Please explain the financial statement with any relevant notes.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter18: Accounting For Income Taxes

Section: Chapter Questions

Problem 12E: Temporary and Permanent Differences Lin has just completed its first year of operations and has a...

Related questions

Question

Please explain the financial statement with any relevant notes.

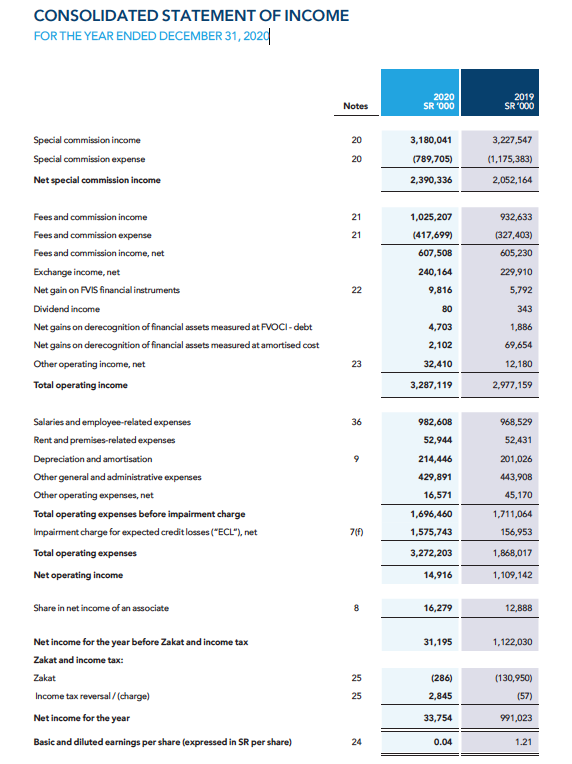

Transcribed Image Text:CONSOLIDATED STATEMENT OF INCOME

FOR THE YEAR ENDED DECEMBER 31, 202|

2020

SR '000

2019

SR '000

Notes

Special commission income

20

3,180,041

3,227,547

Special commission expense

20

(789,705)

(1,175,383)

Net special commission income

2,390,336

2,052,164

Fees and commission income

21

1,025,207

932,633

Fees and commission expense

21

(417,699)

(327,403)

Fees and commission income, net

607,508

605,230

Exchange income, net

240,164

229,910

Net gain on FVIS financial instruments

22

9,816

5,792

Dividend income

80

343

Net gains on derecognition of financial assets measured at FVOCI- debt

4,703

1,886

Net gains on derecognition of financial assets measured at amortised cost

2,102

69,654

Other operating income, net

23

32,410

12,180

Total operating income

3,287,119

2,977,159

Salaries and employee-related expenses

36

982,608

968,529

Rent and premises-related expenses

52,944

52,431

Depreciation and amortisation

214,446

201,026

Other general and administrative expenses

429,891

443,908

Other operating expenses, net

16,571

45,170

Total operating expenses before impairment charge

1,696,460

1,711,064

Impairment charge for expected credit losses ("ECL"), net

1,575,743

156,953

Total operating expenses

3,272,203

1,868,017

Net operating income

14,916

1,109,142

Share in net income of an associate

16,279

12,888

Net income for the year before Zakat and income tax

31,195

1,122,030

Zakat and income tax:

Zakat

25

(286)

(130,950)

Income tax reversal /(charge)

25

2,845

(57)

Net income for the year

33,754

991,023

Basic and diluted earnings per share (expressed in SR per share)

24

0.04

1.21

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning