On January 5, 20x9, Parent Company acquired 80% of the outstanding shares of Subsidiary Company for P350,000. The financial statements of Parent and Subsidiary Company before the acquisition follow: Subsidiary Parent Company Company Value 100,000 100,000 50,000 Parent Cash 700,000 300,000 1,000,000 500,000 1,000,000 500,000 Inventory 55,000 350,000 365,000 200,000 200,000 200,000 100,000 PPE Liabilities Outstanding Shares Retained eamings Financial statements for Parent and Subsidiary for the year ended December 31, 2x19 follow: AdditionalInfomation: The undervahued PPE of Subsidiary on the date of acquisition has a remaining useful life of 5-years. Subsidiary Company owes Parent Company P5,000 on December 31, 2x19.

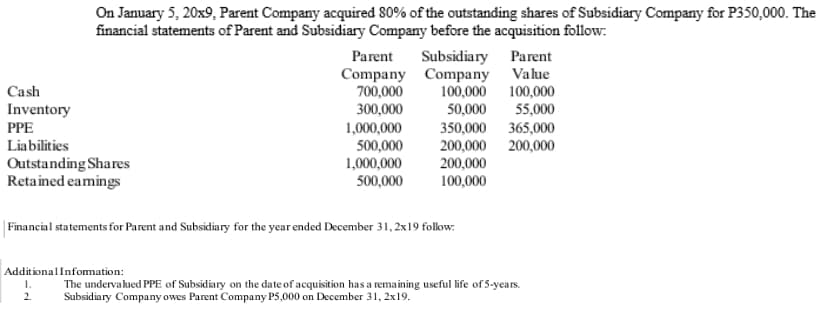

On January 5, 20x9, Parent Company acquired 80% of the outstanding shares of Subsidiary Company for P350,000. The financial statements of Parent and Subsidiary Company before the acquisition follow: Subsidiary Parent Company Company Value 100,000 100,000 50,000 Parent Cash 700,000 300,000 1,000,000 500,000 1,000,000 500,000 Inventory 55,000 350,000 365,000 200,000 200,000 200,000 100,000 PPE Liabilities Outstanding Shares Retained eamings Financial statements for Parent and Subsidiary for the year ended December 31, 2x19 follow: AdditionalInfomation: The undervahued PPE of Subsidiary on the date of acquisition has a remaining useful life of 5-years. Subsidiary Company owes Parent Company P5,000 on December 31, 2x19.

Chapter20: Corporations: Distributions In Complete Liquidation And An Overview Of Reorganizations

Section: Chapter Questions

Problem 38P

Related questions

Question

Prepare the related eliminating entries on January 1, 20x9 and December 31, 20x19

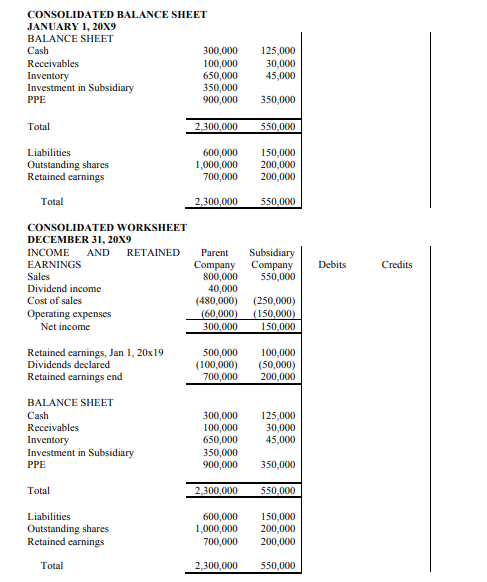

Transcribed Image Text:CONSOLIDATED BALANCE SHEET

JANUARY 1, 20X9

BALANCE SHEET

Cash

Receivables

300,000

100,000

650,000

350,000

900,000

125,000

30,000

45,000

Inventory

Investment in Subsidiary

PPE

350,000

Total

2,300,000

550,000

Liabilities

Outstanding shares

Retained earnings

600,000

1,000,000

700,000

150,000

200,000

200,000

Total

2,300,000

550,000

CONSOLIDATED WORKSHEET

DECEMBER 31, 20X9

INCOME

AND

RETAINED

Parent

Subsidiary

Company

550,000

EARNINGS

Debits

Credits

Company

800,000

40,000

(480,000)

Sales

Dividend income

Cost of sales

(250,000)

(150,000)

150,000

Operating expenses

(60,000)

300,000

Net income

Retained earnings, Jan 1, 20x19

500,000

(100,000)

700,000

100,000

(50,000)

200,000

Dividends declared

Retained earnings end

BALANCE SHEET

Cash

300,000

100,000

650,000

350,000

900,000

125,000

30,000

45,000

Receivables

Inventory

Investment in Subsidiary

PPE

350,000

Total

2,300,000

550,000

600,000

1,000,000

700,000

Liabilities

150,000

200,000

Outstanding shares

Retained earnings

200,000

Total

2,300,000

550,000

Transcribed Image Text:On January 5, 20x9, Parent Company acquired 80% of the outstanding shares of Subsidiary Company for P350,000. The

financial statements of Parent and Subsidiary Company before the acquisition follow:

Parent

Subsidiary Parent

Company Company Value

700,000

300,000

1,000,000

500,000

1,000,000

500,000

Cash

Inventory

PPE

100,000 100,000

50,000

55,000

350,000 365,000

200,000 200,000

200,000

100,000

Liabilities

Outstanding Shares

Retained eamings

|Financial statements for Parent and Subsidiary for the year ended December 31, 2x19 follow:

AdditionalInfomation:

The undervalued PPE of Subsidiary on the date of acquisition has a remaining useful life of 5-years.

Subsidiary Company owes Parent Company P5,000 on December 31, 2x19.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you