Required: Calculate the capital balances of each partner after the admission of Garachico, assuming that bonuses are recorded when appropriate for each of the following assumptions: 1. Garachicho paid Castro P50,000 for 40% of his interest. 2. Garachico invested P50,000 for a one-sixth interest in the partnership. 3. Garachico invested P50,000 for a 25% interest in the partnership.

Required: Calculate the capital balances of each partner after the admission of Garachico, assuming that bonuses are recorded when appropriate for each of the following assumptions: 1. Garachicho paid Castro P50,000 for 40% of his interest. 2. Garachico invested P50,000 for a one-sixth interest in the partnership. 3. Garachico invested P50,000 for a 25% interest in the partnership.

Chapter15: Partnership Accounting

Section: Chapter Questions

Problem 1PA: The partnership of Tatum and Brook shares profits and losses in a 60:40 ratio respectively after...

Related questions

Question

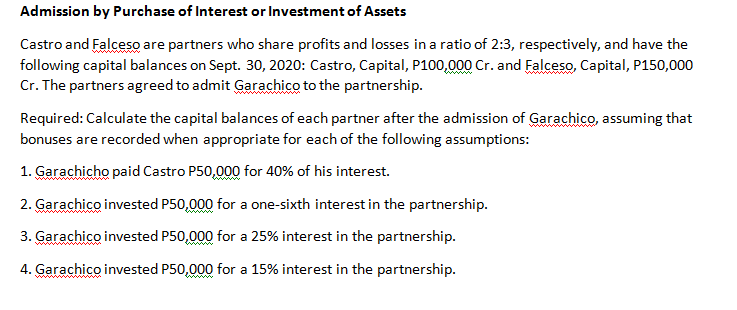

Transcribed Image Text:Admission by Purchase of Interest or Investment of Assets

Castro and Falceso are partners who share profits and losses in a ratio of 2:3, respectively, and have the

following capital balances on Sept. 30, 2020: Castro, Capital, P100,000 Cr. and Falceso, Capital, P150,000

Cr. The partners agreed to admit Garachico to the partnership.

wwww

Required: Calculate the capital balances of each partner after the admission of Garachico, assuming that

bonuses are recorded when appropriate for each of the following assumptions:

1. Garachicho paid Castro P50,000 for 40% of his interest.

2. Garachico invested P50,000 for a one-sixth interest in the partnership.

3. Garachico invested P50,000 for a 25% interest in the partnership.

4. Garachico invested P50,000 for a 15% interest in the partnership.

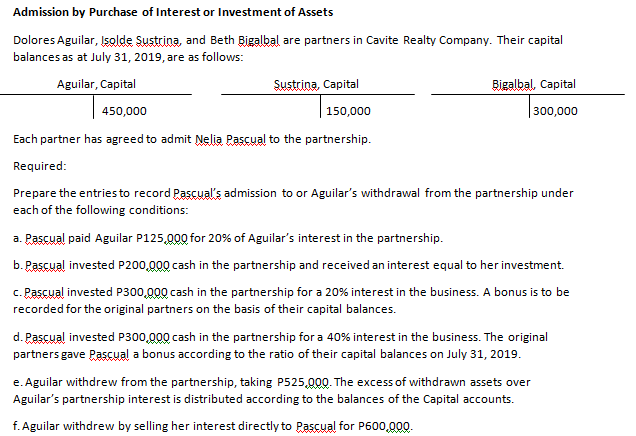

Transcribed Image Text:Admission by Purchase of Interest or Investment of Assets

Dolores Aguilar, Işolde Sustrina, and Beth Bigalbal are partners in Cavite Realty Company. Their capital

balances as at July 31, 2019, are as follows:

Aguilar, Capital

Sustrina, Capital

Bigalbal, Capital

450,000

150,000

300,000

Each partner has agreed to admit Nelia Pascual to the partnership.

Required:

Prepare the entries to record Pascual's admission to or Aguilar's withdrawal from the partnership under

each of the following conditions:

a. Pascual paid Aguilar P125,000 for 20% of Aguilar's interest in the partnership.

b. Pascual invested P200,000 cash in the partnership and received an interest equal to her investment.

c. Pascual invested P300,000 cash in the partnership for a 20% interest in the business. A bonus is to be

recorded for the original partners on the basis of their capital balances.

d. Pascual invested P300,000 cash in the partnership for a 40% interest in the business. The original

partners gave Pascual a bonus according to the ratio of their capital balances on July 31, 2019.

e. Aguilar withdrew from the partnership, taking P525,000. The excess of withdrawn assets over

Aguilar's partnership interest is distributed according to the balances of the Capital accounts.

f. Aguilar withdrew by selling her interest directly to Pascual for P600,000.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning