1. How much is overstatement(understatement) of the retained earnings by the end of 2019? (if UNDER, put a negative sign before the numerical figure) *

1. How much is overstatement(understatement) of the retained earnings by the end of 2019? (if UNDER, put a negative sign before the numerical figure) *

1. How much is overstatement(understatement) of the retained earnings by the end of 2019? (if UNDER, put a negative sign before the numerical figure) *

1. How much is overstatement(understatement) of the retained earnings by the end of 2019? (if UNDER, put a negative sign before the numerical figure) *

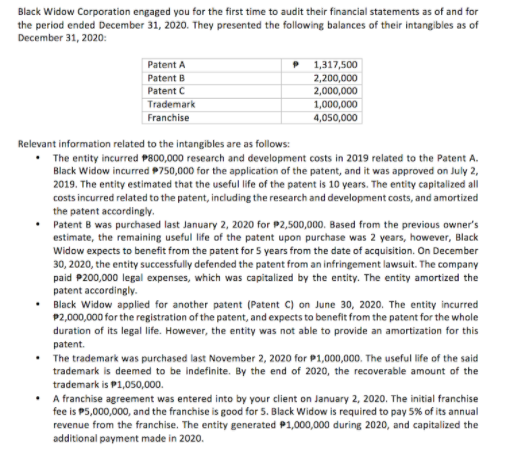

Transcribed Image Text:Black Widow Corporation engaged you for the first time to audit their financial statements as of and for

the period ended December 31, 2020. They presented the following balances of their intangibles as of

December 31, 2020:

Patent A

1,317,500

2,200,000

Patent B

Patent C

2,000,000

Trademark

1,000,000

Franchise

4,050,000

Relevant information related to the intangibles are as follows:

• The entity incurred P800,000 research and development costs in 2019 related to the Patent A.

Black Widow incurred 9750,000 for the application of the patent, and it was approved on July 2,

2019. The entity estimated that the useful life of the patent is 10 years. The entity capitalized all

costs incurred related to the patent, including the research and development costs, and amortized

the patent accordingly.

Patent B was purchased last January 2, 2020 for P2,500,000. Based from the previous owner's

estimate, the remaining useful life of the patent upon purchase was 2 years, however, Black

Widow expects to benefit from the patent for 5 years from the date of acquisition. On December

30, 2020, the entity successfully defended the patent from an infringement lawsuit. The company

paid P200,000 legal expenses, which was capitalized by the entity. The entity amortized the

patent accordingly.

• Black Widow applied for another patent (Patent C) on June 30, 2020. The entity incurred

P2,000,000 for the registration of the patent, and expects to benefit from the patent for the whole

duration of its legal life. However, the entity was not able to provide an amortization for this

patent.

• The trademark was purchased last November 2, 2020 for P1,000,000. The useful life of the said

trademark is deemed to be indefinite. By the end of 2020, the recoverable amount of the

trademark is P1,050,000.

• A franchise agreement was entered into by your client on January 2, 2020. The initial franchise

fee is P5,000,000, and the franchise is good for 5. Black Widow is required to pay 5% of its annual

revenue from the franchise. The entity generated P1,000,000 during 2020, and capitalized the

additional payment made in 2020.

Definition Definition Remaining net income of the company after the required dividends are paid to shareholders. This surplus money is usually invested back into the business to expand its business operations or launch a new product.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.