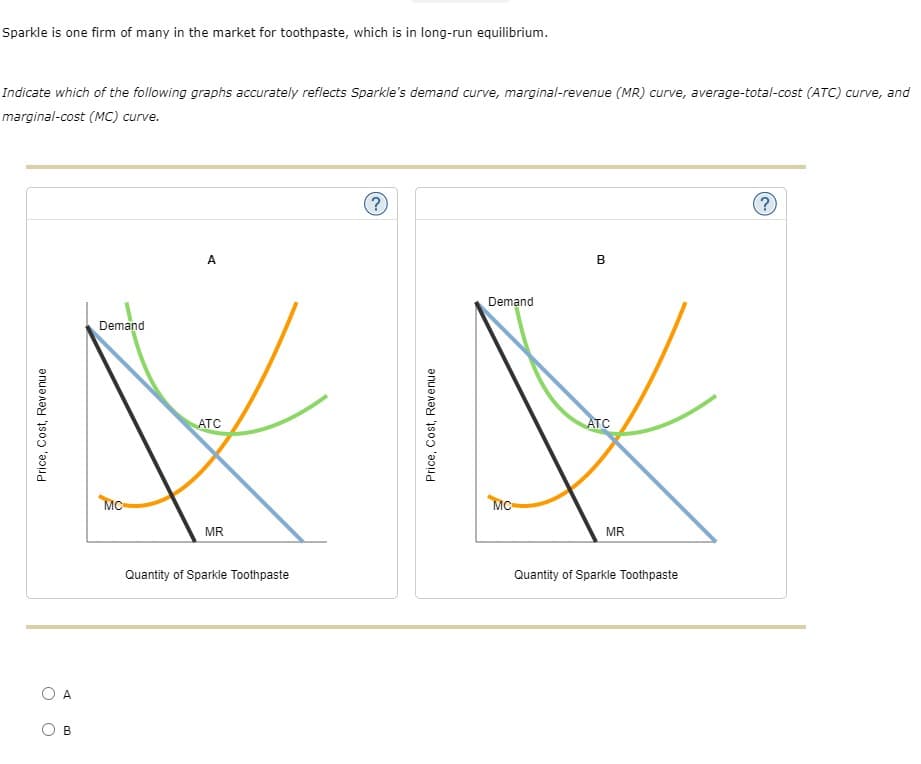

Sparkle is one firm of many in the market for toothpaste, which is in long-run equilibrium. Indicate which of the following graphs accurately reflects Sparkle's demand curve, marginal-revenue (MR) curve, average-total-cost (ATC) curve, and marginal-cost (MC) curve. A Demand Demand ATC ATC MC MC- MR MR Quantity of Sparkle Toothpaste Quantity of Sparkle Toothpaste O A B Price, Cost, Revenue Price, Cost, Revenue

Q: Demand for Fries QD(P) = 10,000 - 10P N number of firms follow: TC(Q) = 20,000 +0.5Q^2 What…

A: In a perfectly competitive market there are large number of firms produce similar and identical…

Q: The market for peanut butter in Nutville ismonopolistically competitive and in long-runequilibrium.…

A: Hi thanks for the question. Since there are multiple subparts in the question, we will answer for…

Q: The graph shows the demand curve (D), average total cost curve (ATC), average variable cost curve…

A: In perfectly competitive market, the firm produces where D=MC. Here, that is denoted by point A in…

Q: Suppose the book-printing industry is competitive and begins in a long-run equilibrium. Then Hi-Tech…

A: The perfectly competitive is the type of firm where there are large number of buyers and sellers.…

Q: Show what happens in the short run on both graphs when a new medical study shows soybeans to be…

A: Demand and the supply curve can shift in the market due to changes in several factors. The changes…

Q: Consider a perfectly competitive constant-cost industry with n identical firms. Startis from long…

A: A perfectly competitive industry with a horizontal long-run industry supply curve as a result of no…

Q: A national campaign to fight obesity runs advertisements during Thanksgiving reducing market demand…

A: Profit maximizing quantity is where marginal revenue equals marginal cost. Long run equilibrium for…

Q: Question 3: The situation facing by firm “Smart”, a producer of running shoes, is shown in the…

A: Hello, thank you for the question. Since there are multiple sub-part questions asked here, only the…

Q: Fill the table below given Perfect Competition Conditions Quantity Demanded/ Produced Total…

A: The cost incurred in the production of final goods and services is known as the total cost. The cost…

Q: Perfect competition is a theoretical market structure in which the following criteria are met: All…

A: Hi! Thank you for the question, As per the honor code, we are allowed to answer three sub-parts at a…

Q: Ellen's total cost is; C = 100+ Q² The market price of eggs is: P = 20 d. Find the equations of…

A: Total Cost : C=100+Q2 Price=20 a. Marginal Cost is the change in the total cost due to the change…

Q: The table below shows the average cost (AC) for a purely competitive market. The average revenue…

A: Given: Average revenue (AR) =RM5 per unit Firm’s total fixed cost (TFC) =RM4.

Q: In the market for running shoes, all the firms face a similar demand curve and have similar cost…

A: Answer - "Thank you for submitting the question but we are authorized to solve 3 sub- parts of the…

Q: Use the table below to answer questions about Christina's Christmas Wreaths. Christina operates in a…

A: We have given price = 64 for product the product. Due to given price, MR becomes equals to the…

Q: b). The Philadelphia water ice industry is a constant cost industry. The demand for water ice…

A: A constant cost industry is an industry whose output can be increased without an increase in the…

Q: In the short-run equilibrium of a competitive marketwith identical firms, if new firms are getting…

A: Perfect competition is a market structure in which characterized by a large number of buyers and…

Q: Peter's Pencils is a perfectly competitive company producing pencils. Suppose Peter is producing…

A: For Perfect competition, we know that P = MC and P = MR (since the price remains the same…

Q: Answer the question on the basis of the following demand and cost data for a specific firm. Demand…

A: Profit maximizing level of output for a firm is at the point where marginal revenue (MR) equals…

Q: Price and cost MC ATC AVC 20 MR 15 14 11 750 1,100 1,350 1,800 Quantity Figure 12-5 shows cost and…

A: The perfect competitive industry is that industry which has large number of buyers and sellers. They…

Q: Paragraph Styles 8. When firms are said to be price takers, it implies that if a firm raises its…

A: Since you have asked multiple question, we will solve the first question for you. If youwant any…

Q: Consider a perfectly competitive market and a firm's average total cost curve and marginal cost…

A: In a perfectly competitive market there are large number of firms producing similar and identical…

Q: The two figures below show (on the left) the industry supply and demand for wheat and (on the right)…

A: Here, the first graph shows the market for wheat and the second graph shows cost functions of a…

Q: Alpha is a price taking firm. At Its currant output level of 100 widgets. Alpha's total revenue is…

A: A price taking firm is one that operates its business in the competitive markets, such that a…

Q: Sparkle is one firm of many in the market for toothpaste, which is in long-run equilibrium. Indicate…

A: Sparkle is one of the many firms in market of toothpaste which means it is talking about…

Q: Suppose the book-printing industry is competitive and begins in a long-run equilibrium. Then Hi-Tech…

A: Long-run equilibrium happens when aggregate demand rises to short-run aggregate supply at a point on…

Q: ssume that apples are produced in a perfectly competitive market. Grande’s Orchard is a typical firm…

A: (a) Market is competitive so a typical firm's demand curve is fixed at market price which means…

Q: Some firms in the market are making profit, others are having losses. Draw and explain graphs…

A:

Q: Suppose Dmitri runs a small business that manufactures frying pans. Assume that the market for…

A: Profit maximization refers to the production and distribution of goods in such a way that maximizes…

Q: Consider a perfectly competitive increasing-cost industry with n identical firms. Starting from long…

A: a) n the short run, perfectly competitive firm is all about seeking the quantity in the output and…

Q: Suppose the book-printing industry is competitive and begins in a long-run equilibrium. Then Hi-Tech…

A: A competitive market is characterized by a large number of buyers and sellers. The market price and…

Q: Read Eye on Smartphones. Explain why smartphone producers offer such a large variety of their…

A: If a product is significantly distinct from those of other companies, it is said to be product…

Q: What is the profit maximizing level of output for the firm? How much profit is this firm earning?…

A: Profit maximizing level of output is achieved where price and quantity are equal i.e., in…

Q: Fruit market (a perfectly competitive market), the industry demand and supply of tomato (a…

A:

Q: Graph the AT C, AV C, MC, and MR curves in a single graph, and indicate the profit maximizing level…

A:

Q: hey i need help with my homework

A: When there is an increase in demand in a competitive firm, the new equilibrium point shifts to B and…

Q: Assume that apples are produced in a perfectly competitive market. Grande’s Orchard is a typical…

A: a) The graph below shows Grande's demand curve along with the cost curves. QG is the profit…

Q: Perfect Competition and the Supply Curve — End of Chapter Problem 3. Bob produces Blu-ray movies for…

A: Hello, Thanks for the question. Since there are multiple sub-parts posted here, only the first three…

Q: ncludes the firm’s dem

A: Perfect competition is a theoretical structure of market in which all firms tend to sell an…

Q: The Nintari Company produces video-game-playing machines and a second firm, Necsega, owns exclusive…

A: Imperfectly Competitive Market An imperfect competition market is a situation where there is a…

Q: Kali is a dot-com entrepreneur who has established a Web site at which people can design and buy a…

A: Given Kali has to pay $100 for an internet connection and 10 per pair of sunglasses So the total…

Q: rcinogenic. On the market graph, you will shift a curve or curves. On the firm's graph, use Price 2…

A: * Answer :-

Q: Question 16 For a purely competitive firm: C marginal revenue will graph as an upsloping line. C the…

A: Answer - Given in the question - For purely competitive firm Evaluating the options - 1. Marginal…

Q: Basti’s Coffee operates in a competitive market. The short run price in the coffee market is equal…

A: Perfect competition is a market structure where a very large number of buyers and sellers exist, and…

Q: Question 2: Assume that apples are produced in a perfectly competitive market. Columbia's Orchard is…

A: a. In a competitive market the demand curve is the fixed at market price. That is, the price line is…

Q: Demand Demand ATC MR MR Quantity of Sparkle Toothpaste Quantity of Sparkie Toothpaste Price, Cost,…

A: The market specified here is that of monopolistic competition. In the long run, a firm in a…

Q: The graph shows an individual firm in a perfectly (purely) competitive industry. Adjust the…

A: The long run equilibrium occur at where the Price = MC= Average total cost (ATC).Below Figure shows…

Q: 3. Entry and exit in the long run Suppose that bike manufacturers in a competitive price-searcher…

A: A downward-sloping demand curve faces firms in a competitive price-searcher market with minimal…

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images

- Sparkle is one firm of many in the market for toothpaste, which is in long-run equilibrium. Indicate which of the following graphs accurately reflects Sparkle's demand curve, marginal-revenue (MR) curve, average-total-cost (ATC) curve, and marginal-cost (MC) curve.Bavarian Crystal Works designs and produces crystal wine decanters for export to international markets. The marketing manager of Bavarian Crystal Works estimates the demand curve for each month to be: P=1,000-0.0025Q Where Q is the number of wine decanters produced monthly. Bavarian Crystal Works also pays a lease for its factory and equipment every month in the amount of $1,000,000. Finally, the cost to produce each wine decanter is $200. What quantity would maximize profits? What is the optimal price for Bavarian Crystals to charge?Fruit market (a perfectly competitive market), the industry demand and supply of tomato (a homogenous product) is given by the following equations respectively: Qd = 50 − P Qs = 1 + 3P The typical firm’s total cost is given by the following equation: TC = 10 + 0.5Q2 + 5Q What is the profit maximizing level of output for the firm? How much profit is this firm earning? Show it graphically Is it short run or long run? Explain!

- A perfectly competitive firm produces good X and has the following weekly cost data. ( Q = total output; TFC = total fixed cost; TVC = total variable cost): Q (units) TFC ($) TVC $ TC ($) ATC $ AVC $ MC $ 0 0 120 1 172 2 219 3 261 4 300 5 342 6 389 7 441 8 499 9 565 10 641 (a) Complete the above table. Round off values to the nearest two decimal places. (b) For each of the following prices determine this firm’s profit- maximising (or loss-minimising) output per week in the short run, and calculate the weekly profit or loss. Show your calculations (to two decimal places). (b.i) $42.50 (b.ii) $47.50…Firm Alpha operates in a perfectly competitive market in a constant-cost industry and is earning negative economic profit. How does Firm Alpha determine its profit-maximizing quantity of output? Explain. Draw correctly labeled side-by-side graphs for Firm Alpha and the market it operates in. Label the axes and all of the following: Market price (PE) and market quantity (QE) The firm's quantity of output (Qe) The firm's average total cost (ATC) Completely shade the area of the firm's total cost. Identify whether the following increase, decrease, or remain constant as the market moves to long-run equilibrium: Market equilibrium quantity Market equilibrium price Assume the product that Firm Alpha produces has a negative externality. Draw the marginal social cost (MSC) on the market graph from part (b). Will the unregulated market produce more or less than the socially optimal quantity? Label the socially optimal quantity (Qso) for the market on your graph from part (b).…Firm Alpha operates in a perfectly competitive market in a constant-cost industry and is earning negative economic profit. How does Firm Alpha determine its profit-maximizing quantity of output? Explain. Draw correctly labeled side-by-side graphs for Firm Alpha and the market it operates in. Label the axes and all of the following: Market price (PE) and market quantity (QE) The firm's quantity of output (Qe) The firm's average total cost (ATC) Completely shade the area of the firm's total cost. Identify whether the following increase, decrease, or remain constant as the market moves to long-run equilibrium: Market equilibrium quantity Market equilibrium price Assume the product that Firm Alpha produces has a negative externality. Draw the marginal social cost (MSC) on the market graph from part (b). Will the unregulated market produce more or less than the socially optimal quantity? Label the socially optimal quantity (Qso) for the market on your graph from part (b).

- Answer the questions based on the table below - Complete the table below. - In which market does this firm operate? Explain your reasons. - Determine the equilibrium output. Calculate whether the firm will it be earning a profit or suffering a loss at equilibrium. Quantity(unit) Total Revenue($) Average Revenue($) MarginalRevenue($) TotalCost($) MarginalCost($) 1 10 5 2 18 11 3 24 16 4 28 20 5 30 23 6 30 25(Figure: Price and Quantity of Output and Table I) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. At a market price of $40, the industry output is ____. A. 4 B. 1 C. 15 D. 9.5 Note:- Please avoid using ChatGPT and refrain from providing handwritten solutions; otherwise, I will definitely give a downvote. Also, be mindful of plagiarism. Answer completely and accurate answer. Rest assured, you will receive an upvote if the answer is accurate.Consider a form that is participating in this market (refer to P, Q (firm quantity), ATC, and AVC in the table below). Graphically illustrate this firm, graph the ATX, AVC, MC, and demand curves and calculate the total revenue, total cost, total fixed cost, total variable cost, and profit for this firm. identify the profit case. Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.

- A typical profit-maximizing firm in a perfectly competitive constant-cost industry is earning a positive economic profit.(a) Is the market price greater than, less than, or equal to the firm's price? Explain.(b) Draw correctly labeled side-by-side graphs for both the market and a typical firm and show each of the Following(i) Market price and quantity, labeled Pm and Qm.(ii) The firm's quantity, labeled Qf(iii) The firm's average revenue curve, labeled AR(iv) The firm's average total cost curve, labeled ATC(v) The area representing total cost, shaded completely(c) If one firm in the market were to raise its price, what will happen to its total revenue? Explain.(d) Now suppose the market is in long-run equilibrium. The government gives a lump-sum subsidy to each firmproducing in the industry. Indicate whether each of the following will increase, decrease, or remain the same.(i)The firm's quantity in the short run. Explain.(ii) The market price and quantity in the long run. Explain.Q2 (a). Assume apples are sold in a perfectly competitive market and firms are making zero economic profit. Explain and illustrate graphically, the effect of increase in market price on the short run position of a single firm selling apples. (Hint: Make sure your graph includes the firm’s demand curve, marginal revenue curve, marginal cost curve and average total cost curve and also explain the profit maximising position of a firm) Q2 (b). Based on the short run position identified in Q2 (a) explain and illustrate graphically effect of entry/exit on the long run position of the firm. (Hint: your answer should include graphs for both market as well as individual firm.) To clarify, there are no values provided (no price change value etc.), the answers simply need to represent the concept of what would happen.Assume perfect competition:Price: $61Cost: TC = 9Q + 0.03Q2Solve for the profit-maximizing Quantity produced by an individual firm in the short run. ROUND TO THE NEAREST WHOLE NUMBER