Supply and demand are both key concepts to understanding the economy because they reflect the prices and quantities of consumer goods and services. According to market economy theory, the relationship between supply and demand balances out at a point in the future; this point is called the equilibrium price. A consumer surplus occurs when the price that consumers pay for a product or service is less than the price they're willing to pay. A producer surplus is the total amount that a producer benefits from producing and selling a quantity of a good at the market price. Both can be represented by areas between the supply and demand curves as shown in the sample figure. 15 and the supply curve y = 15x Find the consumer surplus and producer surplus for the demand curve y = x2 +1 x2 +1 (a) Sketch the graphs and shade the appropriate regions. Find the equilibrium point, (ro, Po). Consumer Supply surplus curve Point of equilibrium Po Demand Producer surplus curve (b) Find the consumer surplus. Show all work to support your answer. Consumer Surplus = (round to nearest tenth) (c) Find the producer surplus. Show all work to support your answer. Producer Surplus = (round to nearest tenth)

Supply and demand are both key concepts to understanding the economy because they reflect the prices and quantities of consumer goods and services. According to market economy theory, the relationship between supply and demand balances out at a point in the future; this point is called the equilibrium price. A consumer surplus occurs when the price that consumers pay for a product or service is less than the price they're willing to pay. A producer surplus is the total amount that a producer benefits from producing and selling a quantity of a good at the market price. Both can be represented by areas between the supply and demand curves as shown in the sample figure. 15 and the supply curve y = 15x Find the consumer surplus and producer surplus for the demand curve y = x2 +1 x2 +1 (a) Sketch the graphs and shade the appropriate regions. Find the equilibrium point, (ro, Po). Consumer Supply surplus curve Point of equilibrium Po Demand Producer surplus curve (b) Find the consumer surplus. Show all work to support your answer. Consumer Surplus = (round to nearest tenth) (c) Find the producer surplus. Show all work to support your answer. Producer Surplus = (round to nearest tenth)

Chapter6: Systems Of Equations And Inequalities

Section: Chapter Questions

Problem 21T: A manufacturer produces two models of television stands. The table at the left shows the times (in...

Related questions

Question

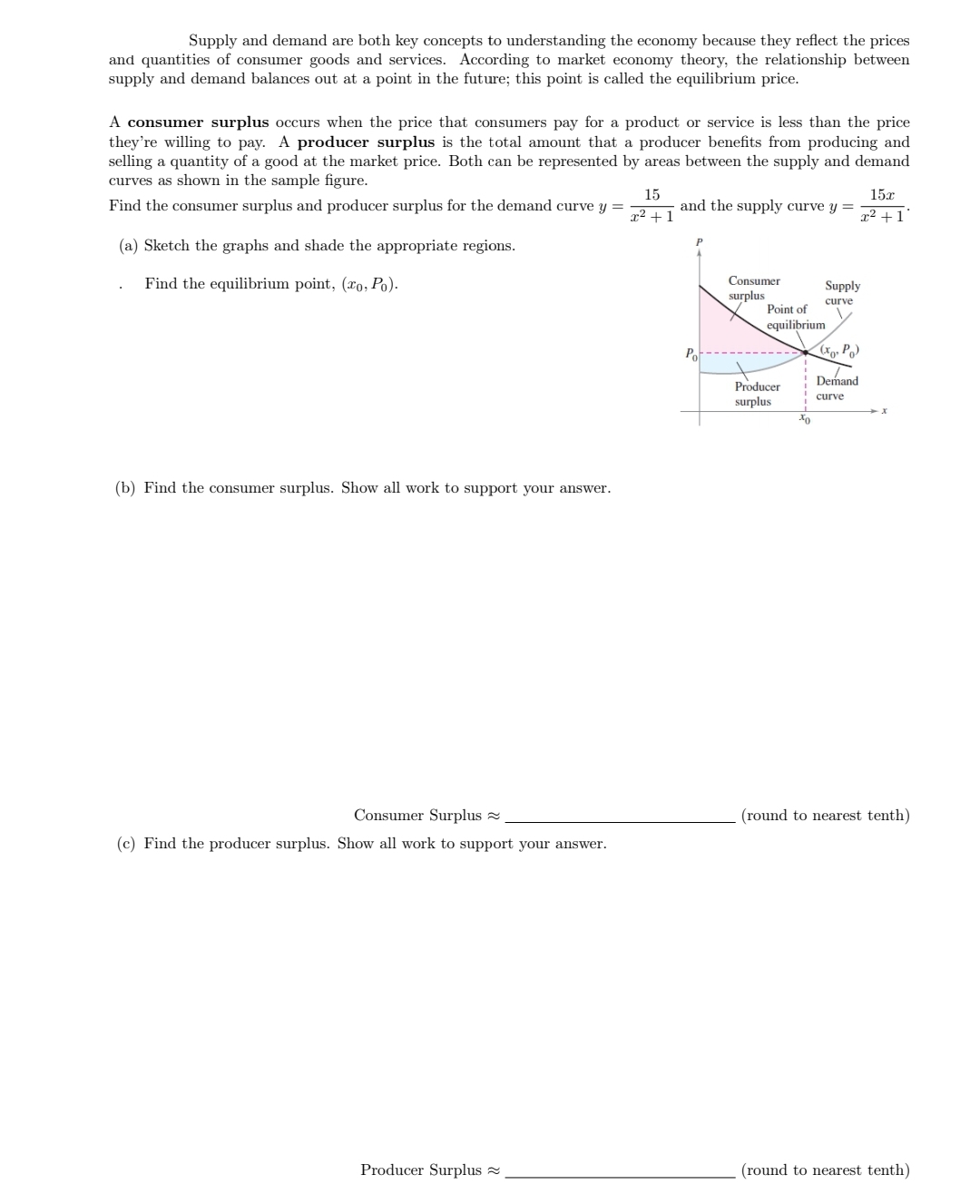

Transcribed Image Text:Supply and demand are both key concepts to understanding the economy because they reflect the prices

and quantities of consumer goods and services. According to market economy theory, the relationship between

supply and demand balances out at a point in the future; this point is called the equilibrium price.

A consumer surplus occurs when the price that consumers pay for a product or service is less than the price

they're willing to pay. A producer surplus is the total amount that a producer benefits from producing and

selling a quantity of a good at the market price. Both can be represented by areas between the supply and demand

curves as shown in the sample figure.

15

and the supply curve y =

15x

Find the consumer surplus and producer surplus for the demand curve y =

x² +1

x² +1°

(a) Sketch the graphs and shade the appropriate regions.

Find the equilibrium point, (xo, Po).

Consumer

Supply

surplus

curve

Point of

equilibrium

Po

(Xg. P)

Producer

Demand

curve

surplus

(b) Find the consumer surplus. Show all work to support your answer.

Consumer Surplus =

(round to nearest tenth)

(c) Find the producer surplus. Show all work to support your answer.

Producer Surplus =

(round to nearest tenth)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 3 images

Recommended textbooks for you

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning