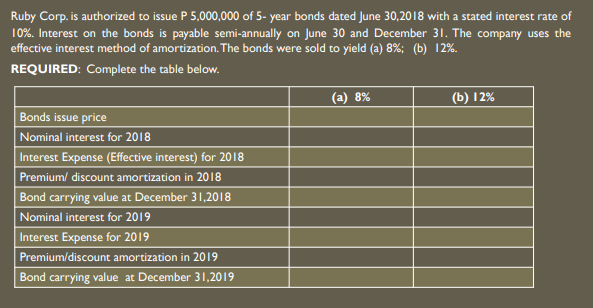

Ruby Corp. is authorized to issue P 5,000,000 of 5- year bonds dated June 30,2018 with a stated interest rate of 10%. Interest on the bonds is payable semi-annually on June 30 and December 31. The company uses the effective interest method of amortization. The bonds were sold to yield (a) 8%; (b) 12%. REQUIRED: Complete the table below. (a) 8% (b) 12% Bonds issue price Nominal interest for 2018 Interest Expense (Effective interest) for 2018 Premium/ discount amortization in 2018

Ruby Corp. is authorized to issue P 5,000,000 of 5- year bonds dated June 30,2018 with a stated interest rate of 10%. Interest on the bonds is payable semi-annually on June 30 and December 31. The company uses the effective interest method of amortization. The bonds were sold to yield (a) 8%; (b) 12%. REQUIRED: Complete the table below. (a) 8% (b) 12% Bonds issue price Nominal interest for 2018 Interest Expense (Effective interest) for 2018 Premium/ discount amortization in 2018

Chapter13: Long-term Liabilities

Section: Chapter Questions

Problem 14MC: Whirlie Inc. issued $300,000 face value, 10% paid annually, 10-year bonds for $319,251 when the...

Related questions

Question

please help me understand this problem. the photos attached has the question and answer already I just need to know where the numbers came from and how it is the answer

Transcribed Image Text:Ruby Corp. is authorized to issue P 5,000,000 of 5- year bonds dated June 30,2018 with a stated interest rate of

10%. Interest on the bonds is payable semi-annually on June 30 and December 31. The company uses the

effective interest method of amortization. The bonds were sold to yield (a) 8%; (b) 12%.

REQUIRED: Complete the table below.

(а) 8%

(b) 1 2%

Bonds issue price

Nominal interest for 2018

Interest Expense (Effective interest) for 2018

Premium/ discount amortization in 2018

Bond carrying value at December 31,2018

Nominal interest for 2019

Interest Expense for 2019

Premium/discount amortization in 2019

Bond carrying value at December 31,2019

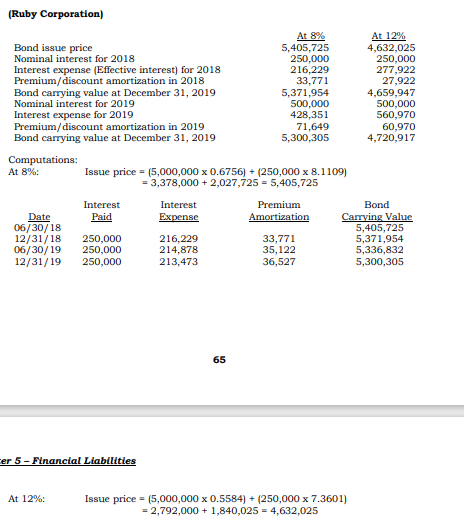

Transcribed Image Text:(Ruby Corporation)

At 8%

5,405,725

250,000

216,229

33,771

5,371,954

500,000

428,351

71,649

5,300,305

At 12%

4,632,025

250,000

277,922

27,922

4,659,947

500,000

560,970

60,970

4,720,917

Bond issue price

Nominal interest for 2018

Interest expense (Effective interest) for 2018

Premium/discount amortization in 2018

Bond carrying value at December 31, 2019

Nominal interest for 2019

Interest expense for 2019

Premium/discount amortization in 2019

Bond carrying value at December 31, 2019

Computations:

At 8%:

Issue price = (5,000,000 x 0.6756) + (250,000 x 8.1109)

= 3,378,000 + 2,027,725 = 5,405,725

Interest

Interest

Premium

Bond

Date

06/30/18

12/31/18

06/30/19

12/31/19

Carrying Value

5,405,725

5,371,954

5,336,832

5,300,305

Paid

Expense

Amortization

250,000

250,000

250,000

216,229

214,878

213,473

33,771

35,122

36,527

65

er 5- Financial Liabilities

At 12%:

Issue price = (5,000,000 x 0.5584) + (250,000 x 7.3601)

= 2,792,000 + 1,840,025 = 4,632,025

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning