Prepare journal entry to recognize the transitional effect of adopting revised PAS 19, determine the employee benefit expense for the current year, remeasurement related to the defined benefit plan

Q: Determine the employee benefit expense for the current year, remeasurement related to the defined…

A: A journal entry is a form of accounting entry that is used to report a business transaction in a…

Q: Instructions (a) Determine the pension expense to be reported on the income statement for 2021. (b)…

A:

Q: Which of the following is not a procedure in accounting for defined contribution plans?…

A: A defined-contribution plan refers to the type of retirement plan under which the employees add up a…

Q: The Employee Retirement Income Security Act (ERISA) requires that companies fund defined-benefit…

A: The post-retirement benefits will be benefits, other than annuity disseminations, paid to…

Q: Detail the possible causes of a deficit in a Defined Benefit (DB) pension plan and explain why a…

A: Underfunding occurs when a firm's pension payout obligations outweigh its reserves, requiring the…

Q: A company currently offers it’s employees a defined benefit pension plan, but is looking into…

A: Defined Benefit pension plan A defined-benefit plan is an employer-sponsored retirement plan where…

Q: tark Inc. follows IFRS for financial reporting and has established a defined benefit pension plan…

A: Step 1 A pension benefit obligation is the present value of retirement benefits earned by employees…

Q: Where a post-employment benefit plan contains characteristics of both defined contribution and…

A: The employer needs to pay post employment benefits in addition to salary. The post employee benefits…

Q: Under IAS 19 Employee Benefits, how is actuarial gain or loss handled? amount falling outside…

A: IAS 19 deals with the employee benefits. It includes the pension, benefit plans and gratuity etc.

Q: Question text Under IFRS, which of the following statements is true regarding accounting for defined…

A: “Since you have asked multiple questions, we will solve the first question for you. If you want any…

Q: How should an employer's commitment for employee benefits be calculated, according to AASB 119

A: Definition: In the context of employee benefits, this refers to all types of consideration offered…

Q: What are the disclosures and important key points of interim financial reporting PAS 34 and employee…

A: Firms issue interim statements, which are financial reports that span a duration of less than a…

Q: Explain the following terms as used in IAS 19 Employee Benefits: (1) The term 'defined benefit…

A: Defined Benefit Plan Defined benefit plan which is described as the long term employees compensation…

Q: Explain the following terms. Include the definition, how they are calculated, treated in the…

A: Disclaimer: “Since you have posted a question with multiple sub-parts, we will solve first three…

Q: Which of the following is not considered by an actuary when determining the annual contribution to a…

A: The correct answer with explanations are as follows.

Q: Alternative methods exist for the measurement of the pension obligation (liability). Which measure…

A: Answer: The pension obligation is liability and it is to be paid once the employees retire.

Q: The projected benefit obligation is the measure of pension obligation that __is not sanctioned…

A: The three components of pension expense 1. Service cost, 2. the interest cost, 3. expected return…

Q: In determining the present value of the prospective benefits (often referred to as the defined…

A: In determining the present value of the prospective benefits (often referred to as the defined…

Q: How much is the defined benefit obligation on December 31, 2019? What is the amount of overfunding…

A: Defined Benefit Plan:-This is the benefit enjoyed by the employees how much benefit they will…

Q: Question text Net interest cost is a component of pension expense under IFRS. How is net interest…

A: “Since you have asked multiple questions, we will solve the first question for you. If you want any…

Q: Determine whether each of the following independent statements best applies to a defined…

A: Tax: A tax is a compulsory charge or a levy imposed upon a taxpayer by a government organization…

Q: Write the definition, recognition, measurement, important key points and disclosure if any provided…

A: Accounting standards are the regulations and rules provided to the business for preparing and…

Q: When an entity amends a pension plan, past service cost should be Recorded in other comprehensive…

A: Under a Pension plan, a regular amount is required to be contributed to a pension account and such…

Q: Determine the amounts of the components of pension expense that should be recognized by the company…

A: Pension :— Money that is paid regularly by a government or companies to some body who has stopped…

Q: According to PAS 19, contributions to a defined contribution plan are recognized a. at each…

A: An organization pays the employee past employee benefits. There are some post employee benefits. ·…

Q: Current accounting standards require that the discount rate used for pension plans be: Multiple…

A: As per IAS 19 discount rate used for pension plans be considered as following

Q: In accounting for a pension plan, any difference between the pension cost charged to expense and the…

A: Answer: In accounting for a pension plan, any difference between the pension cost charged to expense…

Q: panies fund defined-benefit plans, but no such requirement exists for other pos

A: The Employee Retirement Income Security Act of 1974 (ERISA) may be a federal law that sets minimum…

Q: Supplemental wage payments include all of the following except: Commissions. Bonuses. Expenses paid…

A: Introduction: Supplemental wages: Supplementary wages are given to employees along with General…

Q: Under PAS 19, which of the following statement is true? I. Current service cost is the increase in…

A: The PAS 19 is related to pension defined benefit obligation plan, when an employee provides the…

Q: FRS119 Employee Benefits prescribes the accounting and disclosure requirements by employers for…

A: IFRS: IFRS stands for International Financial Reporting Standards. These accounting standards are…

Q: 6. Under a defined contribution plan, which of the following statements is false? * The actual…

A: Lease is a contract where one party provides other party rights to use a property on fixed payments…

Q: The amount of compensation subject to OASDI tax is correctly defined as Select one: a. all amounts…

A: OASDI (Old Age, Survivors, and Disability Insurance program) tax is a tax levied by IRS on all…

Q: a. MFRS119 Employee Benefits prescribes the accounting and disclosure requirements by employers for…

A: “Since you have asked multiple questions, we will solve the first question for you. If you want any…

Q: Access the FASB Accounting Standards Codification at the FASB website ( asc.fasb.org ). Determine…

A: 1. Accounting for the disclosures which are required to be reported in the notes to financial…

Q: Indicate by letter whether each of the events listed below increases (I), decreases (D), or has no…

A: Answer: Events 1. N 2. N 3. D 4. I 5. I 6. D 7. I 8. I 9. N 10. I 11. D…

Q: Based upon this information, how would I make the following journal entries? Record annual pension…

A: Record of above journal entry with all necessary workings are as follows.

Q: 1. How to find out the acturial gains and losses on the defined benefit obligation and the defined…

A: The US GAAP and IFRS principles have a similar method of measuring pension benefit obligations but…

Q: In accounting for a defined-benefit pension plan __the expense recognized each period is equal to…

A: Defined benefits plan is plan of pension in this employer provides fixed amount of pension on…

Q: In a defined-benefit plan, the process of funding refers to determining the projected benefit…

A: Pension plan refers to the plans or scheme sponsored by the employers for the retirement benefits of…

Q: CHOOSE THE LETTER OF THE CORRECT ANSWER What is the employee benefit expense for the current year?…

A: Acuturial gan or loss refers to an increase or decrease in the projections used to value a…

Q: Instruetions: (a) Determine the amounts of the components of pension expense that should be…

A: Pension expense is defined as the equivalent sum recorded by the entity for expenses associated with…

Q: Which of the following is not an essential feature of FBT for the FBT year ended 31 March 2020?…

A: A fringe benefit refers to the excess amount paid by the employer over the annual salary or other…

Prepare

Step by step

Solved in 4 steps with 1 images

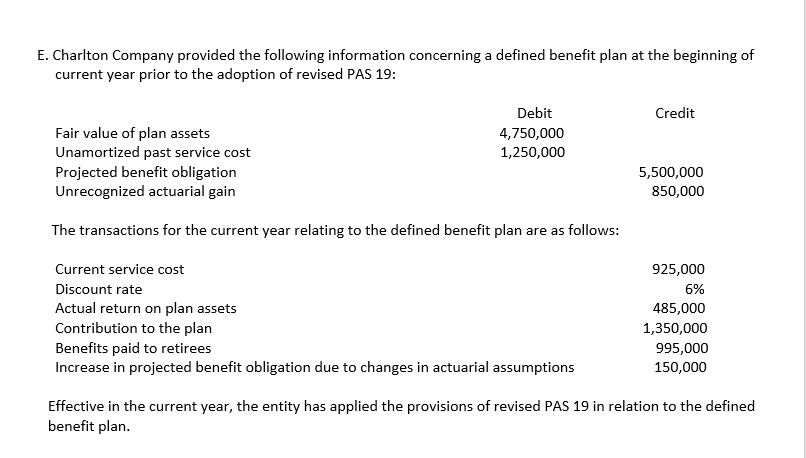

- E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 17. Compute the remeasurement related to the defined benefit plan.E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan. Compute the remeasurement related to the defined benefit plan.

- E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 16. Determine the employee benefit expense for the current year.Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan. 18. Prepare journal entry to record the employee benefit expense.19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.20. Compute for the projected benefit obligation on December 31.Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: Prepare journal entry to recognize the transitional effect of adopting revised PAS 19.

- Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: Prepare journal entry to record the employee benefit expense.Charlton Company provided the following information concerning a defined benefit plan at the beginning of current year prior to the adoption of revised PAS 19: Debit Credit Fair value of plan assets 4,750,000 Unamortized past service cost 1,250,000 Projected benefit obligation Unrecognized actuarial gain 5,500,000 850,000 The transactions for the current year relating to the defined benefit plan are as follows: Current service cost 925,000 Discount rate 6% Actual return on plan assets 485,000 1,350,000 995,000 Contribution to the plan Benefits paid to retirees Increase in projected benefit obligation due to changes in actuarial assumptions 150,000 Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the defined benefit plan. REQUIRED: 15. Prepare journal entry to recognize the transitional effect of adopting revised PAS 19. 17. Compute the remeasurement related to the defined benefit plan. 18. Prepare journal entry to record the…Information about the defined benefit plan of the company is shown belowFair value on plan asset, January 1, 2021 3,000,000Contribution to the fund 1,500,000Return on plan assets 160,000Defined benefit liability. December 31, 2021 410,000Defined benefit obligation, December 31, 2021 4,550,000What is the balance of the fair value on plan asset as of December 31, 2021?

- At the beginning of current year, an entity provided the following information in connection with adefined benefit plan:Fair value of plan assets 10,000,000Projected benefit obligation (13,000,000)Prepaid /accrued benefit cost (3,000,000)The entity revealed the following transactions affecting the plan for the current year:Current service cost 2,500,000Past service cost - remaining vesting period of covered employees is 5 years 1,200,000Contribution to the plan 3,500,000Benefits paid to retirees 3,000,000Actual return on plan assets 1,500,000Decrease in projected benefit obligation due to change in actuarial assumptions 400,000Discount rate 10%Expected return on plan assets 12%REQUIRED:1. Compute the employee benefit expense for the current year2. Compute the net remeasurement gain for the current year3. Compute the fair value of plan assets at year-endAt the beginning of current year, an entity provided the following information in connection with adefined benefit plan:Fair value of plan assets 10,000,000Projected benefit obligation (13,000,000)Prepaid /accrued benefit cost (3,000,000)The entity revealed the following transactions affecting the plan for the current year:Current service cost 2,500,000Past service cost - remaining vesting period of covered employees is 5 years 1,200,000Contribution to the plan 3,500,000Benefits paid to retirees 3,000,000Actual return on plan assets 1,500,000Decrease in projected benefit obligation due to change in actuarial assumptions 400,000Discount rate 10%Expected return on plan assets 12%REQUIRED: 4. Compute the projected benefit obligation at year-end 5. What amount should be reported as accrued or prepaid benefit cost at year-endA. At the beginning of current year, an entity provided the following information in connection with adefined benefit plan: Fair value of plan assets 10,000,000Projected benefit obligation (13,000,000)Prepaid /accrued benefit cost (3,000,000) The entity revealed the following transactions affecting the plan for the current year: Current service cost 2,500,000Past service cost - remaining vesting period of covered employees is 5 years 1,200,000Contribution to the plan 3,500,000Benefits paid to retirees 3,000,000Actual return on plan assets 1,500,000 Decrease in projected benefit obligation due to change in actuarial assumptions 400,000Discount rate 10%Expected return on plan assets 12% Compute the projected benefit obligation at year-end What amount should be reported as accrued or prepaid benefit cost at year-end