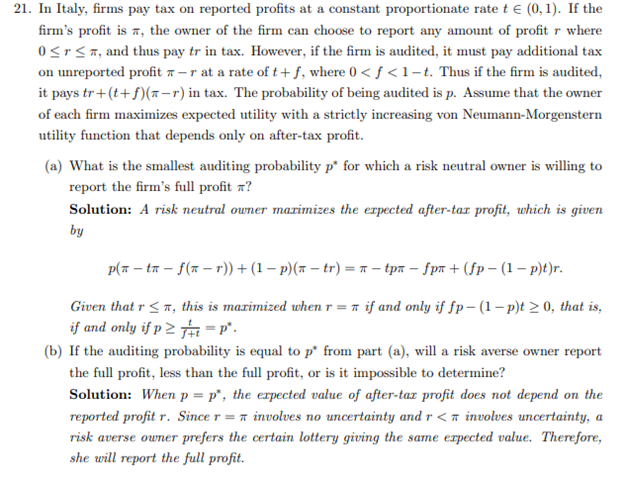

21. In Italy, firms pay tax on reported profits at a constant proportionate rate t € (0, 1). If the firm's profit is a, the owner of the firm can choose to report any amount of profit r where 0 ≤ ≤, and thus pay tr in tax. However, if the firm is audited, it must pay additional tax on unreported profit -r at a rate of t+f, where 0

21. In Italy, firms pay tax on reported profits at a constant proportionate rate t € (0, 1). If the firm's profit is a, the owner of the firm can choose to report any amount of profit r where 0 ≤ ≤, and thus pay tr in tax. However, if the firm is audited, it must pay additional tax on unreported profit -r at a rate of t+f, where 0

Chapter18: Asymmetric Information

Section: Chapter Questions

Problem 18.10P

Related questions

Question

please only do: if you can teach explain steps of how to solve each part

Transcribed Image Text:21. In Italy, firms pay tax on reported profits at a constant proportionate rate t€ (0, 1). If the

firm's profit is, the owner of the firm can choose to report any amount of profit r where

0 ≤r ≤, and thus pay tr in tax. However, if the firm is audited, it must pay additional tax

on unreported profit -r at a rate of t+f, where 0<f<1-t. Thus if the firm is audited,

it pays tr+(t+f)(n-r) in tax. The probability of being audited is p. Assume that the owner

of each firm maximizes expected utility with a strictly increasing von Neumann-Morgenstern

utility function that depends only on after-tax profit.

(a) What is the smallest auditing probability p* for which a risk neutral owner is willing to

report the firm's full profit ?

Solution: A risk neutral owner maximizes the expected after-tax profit, which is given

by

p(n-tn-f(nr)) + (1 − p)(x − tr) = π- tpx − ƒp + (fp-(1-p)t)r.

Given that r ≤, this is maximized when r = if and only if fp-(1-p)t≥ 0, that is,

if and only if p≥t=P².

(b) If the auditing probability is equal to p* from part (a), will a risk averse owner report

the full profit, less than the full profit, or is it impossible to determine?

Solution: When p = p, the expected value of after-tax profit does not depend on the

reported profit r. Since r = involves no uncertainty and r < involves uncertainty, a

risk averse owner prefers the certain lottery giving the same expected value. Therefore,

she will report the full profit.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 1 images

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

why is this Utility from reporting full tax = (1-t)π

Solution

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you