(1) Calculate the following variances between the budgeted contribution margin and the actual contribution margin for May. Assume that all raw material purchased during May was placed into production. Provide all steps of calculations. (a) direct labour rate variance (b) direct labour efficiency variance (c) direct material price variance (d) direct material quantity variance (e) variable overhead spending variance (f) variable overhead efficiency variance (g) sales price variance (h) sales volume variance (5) Prepare a revised contribution margin report showing proper variable cost variances based on a flexible budget instead of the static budget used by Robert Smith. Use the following format: Static Flexible Actual Variance Budget Budget Units Revenue Variable costs: Direct material Housing units Printed circuit boards Reading Heads Total direct material Direct labour Assembly Printed circuit boards Reading Heads Total direct labour Variable overhead Total variable costs Contribution margin CAN YOU PLEASE SOLVE QUESTION 1. E AND F ALSO QUESTION 5 PLEASE !!!

Video Tech Ltd manufactures video game machines. Market saturation and technological

innovations have caused pricing pressures that have resulted in declining profits. To stem the

slide in profits until new products can be introduced, top management has started to focus on

achieving cost savings in manufacturing and increases in sales volume. Sales can be increased

only if production volume increases. Therefore, an incentive program has been developed to

reward those production managers who contribute to an increase in the number of units

produced and achieve cost reductions. In addition, a just-in-time purchasing program has been

implemented, and raw materials are purchased on an as-needed basis.

The production managers have responded to the pressure to improve manufacturing

performance and this has resulted in an increase in the number of completed units over normal

production levels. The video game machines are put together by the assembly group, which

requires parts from both the printed circuit boards (PCB) and the reading heads (RH) groups.

To increase production levels, the PCB and RH groups started to reject parts that previously

would have been tested and modified to meet manufacturing standards. Preventative

maintenance on machines used in the production of these parts has been postponed, with only

emergency repair work being performed to keep production lines moving. The maintenance

department is concerned that there will be serious breakdowns and unsafe operating conditions.

The more aggressive assembly group production supervisors have pressured maintenance

personnel to attend to their machines at the expense of other groups. This has resulted in

machine downtime in the PCB and RH groups which, when coupled with demands for

accelerated parts delivery by the assembly group, has led to more frequent parts rejections and

increased friction between departments. Video Tech uses a

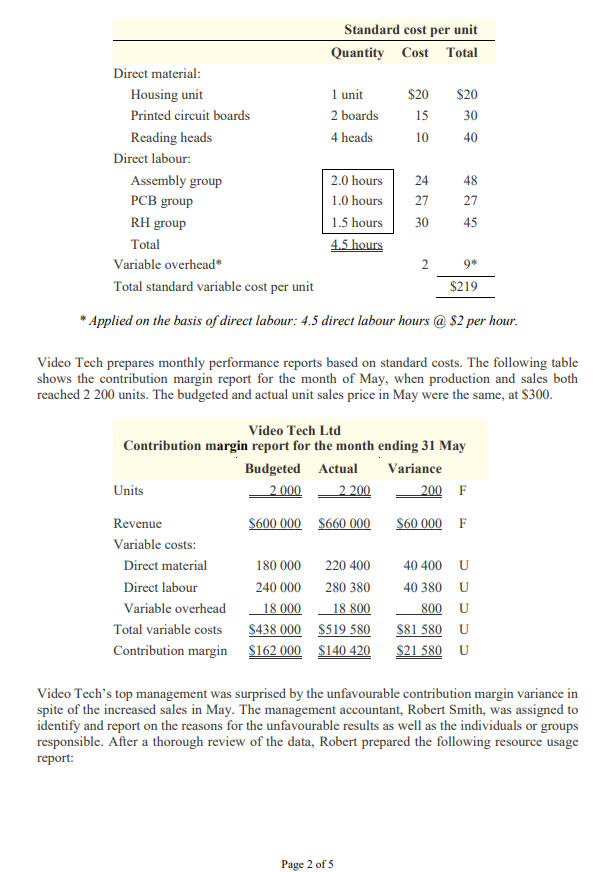

standard costs for video game machines are as follows:

DATA SHOWN IN IMAGE 1 ATTACHED...

Video Tech prepares monthly performance reports based on standard costs. The following table

shows the contribution margin report for the month of May, when production and sales both

reached 2 200 units. The budgeted and actual unit sales price in May were the same, at $300.

DATA SHOWN IN IMAGE 1 ATTACHED...

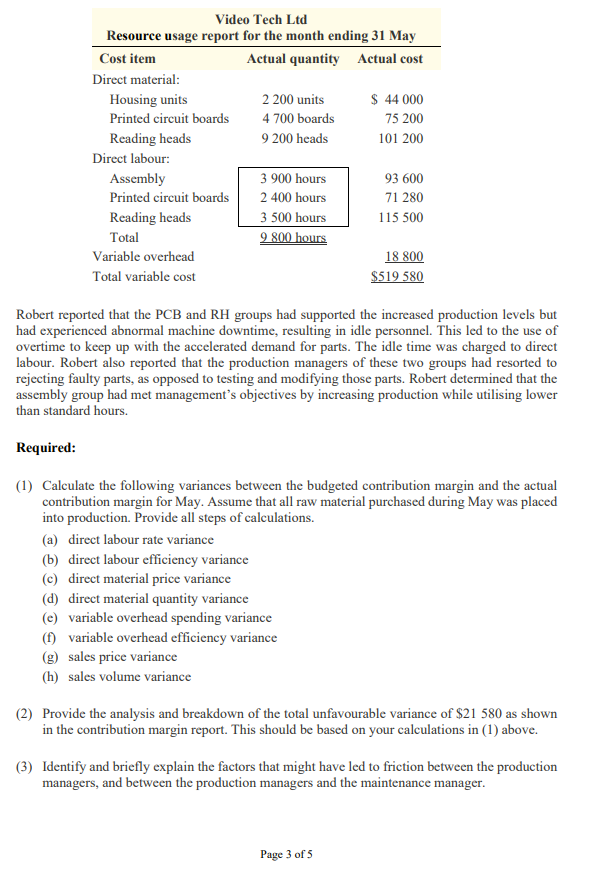

Video Tech’s top management was surprised by the unfavourable contribution margin variance in

spite of the increased sales in May. The

identify and report on the reasons for the unfavourable results as well as the individuals or groups

responsible. After a thorough review of the data, Robert prepared the following resource usage

report:

DATA SHOWN IN IMAGE 2 ATTACHED...

Robert reported that the PCB and RH groups had supported the increased production levels but

had experienced abnormal machine downtime, resulting in idle personnel. This led to the use of

overtime to keep up with the accelerated demand for parts. The idle time was charged to direct

labour. Robert also reported that the production managers of these two groups had resorted to

rejecting faulty parts, as opposed to testing and modifying those parts. Robert determined that the

assembly group had met management’s objectives by increasing production while utilising lower

than standard hours.

Required:

(1) Calculate the following variances between the budgeted contribution margin and the actual

contribution margin for May. Assume that all raw material purchased during May was placed

into production. Provide all steps of calculations.

(a) direct labour rate variance

(b) direct labour efficiency variance

(c) direct material price variance

(d) direct material quantity variance

(e) variable overhead spending variance

(f) variable overhead efficiency variance

(g) sales price variance

(h) sales volume variance

(5) Prepare a revised contribution margin report showing proper variable cost variances based on

a flexible budget instead of the static budget used by Robert Smith. Use the following format:

Static Flexible Actual Variance

Budget Budget

Units

Revenue

Variable costs:

Direct material

Housing units

Printed circuit boards

Reading Heads

Total direct material

Direct labour

Assembly

Printed circuit boards

Reading Heads

Total direct labour

Variable overhead

Total variable costs

Contribution margin

CAN YOU PLEASE SOLVE QUESTION 1. E AND F

ALSO QUESTION 5 PLEASE !!!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Hi Tutor, Can you please write some comment for revised contribution margin I mean how it came and also its impacts on this case and role of it in this case.

IT would be highly appreciated