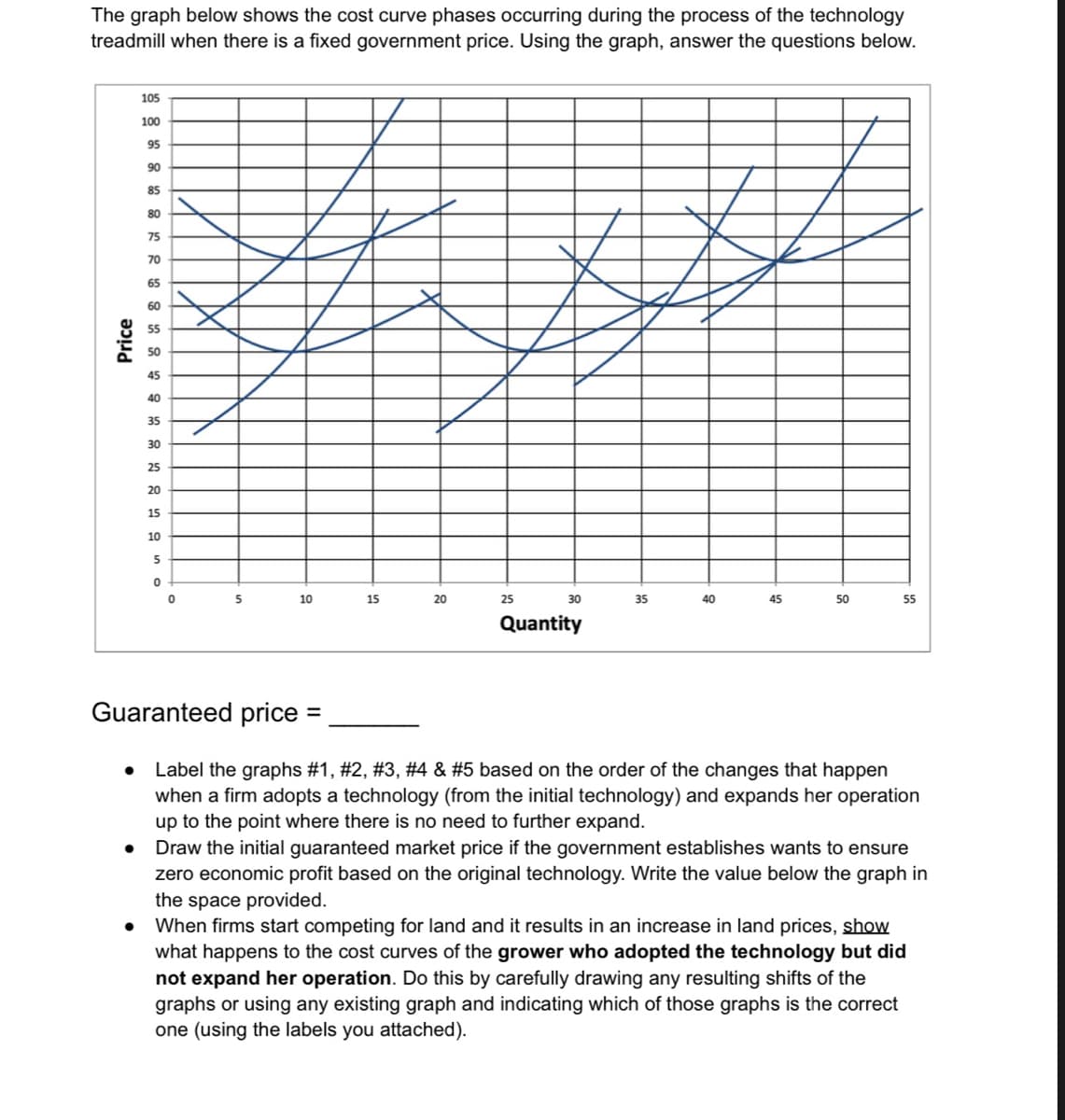

The graph below shows the cost curve phases occurring during the process of the technology treadmill when there is a fixed government price. Using the graph, answer the questions below. Price 105 ● * શ્રુ છુ ૩ 95 85 70 65 60 55 50 45 40 35 30 25 20 15 10 5 0 0 5 10 15 20 25 30 Quantity 35 40 45 50 55 Guaranteed price = Label the graphs #1, #2, #3, #4 & #5 based on the order of the changes that happen when a firm adopts a technology (from the initial technology) and expands her operation up to the point where there is no need to further expand. Draw the initial guaranteed market price if the government establishes wants to ensure zero economic profit based on the original technology. Write the value below the graph in the space provided. When firms start competing for land and it results in an increase in land prices, show what happens to the cost curves of the grower who adopted the technology but did not expand her operation. Do this by carefully drawing any resulting shifts of the graphs or using any existing graph and indicating which of those graphs is the correct one (using the labels you attached).

The graph below shows the cost curve phases occurring during the process of the technology treadmill when there is a fixed government price. Using the graph, answer the questions below. Price 105 ● * શ્રુ છુ ૩ 95 85 70 65 60 55 50 45 40 35 30 25 20 15 10 5 0 0 5 10 15 20 25 30 Quantity 35 40 45 50 55 Guaranteed price = Label the graphs #1, #2, #3, #4 & #5 based on the order of the changes that happen when a firm adopts a technology (from the initial technology) and expands her operation up to the point where there is no need to further expand. Draw the initial guaranteed market price if the government establishes wants to ensure zero economic profit based on the original technology. Write the value below the graph in the space provided. When firms start competing for land and it results in an increase in land prices, show what happens to the cost curves of the grower who adopted the technology but did not expand her operation. Do this by carefully drawing any resulting shifts of the graphs or using any existing graph and indicating which of those graphs is the correct one (using the labels you attached).

Microeconomics: Principles & Policy

14th Edition

ISBN:9781337794992

Author:William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:William J. Baumol, Alan S. Blinder, John L. Solow

Chapter18: Pricing The Factors Of Production

Section: Chapter Questions

Problem 2TY

Related questions

Question

5 the graph below shows the cost curve phases occurring during the process of the technology treadmill when there is a fixed government price . Using the graph answer the questions below

Transcribed Image Text:The graph below shows the cost curve phases occurring during the process of the technology

treadmill when there is a fixed government price. Using the graph, answer the questions below.

Price

105

100

95

90

85

80

75

70

●

65

60

55

50

45

40

35

30

25

20

15

10

5

0

0

5

10

15

20

25

30

Quantity

#

35

40

45

50

55

Guaranteed price

Label the graphs #1, #2, #3, #4 & #5 based on the order of the changes that happen

when a firm adopts a technology (from the initial technology) and expands her operation

up to the point where there is no need to further expand.

Draw the initial guaranteed market price if the government establishes wants to ensure

zero economic profit based on the original technology. Write the value below the graph in

the space provided.

When firms start competing for land and it results in an increase in land prices, show

what happens to the cost curves of the grower who adopted the technology but did

not expand her operation. Do this by carefully drawing any resulting shifts of the

graphs or using any existing graph and indicating which of those graphs is the correct

one (using the labels you attached).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Microeconomics: Principles & Policy

Economics

ISBN:

9781337794992

Author:

William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:

Cengage Learning

Microeconomics: Principles & Policy

Economics

ISBN:

9781337794992

Author:

William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:

Cengage Learning