1. An extract of the trail balance of ABC at 30 September 2012 is set out below: Credit ('000) Particulars Debit ('000) Premises at cost 800 Plant and equipment at cost 460 Motor vehicles at cost 100 Accumulated depreciation at 1/10/2011: Premises 200 Plant & equipment 260 Motor vehicles 73 Inventory at 1/10/2011 144 Purchases 2317 Sales of finished goods 2689 Bank 363 Bank deposit account 496 Bank interest 19 Finance costs 20 Preference dividend paid Trade receivables and payables 256 170 Prepayments and Accruals Administration expenses 27 152 207 10% Loan note (repayment due 2019) Ordinary share capital Irredeemable preference share capital Share premium Retained earnings at 1/10/2011 200 650 100 250 432 ΤΟTAL 5195 5195 Notes: 1. Closing inventory at 30 September 2012 was valued at cost of Rs. 94,000. 2. The premises were revalued from a carrying value of Rs. 6,00,000 to Rs. 8,50,000 during the year. 3. Administration expenses included a dividend paid by ABC to its shareholders of Rs. 31,000. 4. The income tax charge on the profit for the year amounted to Rs. 39,000 and had not yet been accounted for. 5. The 10% loan note had been in issue throughout the year ended 30 Sept 2012. Required: (a) to prepare the statement of comprehensive income for the year ended 30 September 20X2. (b) to prepare the statement of changes in equity for the year ended 30 September 20X2. st (c) to prepare the statement of financial position at 30 September 20X2. stP

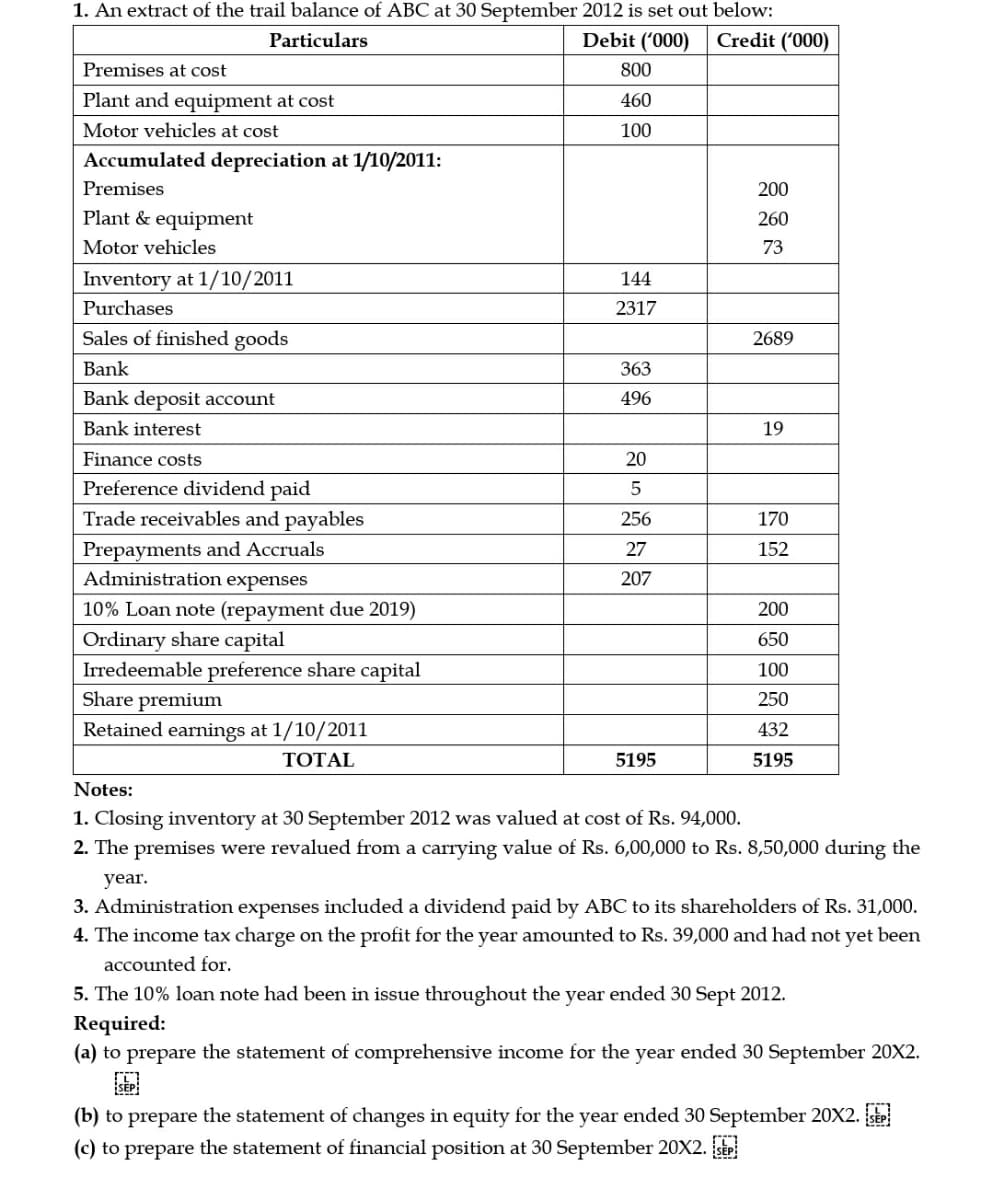

1. An extract of the trail balance of ABC at 30 September 2012 is set out below: Credit ('000) Particulars Debit ('000) Premises at cost 800 Plant and equipment at cost 460 Motor vehicles at cost 100 Accumulated depreciation at 1/10/2011: Premises 200 Plant & equipment 260 Motor vehicles 73 Inventory at 1/10/2011 144 Purchases 2317 Sales of finished goods 2689 Bank 363 Bank deposit account 496 Bank interest 19 Finance costs 20 Preference dividend paid Trade receivables and payables 256 170 Prepayments and Accruals Administration expenses 27 152 207 10% Loan note (repayment due 2019) Ordinary share capital Irredeemable preference share capital Share premium Retained earnings at 1/10/2011 200 650 100 250 432 ΤΟTAL 5195 5195 Notes: 1. Closing inventory at 30 September 2012 was valued at cost of Rs. 94,000. 2. The premises were revalued from a carrying value of Rs. 6,00,000 to Rs. 8,50,000 during the year. 3. Administration expenses included a dividend paid by ABC to its shareholders of Rs. 31,000. 4. The income tax charge on the profit for the year amounted to Rs. 39,000 and had not yet been accounted for. 5. The 10% loan note had been in issue throughout the year ended 30 Sept 2012. Required: (a) to prepare the statement of comprehensive income for the year ended 30 September 20X2. (b) to prepare the statement of changes in equity for the year ended 30 September 20X2. st (c) to prepare the statement of financial position at 30 September 20X2. stP

Chapter12: Current Liabilities

Section: Chapter Questions

Problem 1PB: Consider the following situations and determine (1) which type of liability should be recognized...

Related questions

Question

Transcribed Image Text:1. An extract of the trail balance of ABC at 30 September 2012 is set out below:

Credit ('000)

Particulars

Debit ('000)

Premises at cost

800

Plant and equipment at cost

460

Motor vehicles at cost

100

Accumulated depreciation at 1/10/2011:

Premises

200

Plant & equipment

260

Motor vehicles

73

Inventory at 1/10/2011

144

Purchases

2317

Sales of finished goods

2689

Bank

363

Bank deposit account

496

Bank interest

19

Finance costs

20

Preference dividend paid

Trade receivables and payables

Prepayments and Accruals

Administration expenses

256

170

27

152

207

10% Loan note (repayment due 2019)

Ordinary share capital

Irredeemable preference share capital

Share premium

Retained earnings at 1/10/2011

200

650

100

250

432

ТОTAL

5195

5195

Notes:

1. Closing inventory at 30 September 2012 was valued at cost of Rs. 94,000.

2. The premises were revalued from a carrying value of Rs. 6,00,000 to Rs. 8,50,000 during the

year.

3. Administration expenses included a dividend paid by ABC to its shareholders of Rs. 31,000.

4. The income tax charge on the profit for the year amounted to Rs. 39,000 and had not yet been

accounted for.

5. The 10% loan note had been in issue throughout the year ended 30 Sept 2012.

Required:

(a) to prepare the statement of comprehensive income for the year ended 30 September 20X2.

(b) to prepare the statement of changes in equity for the year ended 30 September 20X2. s

(c) to prepare the statement of financial position at 30 September 20X2. st

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning