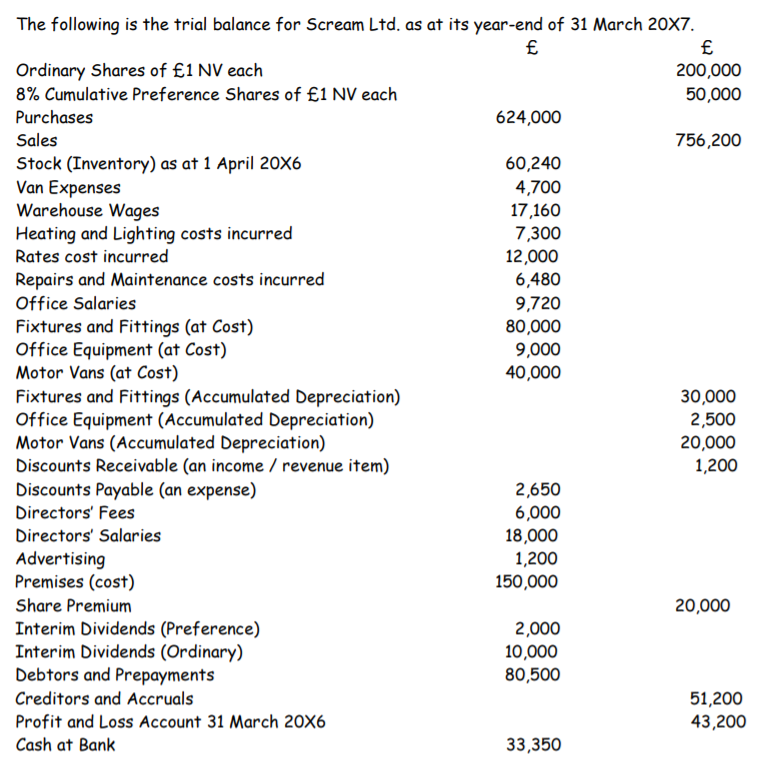

The following is the trial balance for Scream Ltd. as at its year-end of 31 March 20X7. £ Ordinary Shares of £1 NV each 200,000 50,000 8% Cumulative Preference Shares of £1 NV each Purchases 624,000 Sales 756,200 Stock (Inventory) as at 1 April 20X6 Van Expenses Warehouse Wages Heating and Lighting costs incurred Rates cost incurred 60,240 4,700 17,160 7,300 12,000 Repairs and Maintenance costs incurred Office Salaries 6,480 9,720 Fixtures and Fittings (at Cost) Office Equipment (at Cost) Motor Vans (at Cost) Fixtures and Fittings (Accumulated Depreciation) Office Equipment (Accumulated Depreciation) Motor Vans (Accumulated Depreciation) Discounts Receivable (an income / revenue item) Discounts Payable (an expense) 80,000 9,000 40,000 30,000 2,500 20,000 1,200 2,650 Directors' Fees 6,000 Directors' Salaries 18,000 1,200 Advertising Premises (cost) 150,000 Share Premium 20,000 Interim Dividends (Preference) Interim Dividends (Ordinary) Debtors and Prepayments 2,000 10,000 80,500 Creditors and Accruals 51,200 43,200 Profit and Loss Account 31 March 20X6 Cash at Bank 33,350

The following is the trial balance for Scream Ltd. as at its year-end of 31 March 20X7. £ Ordinary Shares of £1 NV each 200,000 50,000 8% Cumulative Preference Shares of £1 NV each Purchases 624,000 Sales 756,200 Stock (Inventory) as at 1 April 20X6 Van Expenses Warehouse Wages Heating and Lighting costs incurred Rates cost incurred 60,240 4,700 17,160 7,300 12,000 Repairs and Maintenance costs incurred Office Salaries 6,480 9,720 Fixtures and Fittings (at Cost) Office Equipment (at Cost) Motor Vans (at Cost) Fixtures and Fittings (Accumulated Depreciation) Office Equipment (Accumulated Depreciation) Motor Vans (Accumulated Depreciation) Discounts Receivable (an income / revenue item) Discounts Payable (an expense) 80,000 9,000 40,000 30,000 2,500 20,000 1,200 2,650 Directors' Fees 6,000 Directors' Salaries 18,000 1,200 Advertising Premises (cost) 150,000 Share Premium 20,000 Interim Dividends (Preference) Interim Dividends (Ordinary) Debtors and Prepayments 2,000 10,000 80,500 Creditors and Accruals 51,200 43,200 Profit and Loss Account 31 March 20X6 Cash at Bank 33,350

Survey of Accounting (Accounting I)

8th Edition

ISBN:9781305961883

Author:Carl Warren

Publisher:Carl Warren

Chapter9: Metric-analysis Of Financial Statements

Section: Chapter Questions

Problem 9.4.5P: Twenty metrics of liquidity, solvency, and profitability The comparative financial statements of...

Related questions

Question

Transcribed Image Text:The following is the trial balance for Scream Ltd. as at its year-end of 31 March 20X7.

Ordinary Shares of £1 NV each

200,000

8% Cumulative Preference Shares of £1 NV each

50,000

Purchases

624,000

Sales

756,200

Stock (Inventory) as at 1 April 20X6

Van Expenses

Warehouse Wages

Heating and Lighting costs incurred

Rates cost incurred

60,240

4,700

17,160

7,300

12,000

6,480

9,720

80,000

9,000

40,000

Repairs and Maintenance costs incurred

Office Salaries

Fixtures and Fittings (at Cost)

Office Equipment (at Cost)

Motor Vans (at Cost)

Fixtures and Fittings (Accumulated Depreciation)

Office Equipment (Accumulated Depreciation)

Motor Vans (Accumulated Depreciation)

Discounts Receivable (an income / revenue item)

Discounts Payable (an expense)

30,000

2,500

20,000

1,200

2,650

Directors' Fees

6,000

Directors' Salaries

18,000

Advertising

Premises (cost)

1,200

150,000

Share Premium

20,000

Interim Dividends (Preference)

Interim Dividends (Ordinary)

Debtors and Prepayments

2,000

10,000

80,500

51,200

43,200

Creditors and Accruals

Profit and Loss Account 31 March 20X6

Cash at Bank

33,350

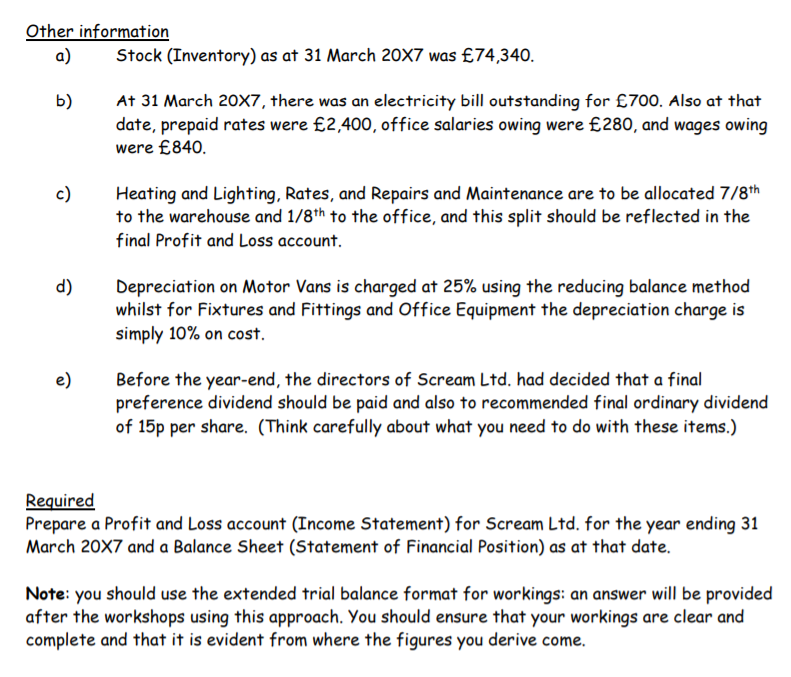

Transcribed Image Text:Other information

a)

Stock (Inventory) as at 31 March 20X7 was £74,340.

At 31 March 20X7, there was an electricity bill outstanding for £700. Also at that

date, prepaid rates were £2,400, office salaries owing were £280, and wages owing

were £840.

b)

Heating and Lighting, Rates, and Repairs and Maintenance are to be allocated 7/8th

to the warehouse and 1/8th to the office, and this split should be reflected in the

final Profit and Loss account.

c)

d)

Depreciation on Motor Vans is charged at 25% using the reducing balance method

whilst for Fixtures and Fittings and Office Equipment the depreciation charge is

simply 10% on cost.

e)

Before the year-end, the directors of Scream Ltd. had decided that a final

preference dividend should be paid and also to recommended final ordinary dividend

of 15p per share. (Think carefully about what you need to do with these items.)

Required

Prepare a Profit and Loss account (Income Statement) for Scream Ltd. for the year ending 31

March 20X7 and a Balance Sheet (Statement of Financial Position) as at that date.

Note: you should use the extended trial balance format for workings: an answer will be provided

after the workshops using this approach. You should ensure that your workings are clear and

complete and that it is evident from where the figures you derive come.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning