1. Consider the following information: In New York €1 =$1.09251 In Frankfurt £1 = €1.1234 In London $1 = £0.85 (a) Determine if there is a currency arbitrage opportunity in this 3-currency situation. (b) If there is such an opportunity, explain how you may be able to capture this profit. YOU NEED TO ILLUSTRATE YOUR PROFITABLE ROAD MAP WITH A NUMERICAL EXAMPLE

1. Consider the following information: In New York €1 =$1.09251 In Frankfurt £1 = €1.1234 In London $1 = £0.85 (a) Determine if there is a currency arbitrage opportunity in this 3-currency situation. (b) If there is such an opportunity, explain how you may be able to capture this profit. YOU NEED TO ILLUSTRATE YOUR PROFITABLE ROAD MAP WITH A NUMERICAL EXAMPLE

Chapter7: International Arbitrage And Interest Rate Parity

Section: Chapter Questions

Problem 51QA

Related questions

Question

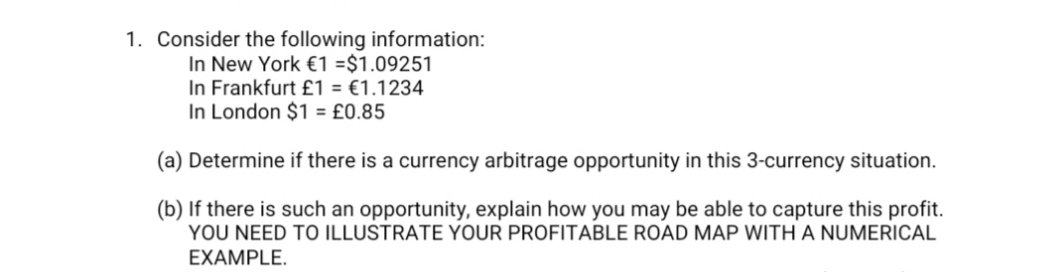

Transcribed Image Text:1. Consider the following information:

In New York €1 =$1.09251

In Frankfurt £1 = €1.1234

In London $1 = £0.85

(a) Determine if there is a currency arbitrage opportunity in this 3-currency situation.

(b) If there is such an opportunity, explain how you may be able to capture this profit.

YOU NEED TO ILLUSTRATE YOUR PROFITABLE ROAD MAP WITH A NUMERICAL

EXAMPLE.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning