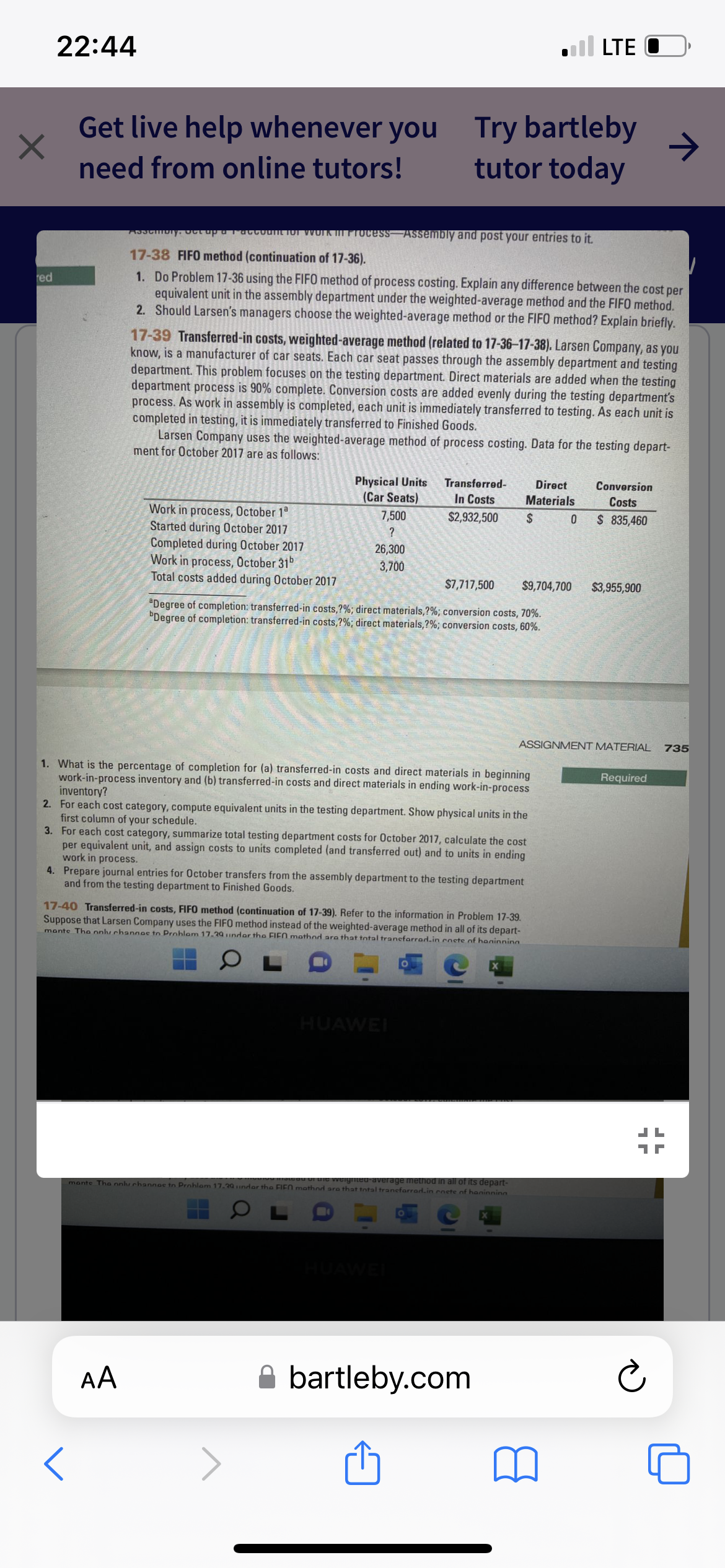

× red 22:44 Get live help whenever you need from online tutors! Work in process, October 1ª Started during October 2017 Assemory. Get up a account for work in Process Assembly and post your entries to it. 17-38 FIFO method (continuation of 17-36). 1. Do Problem 17-36 using the FIFO method of process costing. Explain any difference between the cost per equivalent unit in the assembly department under the weighted-average method and the FIFO method. 2. Should Larsen's managers choose the weighted-average method or the FIFO method? Explain briefly. 17-39 Transferred-in costs, weighted-average method (related to 17-36-17-38). Larsen Company, as you know, is a manufacturer of car seats. Each car seat passes through the assembly department and testing department. This problem focuses on the testing department. Direct materials are added when the testing department process is 90% complete. Conversion costs are added evenly during the testing department's process. As work in assembly is completed, each unit is immediately transferred to testing. As each unit is completed in testing, it is immediately transferred to Finished Goods. Larsen Company uses the weighted-average method of process costing. Data for the testing depart- ment for October 2017 are as follows: Completed during October 2017 Work in process, October 31 Total costs added during October 2017 Physical Units (Car Seats) 7,500 ? AA 26,300 3,700 Try bartleby tutor today Transferred- In Costs $2,932,500 $7,717,500 $9,704,700 "Degree of completion: transferred-in costs,?%; direct materials, ?%; conversion costs, 70%. Degree of completion: transferred-in costs,?%; direct materials, ?%; conversion costs, 60%. 1. What is the percentage of completion for (a) transferred-in costs and direct materials in beginning work-in-process inventory and (b) transferred-in costs and direct materials in ending work-in-process inventory? 2. For each cost category, compute equivalent units in the testing department. Show physical units in the first column of your schedule. 3. For each cost category, summarize total testing department costs for October 2017, calculate the cost per equivalent unit, and assign costs to units completed (and transferred out) and to units in ending work in process. 4. Prepare journal entries for October transfers from the assembly department to the testing department and from the testing department to Finished Goods. HUAWEI 17-40 Transferred-in costs, FIFO method (continuation of 17-39). Refer to the information in Problem 17-39. Suppose that Larsen Company uses the FIFO method instead of the weighted-average method in all of its depart- mante The only channes to Prohlam 17.29 under the FIFO mathod are that total tranefarrad.in enete of haninninn mante The only channes to Prohlam 17.29 indar the FIFO mothnd are that total tranefarrad.in enete of haninninn stead of the weighted average method in all of its depart- Direct Materials $ bartleby.com LTE Conversion Costs 0 $ 835,460 ASSIGNMENT MATERIAL $3,955,900 Required 17 Ć JL 735

Process Costing

Process costing is a sort of operation costing which is employed to determine the value of a product at each process or stage of producing process, applicable where goods produced from a series of continuous operations or procedure.

Job Costing

Job costing is adhesive costs of each and every job involved in the production processes. It is an accounting measure. It is a method which determines the cost of specific jobs, which are performed according to the consumer’s specifications. Job costing is possible only in businesses where the production is done as per the customer’s requirement. For example, some customers order to manufacture furniture as per their needs.

ABC Costing

Cost Accounting is a form of managerial accounting that helps the company in assessing the total variable cost so as to compute the cost of production. Cost accounting is generally used by the management so as to ensure better decision-making. In comparison to financial accounting, cost accounting has to follow a set standard ad can be used flexibly by the management as per their needs. The types of Cost Accounting include – Lean Accounting, Standard Costing, Marginal Costing and Activity Based Costing.

Step by step

Solved in 4 steps