Powers of the Commissioner on Internal Revenue 1. To interpret tax laws and decide tax cases; 2. To obtain information, and to summon, examine and take testimony of persons; 3. To make assessments and prescribe additional requirements for tax administration and enforcement; 4. To conduct inventory - taking, surveillance and to prescribe presumptive gross sales and receipts; 5. To terminate taxable period; 6. To prescribe real property values; 7. To inquire into bank deposit accounts; 8. To accredit and register tax agents; 9. To prescribe additional procedural or documentary requirements; and 10. To delegate power to subordinates. (Sec. 4 to 8, NIRC)

Powers of the Commissioner on Internal Revenue 1. To interpret tax laws and decide tax cases; 2. To obtain information, and to summon, examine and take testimony of persons; 3. To make assessments and prescribe additional requirements for tax administration and enforcement; 4. To conduct inventory - taking, surveillance and to prescribe presumptive gross sales and receipts; 5. To terminate taxable period; 6. To prescribe real property values; 7. To inquire into bank deposit accounts; 8. To accredit and register tax agents; 9. To prescribe additional procedural or documentary requirements; and 10. To delegate power to subordinates. (Sec. 4 to 8, NIRC)

Chapter17: Corporations: Introduction And Operating Rules

Section: Chapter Questions

Problem 15DQ

Related questions

Question

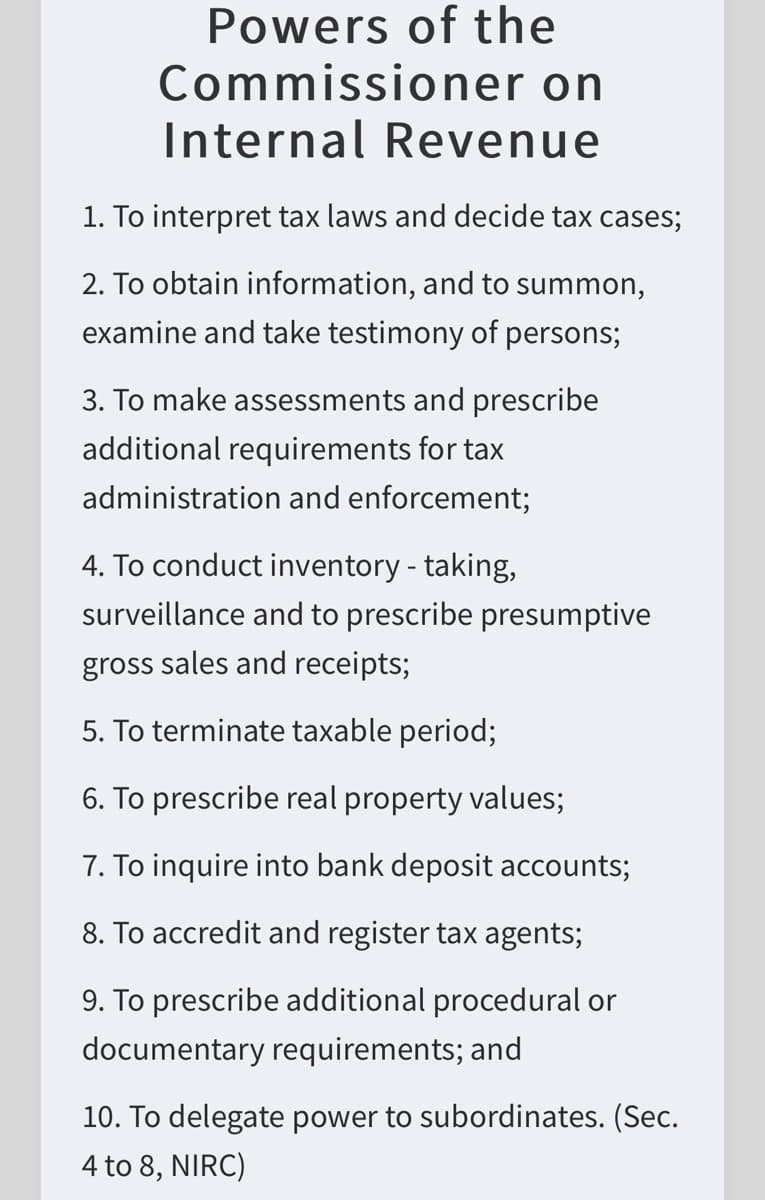

Enumerate and explain ten (10) powers of the Commissioner of Internal Revenue.

Nots: 10 powers of the commissioner is in the photo attached.

Transcribed Image Text:Powers of the

Commissioner on

Internal Revenue

1. To interpret tax laws and decide tax cases;

2. To obtain information, and to summon,

examine and take testimony of persons;

3. To make assessments and prescribe

additional requirements for tax

administration and enforcement;

4. To conduct inventory - taking,

surveillance and to prescribe presumptive

gross sales and receipts;

5. To terminate taxable period;

6. To prescribe real property values;

7. To inquire into bank deposit accounts;

8. To accredit and register tax agents;

9. To prescribe additional procedural or

documentary requirements; and

10. To delegate power to subordinates. (Sec.

4 to 8, NIRC)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning