s and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $983,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for two years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round

s and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $983,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for two years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round

Chapter12: Current Liabilities

Section: Chapter Questions

Problem 16Q: Jain Enterprises honors a short-term note payable. Principal on the note is $425,000, with an annual...

Related questions

Question

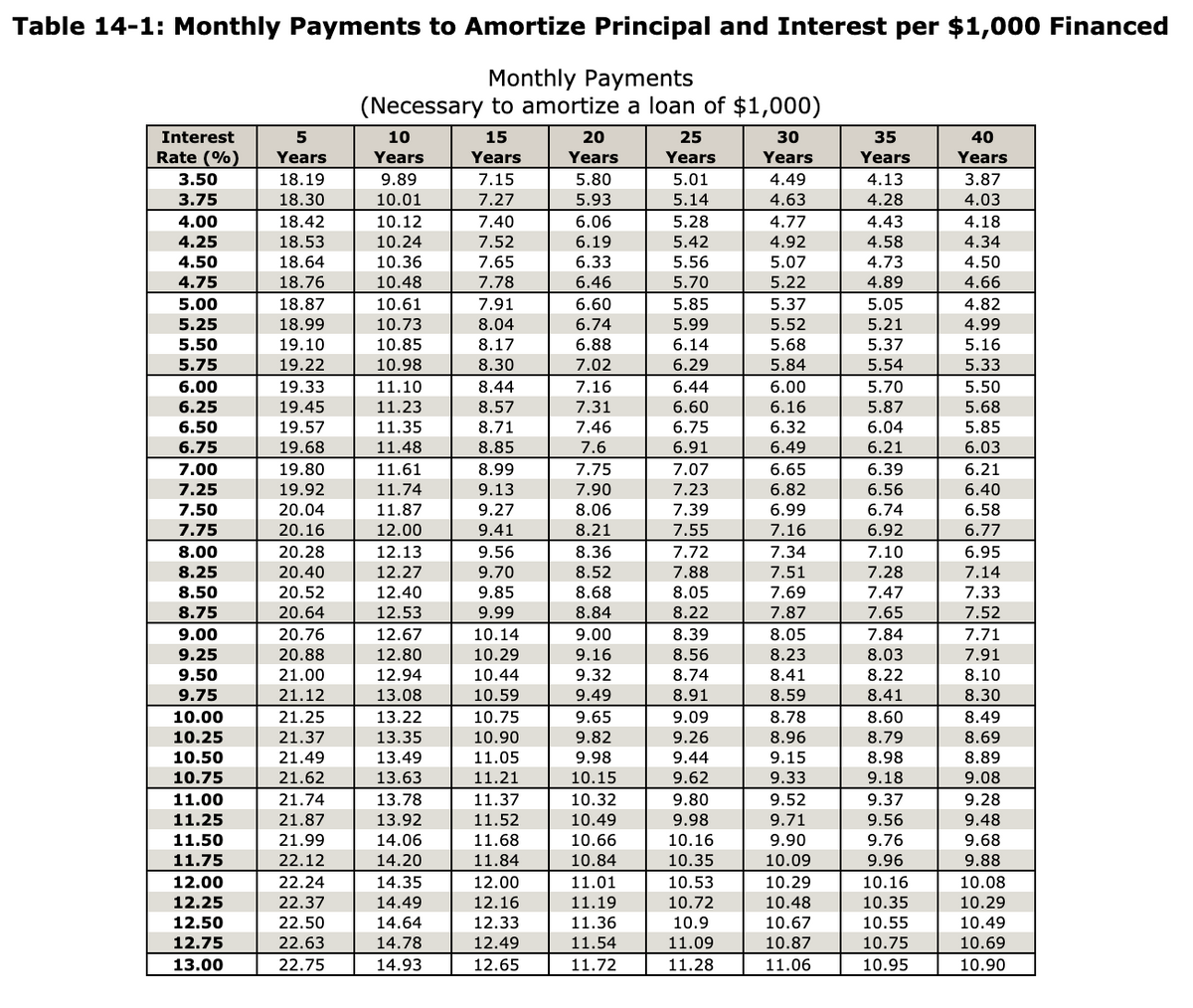

The buyer of a piece of real estate is often given the option of buying down the loan. This option gives the buyer a choice of loan terms in which various combinations of interest rates and discount points are offered. The choice of how many points and what rate is optimal is often a matter of how long the buyer intends to keep the property.

Darrell Frye is planning to buy an office building at a cost of $983,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for two years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round your answers to the nearest cent. Use this table, if necessary.)

(a)

What is the amount being financed?

$

(b)

If Darrell chooses the 4-point 9% loan, what will be his total outlay in points and payments after 24 months?

$

Transcribed Image Text:Table 14-1: Monthly Payments to Amortize Principal and Interest per $1,000 Financed

Monthly Payments

(Necessary to amortize a loan of $1,000)

Interest

5

10

15

20

25

30

35

40

Rate (%)

Years

Years

Years

Years

Years

Years

Years

Years

3.50

18.19

9.89

7.15

5.80

5.01

4.49

4.13

3.87

3.75

18.30

10.01

7.27

5.93

5.14

4.63

4.28

4.03

6.06

6.19

4.77

4.00

4.25

5.28

5.42

18.42

10.12

7.40

7.52

4.43

4.58

4.18

18.53

10.24

4.92

4.34

4.50

18.64

10.36

7.65

6.33

5.56

5.07

4.73

4.50

4.75

18.76

10.48

7.78

6.46

5.70

5.22

4.89

4.66

5.00

18.87

10.61

7.91

6.60

5.85

5.37

5.05

4.82

8.04

8.17

5.25

18.99

10.73

6.74

5.99

5.52

5.21

4.99

5.50

19.10

10.85

6.88

6.14

5.68

5.37

5.16

5.75

19.22

10.98

8.30

7.02

6.29

5.84

5.54

5.33

6.00

19.33

11.10

8.44

7.16

6.44

6.00

5.70

5.50

6.25

19.45

11.23

8.57

7.31

6.60

6.16

5.87

5.68

6.50

19.57

11.35

8.71

7.46

6.75

6.32

6.04

5.85

6.75

19.68

11.48

8.85

7.6

6.91

6.49

6.21

6.03

7.00

19.80

11.61

8.99

7.75

7.07

6.65

6.39

6.21

11.74

11.87

7.25

19.92

9.13

7.90

7.23

7.39

6.82

6.56

6.40

7.50

20.04

9.27

8.06

6.99

6.74

6.58

7.75

20.16

12.00

9.41

8.21

7.55

7.16

6.92

6.77

8.00

20.28

12.13

9.56

8.36

7.72

7.34

7.10

6.95

8.25

20.40

12.27

9.70

8.52

7.88

7.51

7.28

7.14

8.50

20.52

20.64

12.40

9.85

9.99

8.68

8.05

7.69

7.87

7.47

7.33

8.75

12.53

8.84

8.22

7.65

7.52

9.00

20.76

12.67

10.14

9.00

8.39

8.05

7.84

7.71

12.80

12.94

13.08

9.25

20.88

10.29

9.16

8.56

8.23

8.03

7.91

9.50

21.00

10.44

9.32

8.74

8.41

8.22

8.10

9.75

21.12

10.59

9.49

8.91

8.59

8.41

8.30

9.65

9.82

10.00

21.25

13.22

10.75

9.09

8.78

8.60

8.49

10.25

21.37

13.35

10.90

9.26

8.96

8.79

8.69

10.50

21.49

13.49

11.05

9.98

9.44

9.15

8.98

8.89

10.75

21.62

13.63

11.21

10.15

9.62

9.33

9.18

9.08

11.00

21.74

13.78

11.37

10.32

9.80

9.52

9.37

9.28

11.25

21.87

13.92

11.52

10.49

9.98

9.71

9.56

9.48

14.06

14.20

11.50

21.99

11.68

10.66

10.16

9.90

9.76

9.68

11.75

22.12

11.84

10.84

10.35

10.09

9.96

9.88

12.00

14.35

14.49

10.08

10.29

22.24

12.00

11.01

10.53

10.29

10.16

12.25

22.37

12.16

11.19

10.72

10.48

10.35

12.50

22.50

14.64

12.33

11.36

10.9

10.67

10.55

10.49

12.75

22.63

14.78

12.49

11.54

11.09

10.87

10.75

10.69

13.00

22.75

14.93

12.65

11.72

11.28

11.06

10.95

10.90

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781337395250

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning