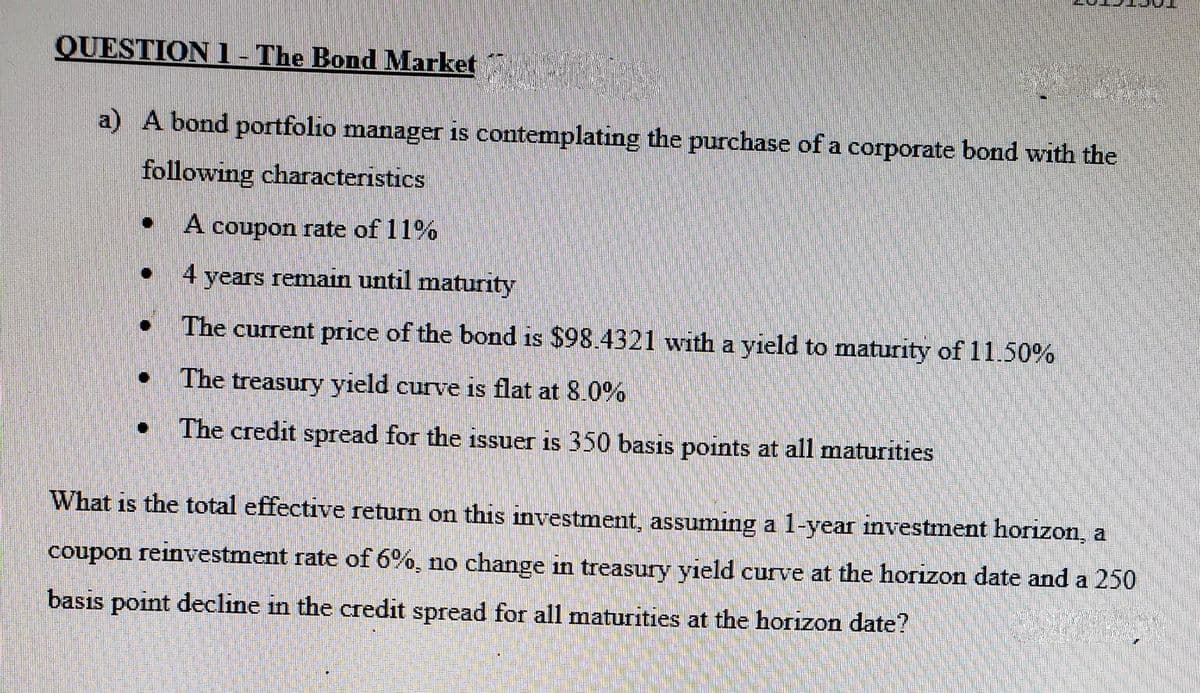

QUESTION 1 - The Bond Market NAR a) A bond portfolio manager is contemplating the purchase of a corporate bond with the following characteristics . A coupon rate of 11% ● 4 years remain until maturity ● The current price of the bond is $98.4321 with a yield to maturity of 11.50% ● The treasury yield curve is flat at 8.0% ● The credit spread for the issuer is 350 basis points at all maturities What is the total effective return on this investment, assuming a 1-year investment horizon, a coupon reinvestment rate of 6%, no change in treasury yield curve at the horizon date and a 250 basis point decline in the credit spread for all maturities at the horizon date?

QUESTION 1 - The Bond Market NAR a) A bond portfolio manager is contemplating the purchase of a corporate bond with the following characteristics . A coupon rate of 11% ● 4 years remain until maturity ● The current price of the bond is $98.4321 with a yield to maturity of 11.50% ● The treasury yield curve is flat at 8.0% ● The credit spread for the issuer is 350 basis points at all maturities What is the total effective return on this investment, assuming a 1-year investment horizon, a coupon reinvestment rate of 6%, no change in treasury yield curve at the horizon date and a 250 basis point decline in the credit spread for all maturities at the horizon date?

Pfin (with Mindtap, 1 Term Printed Access Card) (mindtap Course List)

7th Edition

ISBN:9780357033609

Author:Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Publisher:Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Chapter12: Investing In Stocks And Bonds

Section: Chapter Questions

Problem 8FPE: Describe and differentiate between a bonds (a) current yield and (b) yield to maturity. Why are...

Related questions

Question

Transcribed Image Text:QUESTION 1 - The Bond Market

a) A bond portfolio manager is contemplating the purchase of a corporate bond with the

following characteristics

A coupon rate of 11%

4 years remain until maturity

The current price of the bond is $98.4321 with a yield to maturity of 11.50%

The treasury yield curve is flat at 8.0%

The credit spread for the issuer is 350 basis points at all maturities

What is the total effective return on this investment, assuming a 1-year investment horizon, a

coupon reinvestment rate of 6%, no change in treasury yield curve at the horizon date and a 250

basis point decline in the credit spread for all maturities at the horizon date?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Pfin (with Mindtap, 1 Term Printed Access Card) (…

Finance

ISBN:

9780357033609

Author:

Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Pfin (with Mindtap, 1 Term Printed Access Card) (…

Finance

ISBN:

9780357033609

Author:

Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning