The multiplier for a futures contract on a stock market index is $80. The maturity of the contract is one year, the current level of the index is $5,100, and the risk-free interest rate is 0.4% per month. The dividend yield on the index is 0.1% per month. Suppose that after one month, the stock index is at 5,150. Required: a. Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly. b. Find the holding-period return if the initial margin on the contract is $10,600. Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required A Required B Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly. Note: Do not round intermediate calculations. Round your answer to 2 decimal places. Cash flow $ 4,000.00 x

The multiplier for a futures contract on a stock market index is $80. The maturity of the contract is one year, the current level of the index is $5,100, and the risk-free interest rate is 0.4% per month. The dividend yield on the index is 0.1% per month. Suppose that after one month, the stock index is at 5,150. Required: a. Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly. b. Find the holding-period return if the initial margin on the contract is $10,600. Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required A Required B Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly. Note: Do not round intermediate calculations. Round your answer to 2 decimal places. Cash flow $ 4,000.00 x

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 9P

Related questions

Question

Baghiben

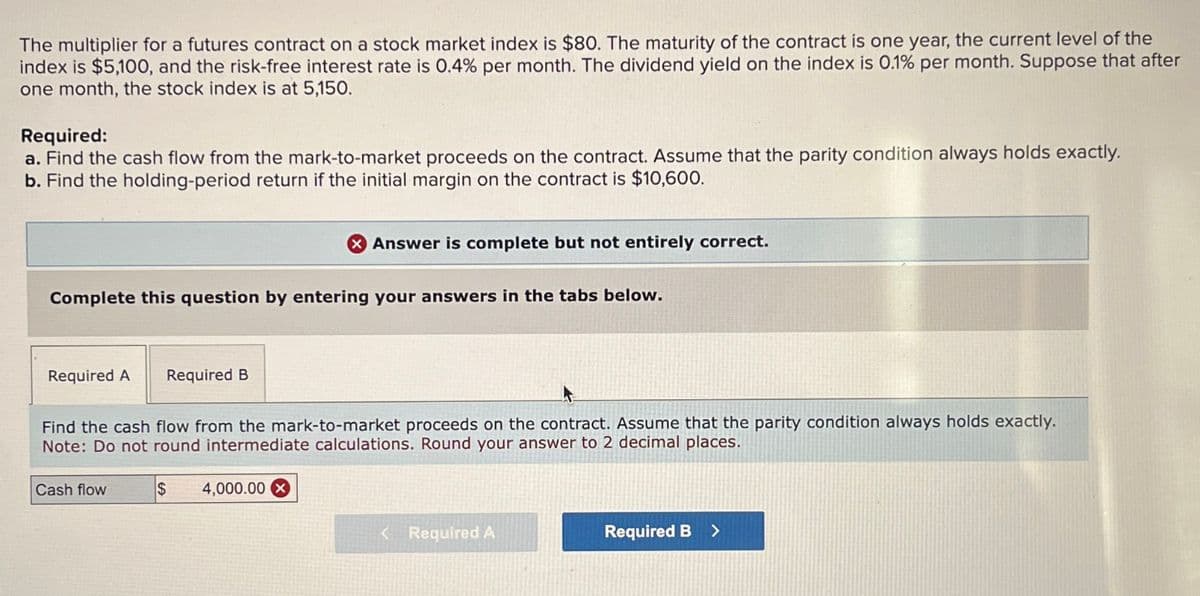

Transcribed Image Text:The multiplier for a futures contract on a stock market index is $80. The maturity of the contract is one year, the current level of the

index is $5,100, and the risk-free interest rate is 0.4% per month. The dividend yield on the index is 0.1% per month. Suppose that after

one month, the stock index is at 5,150.

Required:

a. Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly.

b. Find the holding-period return if the initial margin on the contract is $10,600.

Answer is complete but not entirely correct.

Complete this question by entering your answers in the tabs below.

Required A

Required B

Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly.

Note: Do not round intermediate calculations. Round your answer to 2 decimal places.

Cash flow

$

4,000.00 x

<Required A

Required B >

AI-Generated Solution

Unlock instant AI solutions

Tap the button

to generate a solution

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning