Q.2.1 Calculate the correct bank balance at 30 June 2019. Hint – Start by calculating the bank balance at 31 May 2019). Q.2.2 Prepare the bank reconciliation statement at 30 June 2019

Reporting Cash Flows

Reporting of cash flows means a statement of cash flow which is a financial statement. A cash flow statement is prepared by gathering all the data regarding inflows and outflows of a company. The cash flow statement includes cash inflows and outflows from various activities such as operating, financing, and investment. Reporting this statement is important because it is the main financial statement of the company.

Balance Sheet

A balance sheet is an integral part of the set of financial statements of an organization that reports the assets, liabilities, equity (shareholding) capital, other short and long-term debts, along with other related items. A balance sheet is one of the most critical measures of the financial performance and position of the company, and as the name suggests, the statement must balance the assets against the liabilities and equity. The assets are what the company owns, and the liabilities represent what the company owes. Equity represents the amount invested in the business, either by the promoters of the company or by external shareholders. The total assets must match total liabilities plus equity.

Financial Statements

Financial statements are written records of an organization which provide a true and real picture of business activities. It shows the financial position and the operating performance of the company. It is prepared at the end of every financial cycle. It includes three main components that are balance sheet, income statement and cash flow statement.

Owner's Capital

Before we begin to understand what Owner’s capital is and what Equity financing is to an organization, it is important to understand some basic accounting terminologies. A double-entry bookkeeping system Normal account balances are those which are expected to have either a debit balance or a credit balance, depending on the nature of the account. An asset account will have a debit balance as normal balance because an asset is a debit account. Similarly, a liability account will have the normal balance as a credit balance because it is amount owed, representing a credit account. Equity is also said to have a credit balance as its normal balance. However, sometimes the normal balances may be reversed, often due to incorrect journal or posting entries or other accounting/ clerical errors.

The following information was taken from the books of Zia Traders on 30 June 2019:

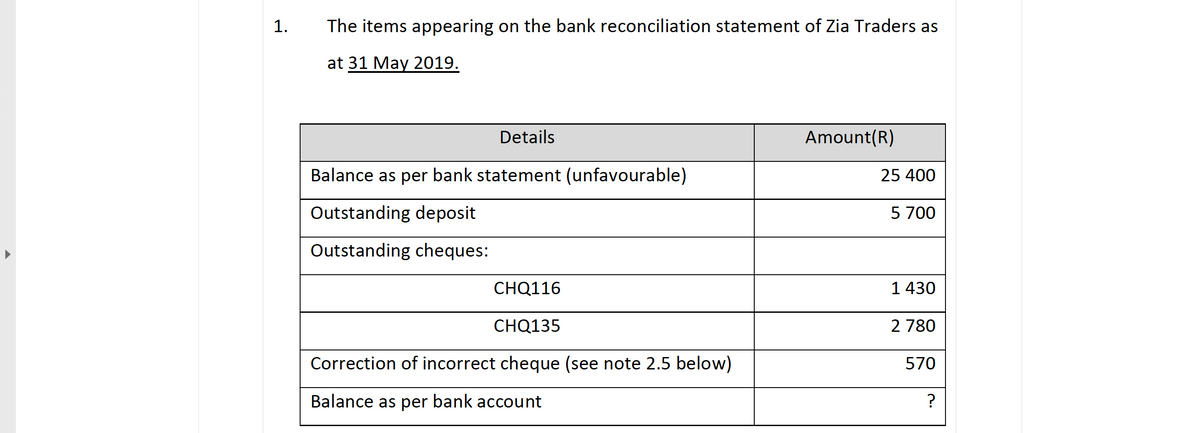

1. The items appearing on the

A comparison of the cashbooks for June, the above bank reconciliation statement and the bank statement for June showed the following:

2.1 Provisional totals in the cashbooks on 30 June:

-

-Cashbook Payments R 96 000

2.2 The outstanding deposit at the end of May for R5 700 appeared on the bank statement on 5 June 2019.

2.3 Cheque number CHQ135 appeared on the bank statement on 7 June for R3 100. An investigation revealed that the bank statement amount was correct.

2.4 Cheque number CHQ116 still did not appear on the bank statement for June 2019. The cheque was originally written out to Gift for the Needy as a donation on 20 November 2018.

2.5 The correction of the incorrect cheque for R570 refers to a cheque that was incorrectly debited twice by the bank. This error has not been rectified by the bank.

2.6 The bookkeeper is in possession of two cheques that she has not entered as she is unsure of what to do:

-CHQ 141 for R5 400 issued to Gilford’s Furnisher’s dated 15

July 2019.

-CHH 101 received from a debtor, M Habana, for R 3 200,

dated 25 July 2019.

2.7 The following cheques appear on the cashbook payments but not on the bank statement:

-CHQ 138 for R 1 200( dated 4 June 2019)

-CHQ 140 for R 680 ( dated 21 June 2019)

2.8 The bank statement showed an electronic transfer into our account from V. Vice, a debtor for R 5 000.

2.9 The bank statement showed the following charges:

-Bank charges – R 450

-Interest on overdraft – R 740

-A dishonoured cheque for R870 originally received from F.Ford in settlement of her debt of R960.

-A debit order to the insurance company for R 3 600

2.10 An investigation revealed the bank has paid the insurance policy twice, i.e. the actual amount is R 1 800. This mistake was also made last month. They have promised to rectify the matter and to refund the amount to the business. The insurance is paid by debit order. Debit orders are captured in the monthly cashbook payments from the bank statement.

2.11 The cashbook receipts showed an amount of R15 600 on 30 June 2019 that did not appear on the bank statement.

2.12 The bank statement received on 30 June showed an unfavourable balance of R19 980.

Required:

Q.2.1 Calculate the correct bank balance at 30 June 2019.

Hint – Start by calculating the bank balance at 31 May 2019).

Q.2.2 Prepare the bank reconciliation statement at 30 June 2019

**please see attached image for format and begining of information**

Step by step

Solved in 2 steps with 3 images