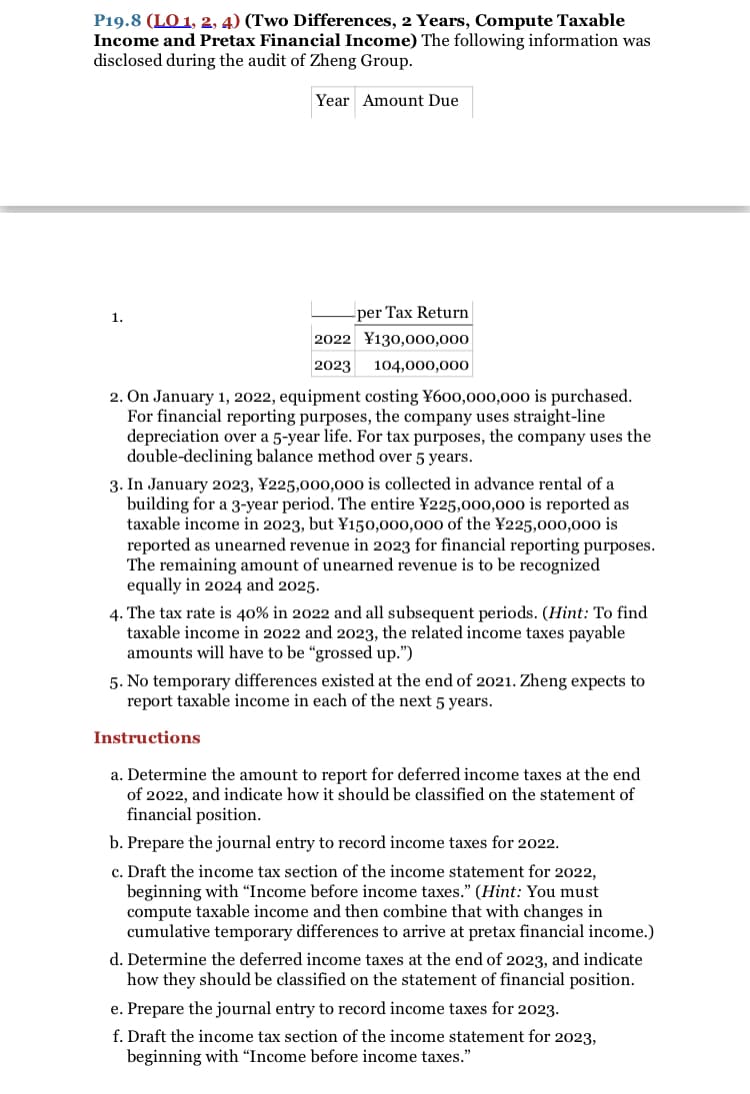

P19.8 (LO 1, 2, 4) (Two Differences, 2 Years, Compute Taxable Income and Pretax Financial Income) The following information was disclosed during the audit of Zheng Group. Year Amount Due 1. per Tax Return 2022 ¥130,000,000 2023 104,000,000 2. On January 1, 2022, equipment costing ¥600,000,000 is purchased. For financial reporting purposes, the company uses straight-line depreciation over a 5-year life. For tax purposes, the company uses the double-declining balance method over 5 years. 3. In January 2023, ¥225,000,000 is collected in advance rental of a building for a 3-year period. The entire Y225,000,000 is reported as taxable income in 2023, but Y150,000,000 of the Y225,000,000 is reported as unearned revenue in 2023 for financial reporting purposes. The remaining amount of unearned revenue is to be recognized equally in 2024 and 2025. 4. The tax rate is 40% in 2022 and all subsequent periods. (Hint: To find taxable income in 2022 and 2023, the related income taxes payable amounts will have to be "grossed up.") 5. No temporary differences existed at the end of 2021. Zheng expects to report taxable income in each of the next 5 years. Instructions a. Determine the amount to report for deferred income taxes at the end of 2022, and indicate how it should be classified on the statement of financial position. b. Prepare the journal entry to record income taxes for 2022. c. Draft the income tax section of the income statement for 2022, beginning with "Income before income taxes." (Hint: You must compute taxable income and then combine that with changes in cumulative temporary differences to arrive at pretax financial income.) d. Determine the deferred income taxes at the end of 2023, and indicate how they should be classified on the statement of financial position. e. Prepare the journal entry to record income taxes for 2023. f. Draft the income tax section of the income statement for 2023, beginning with “Income before income taxes."

P19.8 (LO 1, 2, 4) (Two Differences, 2 Years, Compute Taxable Income and Pretax Financial Income) The following information was disclosed during the audit of Zheng Group. Year Amount Due 1. per Tax Return 2022 ¥130,000,000 2023 104,000,000 2. On January 1, 2022, equipment costing ¥600,000,000 is purchased. For financial reporting purposes, the company uses straight-line depreciation over a 5-year life. For tax purposes, the company uses the double-declining balance method over 5 years. 3. In January 2023, ¥225,000,000 is collected in advance rental of a building for a 3-year period. The entire Y225,000,000 is reported as taxable income in 2023, but Y150,000,000 of the Y225,000,000 is reported as unearned revenue in 2023 for financial reporting purposes. The remaining amount of unearned revenue is to be recognized equally in 2024 and 2025. 4. The tax rate is 40% in 2022 and all subsequent periods. (Hint: To find taxable income in 2022 and 2023, the related income taxes payable amounts will have to be "grossed up.") 5. No temporary differences existed at the end of 2021. Zheng expects to report taxable income in each of the next 5 years. Instructions a. Determine the amount to report for deferred income taxes at the end of 2022, and indicate how it should be classified on the statement of financial position. b. Prepare the journal entry to record income taxes for 2022. c. Draft the income tax section of the income statement for 2022, beginning with "Income before income taxes." (Hint: You must compute taxable income and then combine that with changes in cumulative temporary differences to arrive at pretax financial income.) d. Determine the deferred income taxes at the end of 2023, and indicate how they should be classified on the statement of financial position. e. Prepare the journal entry to record income taxes for 2023. f. Draft the income tax section of the income statement for 2023, beginning with “Income before income taxes."

SWFT Essntl Tax Individ/Bus Entities 2020

23rd Edition

ISBN:9780357391266

Author:Nellen

Publisher:Nellen

Chapter3: Taxes On The Financial Statements

Section: Chapter Questions

Problem 14P

Related questions

Question

Transcribed Image Text:P19.8 (LO 1, 2, 4) (Two Differences, 2 Years, Compute Taxable

Income and Pretax Financial Income) The following information was

disclosed during the audit of Zheng Group.

Year Amount Due

1.

per Tax Return

2022 ¥130,000,000

2023

104,000,000

2. On January 1, 2022, equipment costing ¥600,000,000 is purchased.

For financial reporting purposes, the company uses straight-line

depreciation over a 5-year life. For tax purposes, the company uses the

double-declining balance method over 5 years.

3. In January 2023, ¥225,000,000 is collected

building for a 3-year period. The entire ¥225,000,000 is reported as

taxable income in 2023, but ¥150,000,000 of the ¥225,000,000 is

reported as unearned revenue in 2023 for financial reporting purposes.

The remaining amount of unearned revenue is to be recognized

equally in 2024 and 2025.

advance rental of a

4. The tax rate is 40% in 2022 and all subsequent periods. (Hint: To find

taxable income in 2022 and 2023, the related income taxes payable

amounts will have to be "grossed up.")

5. No temporary differences existed at the end of 2021. Zheng expects to

report taxable income in each of the next 5 years.

Instructions

a. Determine the amount to report for deferred income taxes at the end

of 2022, and indicate how it should be classified on the statement of

financial position.

b. Prepare the journal entry to record income taxes for 2022.

c. Draft the income tax section of the income statement for 2022,

beginning with "Income before income taxes." (Hint: You must

compute taxable income and then combine that with changes in

cumulative temporary differences to arrive at pretax financial income.)

d. Determine the deferred income taxes at the end of 2023, and indicate

how they should be classified on the statement of financial position.

e. Prepare the journal entry to record income taxes for 2023.

f. Draft the income tax section of the income statement for 2023,

beginning with “Income before income taxes."

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT