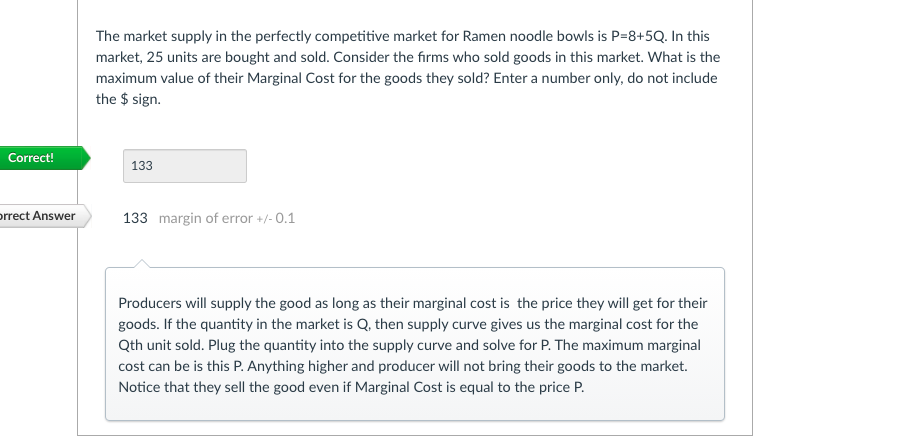

The market supply in the perfectly competitive market for Ramen noodle bowls is P=8+5Q. In this market, 25 units are bought and sold. Consider the firms who sold goods in this market. What is the maximum value of their Marginal Cost for the goods they sold? Enter a number only, do not include the $ sign.

The market supply in the perfectly competitive market for Ramen noodle bowls is P=8+5Q. In this market, 25 units are bought and sold. Consider the firms who sold goods in this market. What is the maximum value of their Marginal Cost for the goods they sold? Enter a number only, do not include the $ sign.

Chapter19: Externalities And Public Goods

Section: Chapter Questions

Problem 19.1P: A firm in a perfectly competitive industry has patented a newprocess for making widgets. The new...

Related questions

Question

Question in image. Been stuck on for hours.

If you don't understand how to solve, let someone else answer it instead of rejecting question

Warm regards.

Transcribed Image Text:The market supply in the perfectly competitive market for Ramen noodle bowls is P=8+5Q. In this

market, 25 units are bought and sold. Consider the firms who sold goods in this market. What is the

maximum value of their Marginal Cost for the goods they sold? Enter a number only, do not include

the $ sign.

Correct!

133

prrect Answer

133 margin of error +/- 0.1

Producers will supply the good as long as their marginal cost is the price they will get for their

goods. If the quantity in the market is Q, then supply curve gives us the marginal cost for the

Qth unit sold. Plug the quantity into the supply curve and solve for P. The maximum marginal

cost can be is this P. Anything higher and producer will not bring their goods to the market.

Notice that they sell the good even if Marginal Cost is equal to the price P.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you