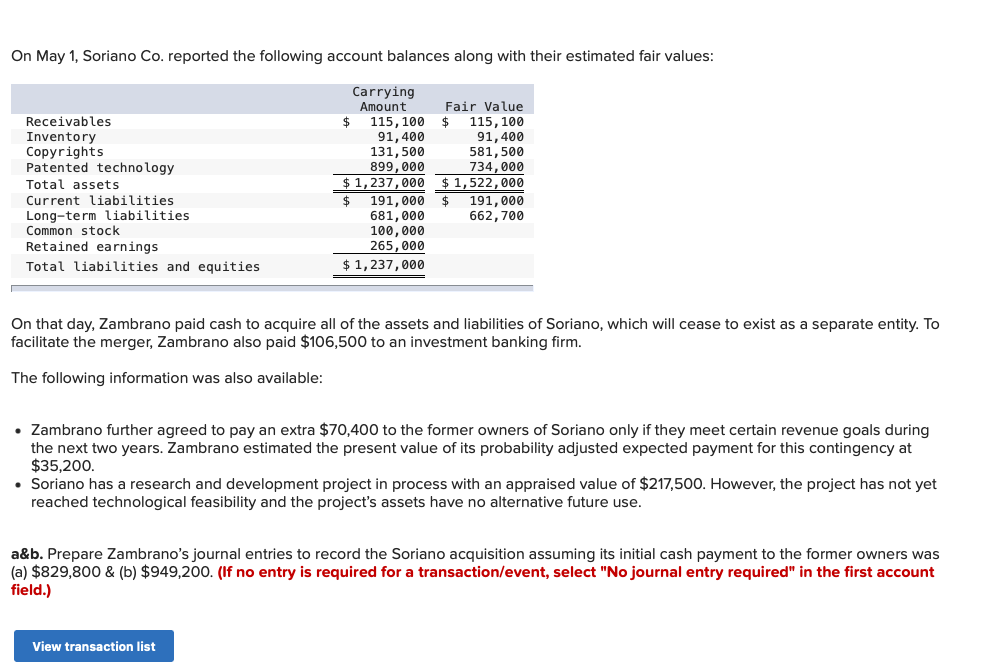

On May 1, Soriano Co. reported the following account balances along with their estimated fair values: Carrying Amount Receivables Inventory Copyrights Patented technology Total assets Current liabilities Long-term liabilities Common stock Retained earnings Total liabilities and equities Fair Value $ 115,100 $ 115,100 91,400 91,400 131,500 581,500 899,000 734,000 $1,237,000 $1,522,000 $ 191,000 $ 191,000 681,000 662,700 100,000 265,000 $ 1,237,000 On that day, Zambrano paid cash to acquire all of the assets and liabilities of Soriano, which will cease to exist as a separate entity. To facilitate the merger, Zambrano also paid $106,500 to an investment banking firm. The following information was also available: • Zambrano further agreed to pay an extra $70,400 to the former owners of Soriano only if they meet certain revenue goals during the next two years. Zambrano estimated the present value of its probability adjusted expected payment for this contingency at $35,200. • Soriano has a research and development project in process with an appraised value of $217,500. However, the project has not yet reached technological feasibility and the project's assets have no alternative future use. a&b. Prepare Zambrano's journal entries to record the Soriano acquisition assuming its initial cash payment to the former owners was (a) $829,800 & (b) $949,200. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)

On May 1, Soriano Co. reported the following account balances along with their estimated fair values: Carrying Amount Receivables Inventory Copyrights Patented technology Total assets Current liabilities Long-term liabilities Common stock Retained earnings Total liabilities and equities Fair Value $ 115,100 $ 115,100 91,400 91,400 131,500 581,500 899,000 734,000 $1,237,000 $1,522,000 $ 191,000 $ 191,000 681,000 662,700 100,000 265,000 $ 1,237,000 On that day, Zambrano paid cash to acquire all of the assets and liabilities of Soriano, which will cease to exist as a separate entity. To facilitate the merger, Zambrano also paid $106,500 to an investment banking firm. The following information was also available: • Zambrano further agreed to pay an extra $70,400 to the former owners of Soriano only if they meet certain revenue goals during the next two years. Zambrano estimated the present value of its probability adjusted expected payment for this contingency at $35,200. • Soriano has a research and development project in process with an appraised value of $217,500. However, the project has not yet reached technological feasibility and the project's assets have no alternative future use. a&b. Prepare Zambrano's journal entries to record the Soriano acquisition assuming its initial cash payment to the former owners was (a) $829,800 & (b) $949,200. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)

Survey of Accounting (Accounting I)

8th Edition

ISBN:9781305961883

Author:Carl Warren

Publisher:Carl Warren

Chapter9: Metric-analysis Of Financial Statements

Section: Chapter Questions

Problem 9.23E: Unusual income statement items Assume that the amount of each of the following items is material to...

Related questions

Question

Transcribed Image Text:On May 1, Soriano Co. reported the following account balances along with their estimated fair values:

Receivables

Inventory

Copyrights

Patented technology

Total assets

Current liabilities.

Long-term liabilities.

Common stock

Retained earnings

Total liabilities and equities

Carrying

Amount

115, 100

91, 400

131,500

899,000

$1,237,000

$

$

View transaction list

Fair Value

$

115, 100

91,400

581,500

734,000

$ 1,522,000

191,000

662,700

191,000 $

681,000

100,000

265,000

$ 1,237,000

On that day, Zambrano paid cash to acquire all of the assets and liabilities of Soriano, which will cease to exist as a separate entity. To

facilitate the merger, Zambrano also paid $106,500 to an investment banking firm.

The following information was also available:

• Zambrano further agreed to pay an extra $70,400 to the former owners of Soriano only if they meet certain revenue goals during

the next two years. Zambrano estimated the present value of its probability adjusted expected payment for this contingency at

$35,200.

Soriano has a research and development project in process with an appraised value of $217,500. However, the project has not yet

reached technological feasibility and the project's assets have no alternative future use.

a&b. Prepare Zambrano's journal entries to record the Soriano acquisition assuming its initial cash payment to the former owners was

(a) $829,800 & (b) $949,200. (If no entry is required for a transaction/event, select "No journal entry required" in the first account

field.)

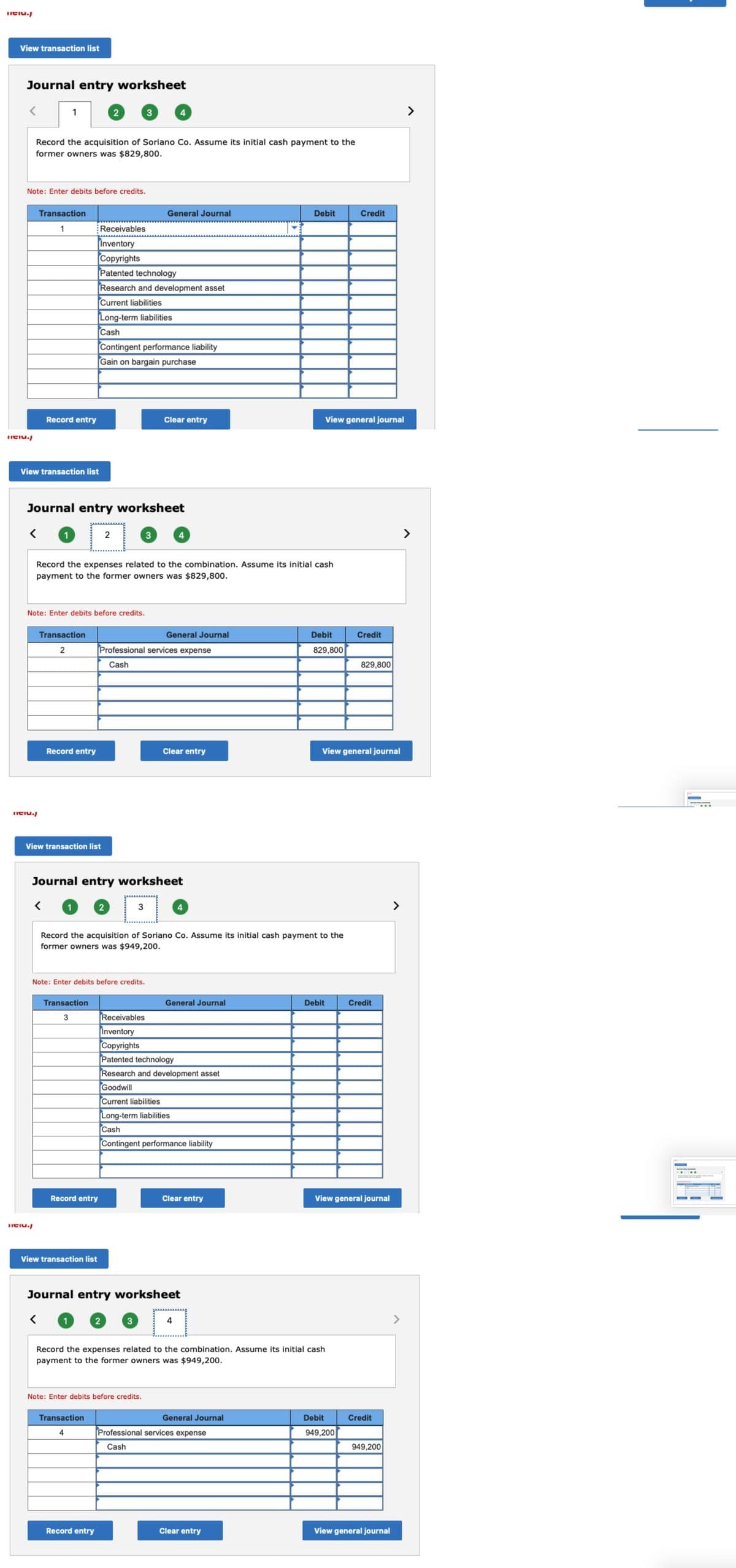

Transcribed Image Text:Titiu.

View transaction list

Journal entry worksheet

Tel./

1

Note: Enter debits before credits.

Record the acquisition of Soriano Co. Assume its initial cash payment to the

former owners was $829,800.

Transaction

1

View transaction list

Record entry

Tel./

Tel./

Transaction

2

Record entry

Note: Enter debits before credits.

Journal entry worksheet

< 1

View transaction list

2

Transaction

3

Receivables

Inventory

Copyrights

Patented technology

Record entry

View transaction list

Research and development asset

Current liabilities

Long-term liabilities

Cash

Record the expenses related to the combination. Assume its initial cash

payment to the former owners was $829,800.

Contingent performance liability

Gain on bargain purchase

2

3

Note: Enter debits before credits.

Transaction

4

2

Record entry

Journal entry worksheet

4

General Journal

3

2

3

Professional services expense

Cash

Clear entry

Note: Enter debits before credits.

4

General Journal

Record the acquisition of Soriano Co. Assume its initial cash payment to the

former owners was $949,200.

Clear entry

4

Receivables

Inventory

Copyrights

Patented technology

Research and development asset

Goodwill

Current liabilities

Long-term liabilities

Cash

Contingent performance liability

Journal entry worksheet

< 1

General Journal

4

Clear entry

Debit

General Journal

Record the expenses related to the combination. Assume its initial cash

payment to the former owners was $949,200.

Professional services expense

Cash

Clear entry

View general journal

Debit

829,800

Debit

Credit

View general journal

Credit

Debit

949,200

829,800

View general journal

Credit

Credit

949,200

View general journal

>

www.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning