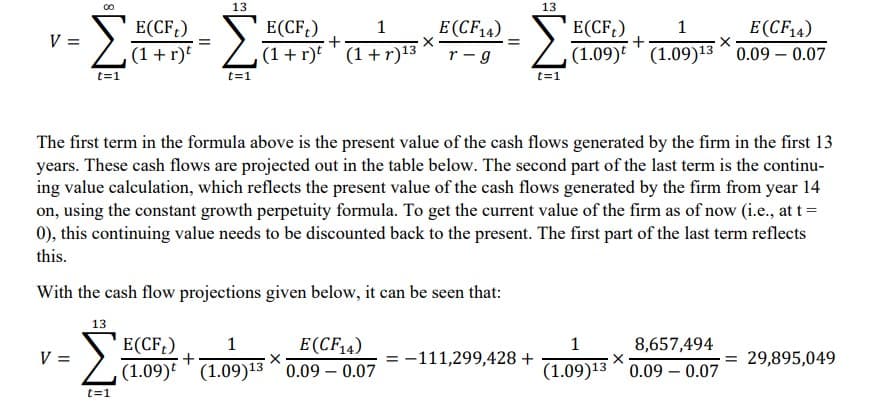

Suppose you are asked to value a small start-up company that is expected to generate a Free Cash Flow of - $100 million next year, and - $50 million in the following year (year 2), before the firm turns profitable in year 3. Its first positive cash flow is equal to $2 million, and cash flows are expected to grow at a rate of 15% per year for 10 years (until year 13). Then, between year 13 and 14, the growth rate drops to 7% and stays there forever. Value the start-up company if the relevant discount rate is equal to 9%. My question is when calculating the perpetuity with a cosntant growth rate, why we muliply: 1/(1+r)^13 * E(CF_14)/0,09-0,07 Why does this make sense?

Suppose you are asked to value a small start-up company that is expected to generate a Free Cash

Flow of - $100 million next year, and - $50 million in the following year (year 2), before the firm

turns profitable in year 3. Its first positive cash flow is equal to $2 million, and cash flows are expected to grow at a rate of 15% per year for 10 years (until year 13). Then, between year 13 and 14,

the growth rate drops to 7% and stays there forever. Value the start-up company if the relevant discount rate is equal to 9%.

My question is when calculating the perpetuity with a cosntant growth rate, why we muliply:

1/(1+r)^13 * E(CF_14)/0,09-0,07

Why does this make sense?

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images