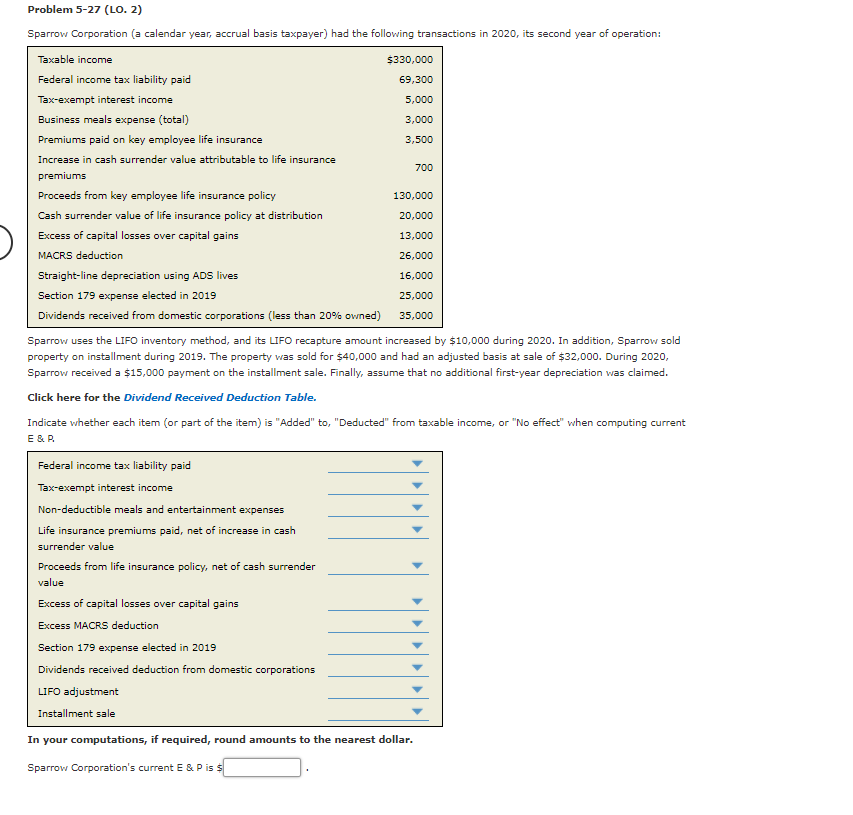

Sparrow Corporation (a calendar year, accrual basis taxpayer) had the following transactions in 2020, its second year of operation: Taxable income $330,000 Federal income tax liability paid 69,300 Tax-exempt interest income 5,000 Business meals expense (total) 3,000 Premiums paid on key employee life insurance 3,500 Increase in cash surrender value attributable to life insurance 700 premiums Proceeds from key employee life insurance policy 130,000 Cash surrender value of life insurance policy at distribution 20,000 Excess of capital losses over capital gains 13,000 MACRS deduction 26,000 Straight-line depreciation using ADS lives 16,000 Section 179 expense elected in 2019 25,000 Dividends received from domestic corporations (less than 20% ovned) 35,000 Sparrow uses the LIFO inventory method, and its LIFO recapture amount increased by $10,000 during 2020. In addition, Sparrovw sold property on installment during 2019. The property vas sold for $40,000 and had an adjusted basis at sale of $32,000. During 2020, Sparrow received a $15,000 payment on the installment sale. Finally, assume that no additional first-year depreciation was claimed. Click here for the Dividend Received Deduction Table. Indicate whether each item (or part of the item) is "Added" to, "Deducted" from taxable income, or "No effect" when computing current E&R Federal income tax liability paid Tax-exempt interest income Non-deductible meals and entertainment expenses Life insurance premiums paid, net of increase in cash surrender value Proceeds from life insurance policy, net of cash surrender value Excess of capital losses over capital gains Excess MACRS deduction Section 179 expense elected in 2019 Dividends received deduction from domestic corporations LIFO adjustment Installment sale In your computations, if required, round amounts to the nearest dollar. Sparrow Corporation's current E& P is s

Sparrow Corporation (a calendar year, accrual basis taxpayer) had the following transactions in 2020, its second year of operation: Taxable income $330,000 Federal income tax liability paid 69,300 Tax-exempt interest income 5,000 Business meals expense (total) 3,000 Premiums paid on key employee life insurance 3,500 Increase in cash surrender value attributable to life insurance 700 premiums Proceeds from key employee life insurance policy 130,000 Cash surrender value of life insurance policy at distribution 20,000 Excess of capital losses over capital gains 13,000 MACRS deduction 26,000 Straight-line depreciation using ADS lives 16,000 Section 179 expense elected in 2019 25,000 Dividends received from domestic corporations (less than 20% ovned) 35,000 Sparrow uses the LIFO inventory method, and its LIFO recapture amount increased by $10,000 during 2020. In addition, Sparrovw sold property on installment during 2019. The property vas sold for $40,000 and had an adjusted basis at sale of $32,000. During 2020, Sparrow received a $15,000 payment on the installment sale. Finally, assume that no additional first-year depreciation was claimed. Click here for the Dividend Received Deduction Table. Indicate whether each item (or part of the item) is "Added" to, "Deducted" from taxable income, or "No effect" when computing current E&R Federal income tax liability paid Tax-exempt interest income Non-deductible meals and entertainment expenses Life insurance premiums paid, net of increase in cash surrender value Proceeds from life insurance policy, net of cash surrender value Excess of capital losses over capital gains Excess MACRS deduction Section 179 expense elected in 2019 Dividends received deduction from domestic corporations LIFO adjustment Installment sale In your computations, if required, round amounts to the nearest dollar. Sparrow Corporation's current E& P is s

Chapter5: Corporations: Earnings & Profits And Dividend Distributions

Section: Chapter Questions

Problem 27P

Related questions

Question

See Attached 5.27 with Dividened Reduction Table

Transcribed Image Text:Problem 5-27 (LO. 2)

Sparrow Corporation (a calendar year, accrual basis taxpayer) had the following transactions in 2020, its second year of operation:

Taxable income

$330,000

Federal income tax liability paid

69,300

Tax-exempt interest income

5,000

Business meals expense (total)

3,000

Premiums paid on key employee life insurance

3,500

Increase in cash surrender value attributable to life insurance

700

premiums

Proceeds from key employee life insurance policy

130,000

Cash surrender value of life insurance policy at distribution

20,000

Excess of capital losses over capital gains

13,000

MACRS deduction

26,000

Straight-line depreciation using ADs lives

16,000

Section 179 expense elected in 2019

25,000

Dividends received from domestic corporations (less than 20% owned)

35,000

Sparrow uses the LIFO inventory method, and its LIFO recapture amount increased by $10,000 during 2020. In addition, Sparrow sold

property on installment during 2019. The property vas sold for $40,000 and had an adjusted basis at sale of $32,000. During 2020,

Sparrow received a $15,000 payment on the installment sale. Finally, assume that no additional first-year depreciation was claimed.

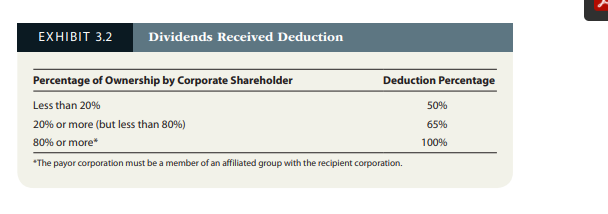

Click here for the Dividend Received Deduction Table.

Indicate whether each item (or part of the item) is "Added" to, "Deducted" from taxable income, or "No effect" when computing current

E & P.

Federal income tax liability paid

Tax-exempt interest income

Non-deductible meals and entertainment expenses

Life insurance premiums paid, net of increase in cash

surrender value

Proceeds from life insurance policy, net of cash surrender

value

Excess of capital losses over capital gains

Excess MACRS deduction

Section 179 expense elected in 2019

Dividends received deduction from domestic corporations

LIFO adjustment

Installment sale

In your computations, if required, round amounts to the nearest dollar.

Sparrow Corporation's current E & P is $

Transcribed Image Text:EXHIBIT 3.2

Dividends Received Deduction

Percentage of Ownership by Corporate Shareholder

Deduction Percentage

Less than 20%

50%

20% or more (but less than 80%)

65%

80% or more*

100%

*The payor corporation must be a member of an affiliated group with the recipient corporation.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT