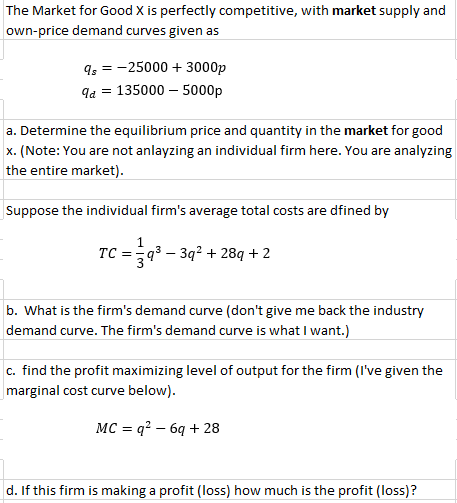

The Market for Good X is perfectly competitive, with market supply and own-price demand curves given as q, = -25000 + 3000p 9a = 135000 – 5000p a. Determine the equilibrium price and quantity in the market for good x. (Note: You are not anlayzing an individual firm here. You are analyzing the entire market). Suppose the individual firm's average total costs are dfined by TC =q3 – 3q2 + 28q + 2 b. What is the firm's demand curve (don't give me back the industry demand curve. The firm's demand curve is what I want.) c. find the profit maximizing level of output for the firm (I've given the marginal cost curve below). MC = q? – 6q + 28 d. If this firm is making a profit (loss) how much is the profit (loss)?

The Market for Good X is perfectly competitive, with market supply and own-price demand curves given as q, = -25000 + 3000p 9a = 135000 – 5000p a. Determine the equilibrium price and quantity in the market for good x. (Note: You are not anlayzing an individual firm here. You are analyzing the entire market). Suppose the individual firm's average total costs are dfined by TC =q3 – 3q2 + 28q + 2 b. What is the firm's demand curve (don't give me back the industry demand curve. The firm's demand curve is what I want.) c. find the profit maximizing level of output for the firm (I've given the marginal cost curve below). MC = q? – 6q + 28 d. If this firm is making a profit (loss) how much is the profit (loss)?

Chapter11: Profit Maximization

Section: Chapter Questions

Problem 11.12P

Related questions

Question

b,c,d would be amazing. THank you

Transcribed Image Text:The Market for Good X is perfectly competitive, with market supply and

own-price demand curves given as

q, = -25000 + 3000p

qa = 135000 – 5000p

a. Determine the equilibrium price and quantity in the market for good

x. (Note: You are not anlayzing an individual firm here. You are analyzing

the entire market).

Suppose the individual firm's average total costs are dfined by

TC =

q3 – 3q2 + 289 +2

b. What is the firm's demand curve (don't give me back the industry

demand curve. The firm's demand curve is what I want.)

c. find the profit maximizing level of output for the firm (I've given the

marginal cost curve below).

MC = q? – 6q + 28

d. If this firm is making a profit (loss) how much is the profit (loss)?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you