The following information related to ExxonMobil's inventories is taken from its 2014 annual report. 3. Miscellaneous Financial Information In 2014, 2013, and 2012, net income included gains of $187 million, $282 million, and $328 million respectively, attributable to the combined effects of LIFO inventory accumulations and drawdowns. The aggregate replacement cost of inventories was estimated to exceed their LIFO carrying values by $10.6 billion and $21.2 billion at December 31, 2014 and 2013, respectively Crude oil, products, and merchandise as of year-end 2014 and 2013 consist of the following ($ in billions) 2014 2013 Petroleum products $4.1 $3.9 Crude oil 4.6 4.7 Chemical products 2.9 2.9 Gas/other 0.8 0.6 Total $12.4 $12.1 Required: page 497 1. By how much would net income for 2014 have differed had ExxonMobil used FIFO to value those inventory items valued under LIFO? Assume a 35% marginal tax rate. Be sure to indicate whether FIFO income would be higher or lower than LIFO income 2. What would the LIFO reserve have been on December 31, 2014, if no drawdowns had occurred in 2014? The drawdowns represent LIFO liquidations 3. What was the net difference in 2014 income taxes that ExxonMobil experienced as a result of using LIFO rather than FIFO? Assume a 35% tax rate and indicate whether FIFO or LIFO would yield the higher tax and by how much 4. What was the approximate rate of change in input costs in 2014 for ExxonMobil's inventory?

The following information related to ExxonMobil's inventories is taken from its 2014 annual report. 3. Miscellaneous Financial Information In 2014, 2013, and 2012, net income included gains of $187 million, $282 million, and $328 million respectively, attributable to the combined effects of LIFO inventory accumulations and drawdowns. The aggregate replacement cost of inventories was estimated to exceed their LIFO carrying values by $10.6 billion and $21.2 billion at December 31, 2014 and 2013, respectively Crude oil, products, and merchandise as of year-end 2014 and 2013 consist of the following ($ in billions) 2014 2013 Petroleum products $4.1 $3.9 Crude oil 4.6 4.7 Chemical products 2.9 2.9 Gas/other 0.8 0.6 Total $12.4 $12.1 Required: page 497 1. By how much would net income for 2014 have differed had ExxonMobil used FIFO to value those inventory items valued under LIFO? Assume a 35% marginal tax rate. Be sure to indicate whether FIFO income would be higher or lower than LIFO income 2. What would the LIFO reserve have been on December 31, 2014, if no drawdowns had occurred in 2014? The drawdowns represent LIFO liquidations 3. What was the net difference in 2014 income taxes that ExxonMobil experienced as a result of using LIFO rather than FIFO? Assume a 35% tax rate and indicate whether FIFO or LIFO would yield the higher tax and by how much 4. What was the approximate rate of change in input costs in 2014 for ExxonMobil's inventory?

Financial Reporting, Financial Statement Analysis and Valuation

8th Edition

ISBN:9781285190907

Author:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Chapter9: Operating Activities

Section: Chapter Questions

Problem 20PC: A large manufacturer of truck and car tires recently changed its cost-flow assumption method for...

Related questions

Question

*Question included in picture.

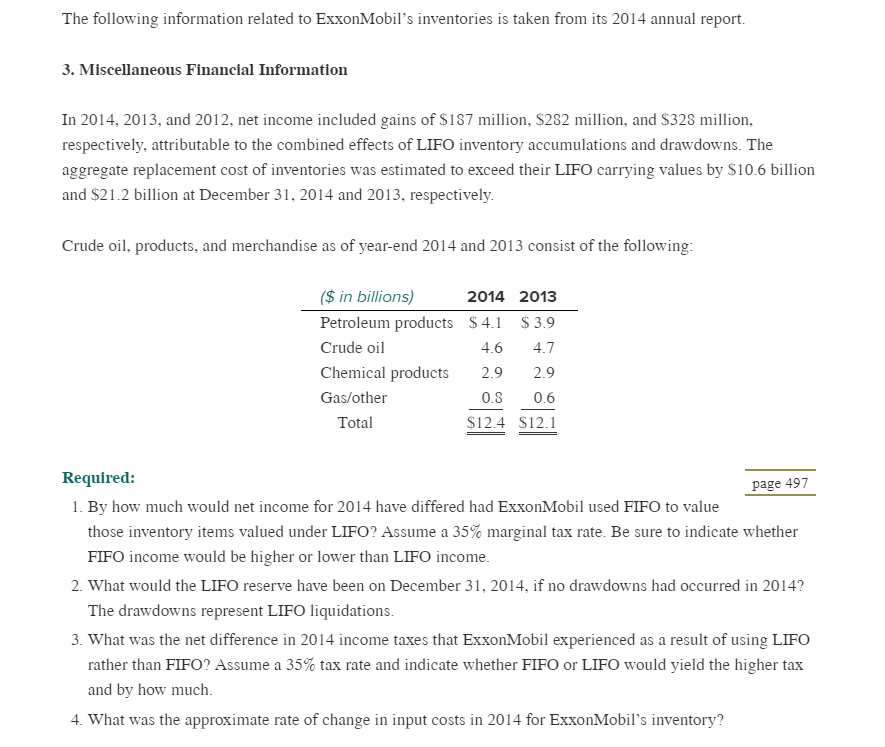

Transcribed Image Text:The following information related to ExxonMobil's inventories is taken from its 2014 annual report.

3. Miscellaneous Financial Information

In 2014, 2013, and 2012, net income included gains of $187 million, $282 million, and $328 million

respectively, attributable to the combined effects of LIFO inventory accumulations and drawdowns. The

aggregate replacement cost of inventories was estimated to exceed their LIFO carrying values by $10.6 billion

and $21.2 billion at December 31, 2014 and 2013, respectively

Crude oil, products, and merchandise as of year-end 2014 and 2013 consist of the following

($ in billions)

2014 2013

Petroleum products $4.1

$3.9

Crude oil

4.6

4.7

Chemical products

2.9

2.9

Gas/other

0.8

0.6

Total

$12.4 $12.1

Required:

page 497

1. By how much would net income for 2014 have differed had ExxonMobil used FIFO to value

those inventory items valued under LIFO? Assume a 35% marginal tax rate. Be sure to indicate whether

FIFO income would be higher or lower than LIFO income

2. What would the LIFO reserve have been on December 31, 2014, if no drawdowns had occurred in 2014?

The drawdowns represent LIFO liquidations

3. What was the net difference in 2014 income taxes that ExxonMobil experienced as a result of using LIFO

rather than FIFO? Assume a 35% tax rate and indicate whether FIFO or LIFO would yield the higher tax

and by how much

4. What was the approximate rate of change in input costs in 2014 for ExxonMobil's inventory?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning