1 What is thế annual lease payment? a 400,000 b. 435,044 c. 480,000 d. 522,053 2 What is the total annual lease payment? a 420,000 b. 455,044 c. 542,053 d. 500,000 & What is the unearned interest income of the lessor at: the beginning of current year?

1 What is thế annual lease payment? a 400,000 b. 435,044 c. 480,000 d. 522,053 2 What is the total annual lease payment? a 420,000 b. 455,044 c. 542,053 d. 500,000 & What is the unearned interest income of the lessor at: the beginning of current year?

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter20: Accounting For Leases

Section: Chapter Questions

Problem 1E: Determining Type of Lease and Subsequent Accounting On January 1, 2019, Caswell Company signs a...

Related questions

Question

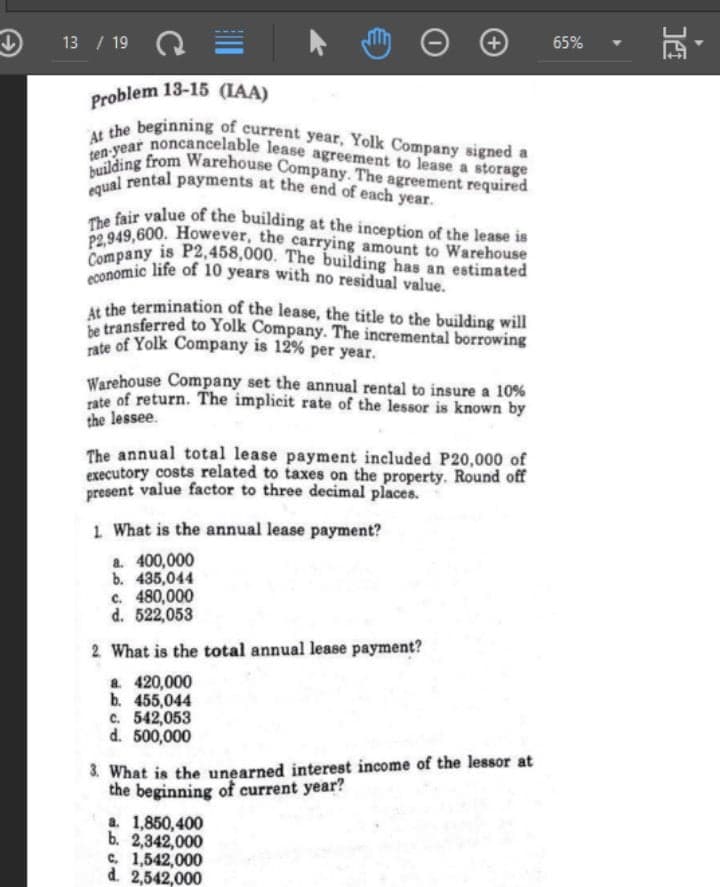

Transcribed Image Text:building from Warehouse Company. The agreement required

ten-year noncancelable lease agreement to lease a storage

At the beginning of current year, Yolk Company signed a

equal rental payments at the end of each year.

The fair value of the building at the inception of the lease is

P2,949,600. However, the carrying amount to Warehouse

economic life of 10 years with no residual value.

Company is P2,458,000. The building has an estimated

rate of Yolk Company is 12% per year.

13 / 19

65%

Problem 13-15 (IAA)

Company is P2,458,000. The building has an estimated

At the termination of the lease, the title to the building will

transferred to Yolk Company. The incremental borrowing

te of Yolk Company is 12% per year.

Warehouse Company set the annual rental to insure a 10%

rate of return. The implicit rate of the lessor is known by

the lessee.

The annual total lease payment included P20,000 of

executory costs related to taxes on the property. Round off

present value factor to three decimal places.

1 What is the annual lease payment?

a. 400,000

b. 435,044

c. 480,000

d. 522,053

2 What is the total annual lease payment?

a. 420,000

b. 455,044

c. 542,053

d. 500,000

3 What is the unearned interest income of the lessor at

the beginning of current year?

a. 1,850,400

b. 2,342,000

C. 1,542,000

d. 2,542,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning