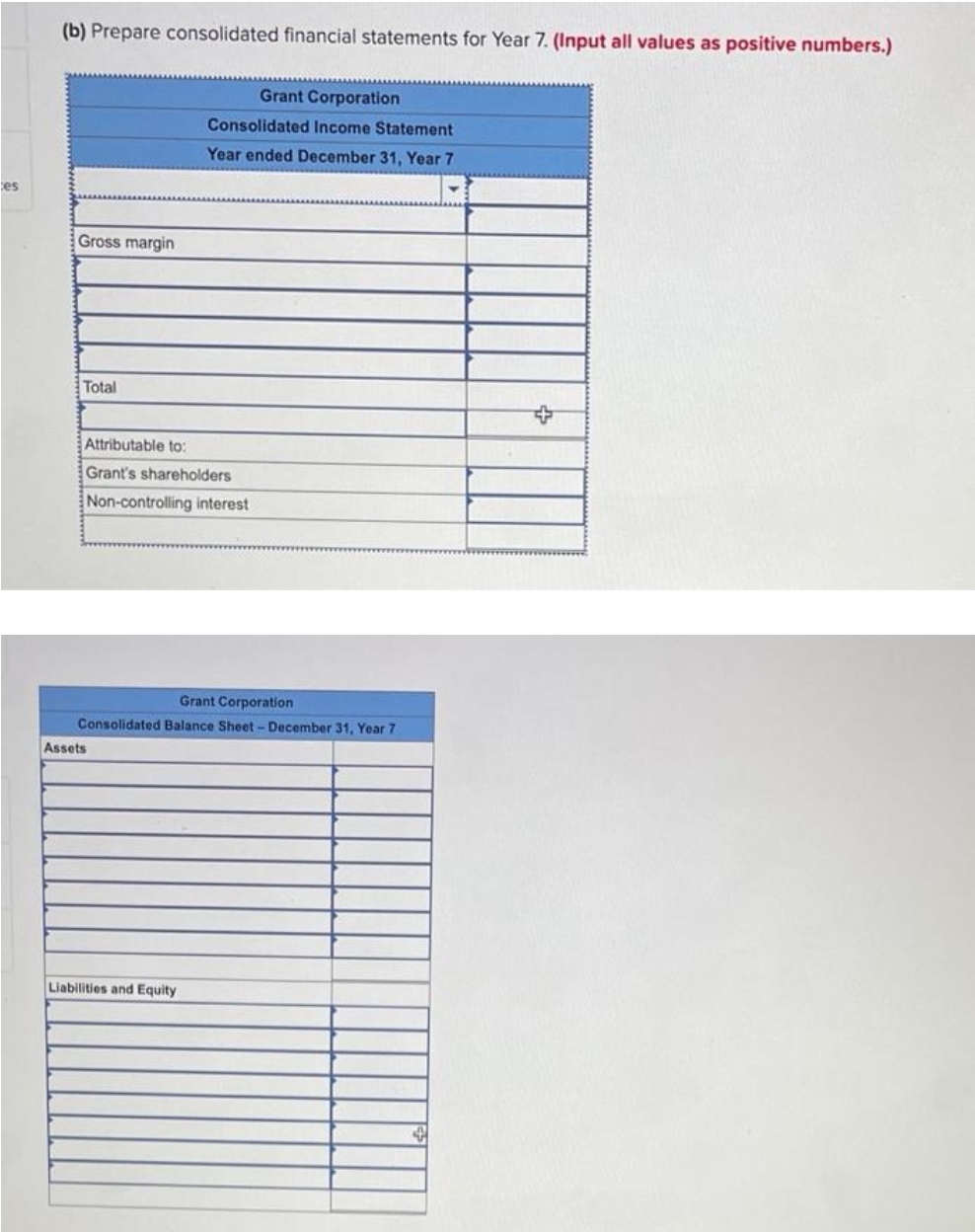

(b) Prepare consolidated financial statements for Year 7. (Input all values as positive numbers.)

Transcribed Image Text:es

(b) Prepare consolidated financial statements for Year 7. (Input all values as positive numbers.)

Gross margin

Total

Attributable to:

Grant's shareholders

Non-controlling interest

Grant Corporation

Consolidated Income Statement

Year ended December 31, Year 7

Grant Corporation

Consolidated Balance Sheet- December 31, Year 7

Assets

Liabilities and Equity

4

+

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning